Is Everyone Having Fun Yet?

Credit: X

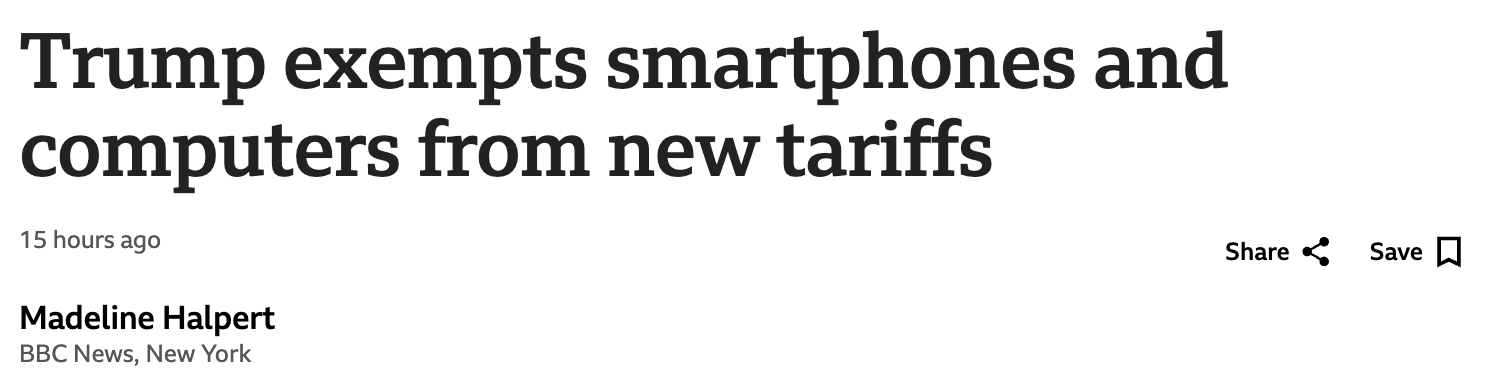

After a wild week of intense geopolitical aggression from the US vs the rest of the world, we ended the week on a strong note as President Trump appears to have made a significant concession with a stated exemption on smartphones, computers, and other electronic devices from reciprocal tariffs. Specifically, the US Customs and Border Patrol also said that the goods would be excluded from Trump’s 10% global tariff on most countries.

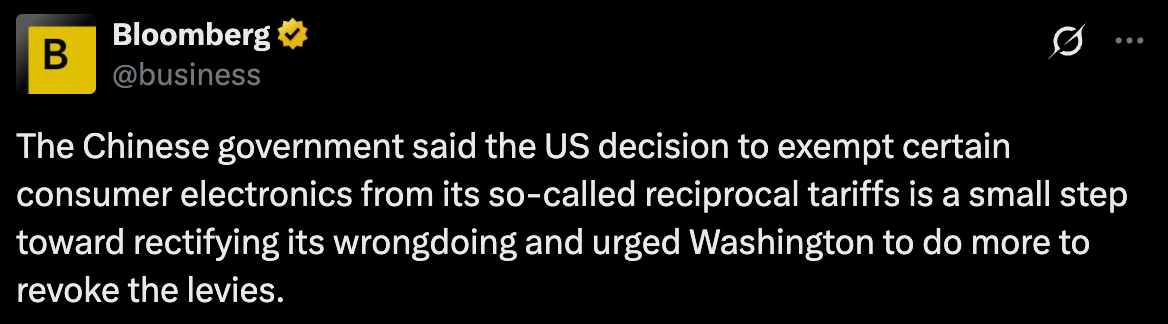

The Chinese government responded positively and stated the move as a ‘small step’ towards rectifying Washington’s ‘wrong doing’ and removing the rest of the levies.

Trump’s Latest “Apple-Saving Exemptions” Signals a Substantial Retreat From His Tariff Transgressions

Source: BBC, Bloomberg

Risk assets obviously welcomed the move, with Nasdaq gaining 1.5% and China equities rallying by over 3% in the early Asian session. Even some subsequent retractions from Lutnick and the Trump administration were not able to dull the risk-on sentiment, with participants cautiously hopeful that the worst rhetoric is behind us (for now).

Tariff Exemptions –> Refunds –> Delays –> Recategorization –> Reversal… Macro is Starting to Tune Out the Trade Noises Now

Source: CNBC

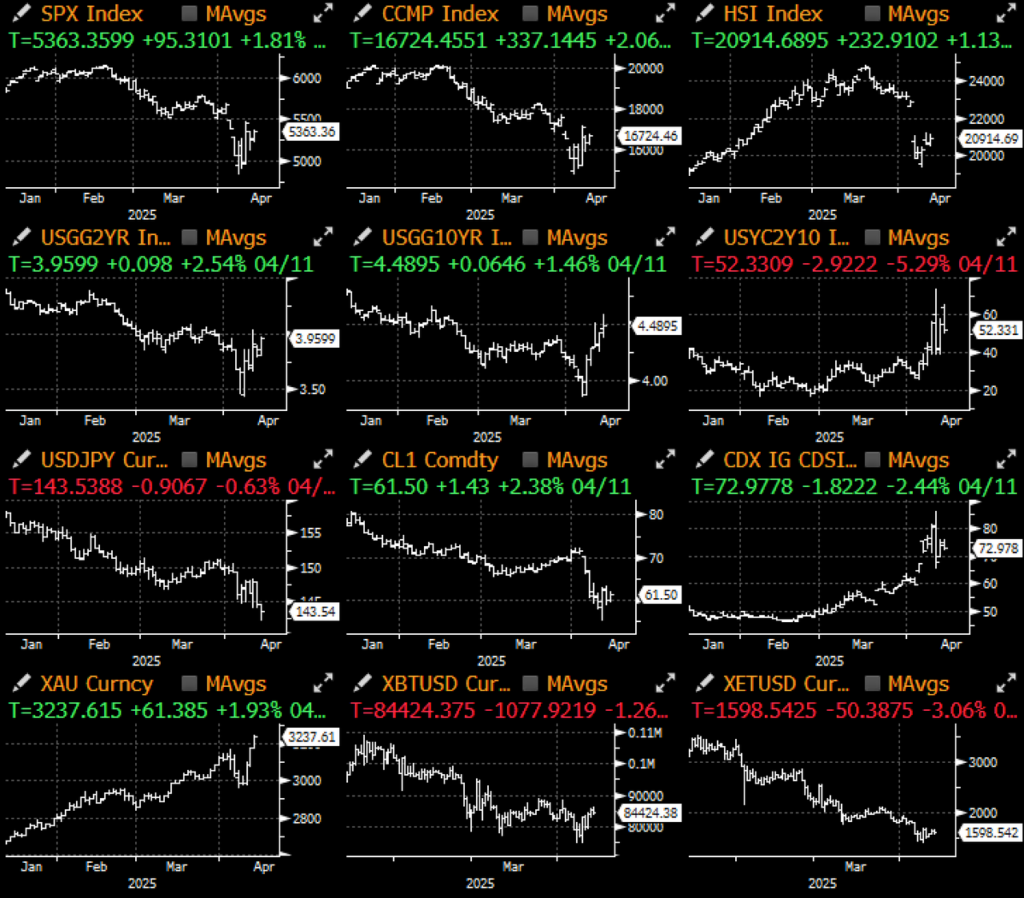

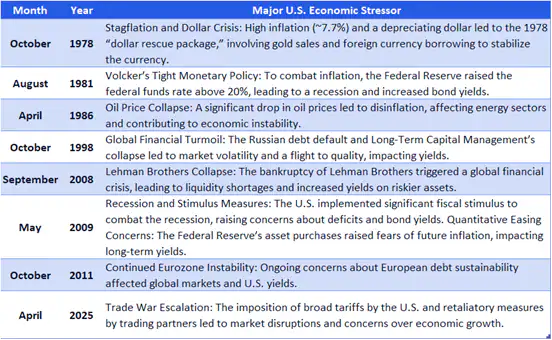

Despite the impressive risk bounce, US assets have suffered notably throughout this tariff saga, with the USD losing 3% and 10yr yields rising by nearly 60bp over the past week on heavy trading volumes. Citi reports that there were ~13 other historical instances where the dollar fell over 2% and 10y yields rose by over 30bp, ranging from the late 70s stagflation crisis, early 80s Volcker shock, and the Eurzone crisis in early 2010s. Historically, the SPX had recovered with double digital gains across the majority of these instances, but are things different this time around? Only time will tell.

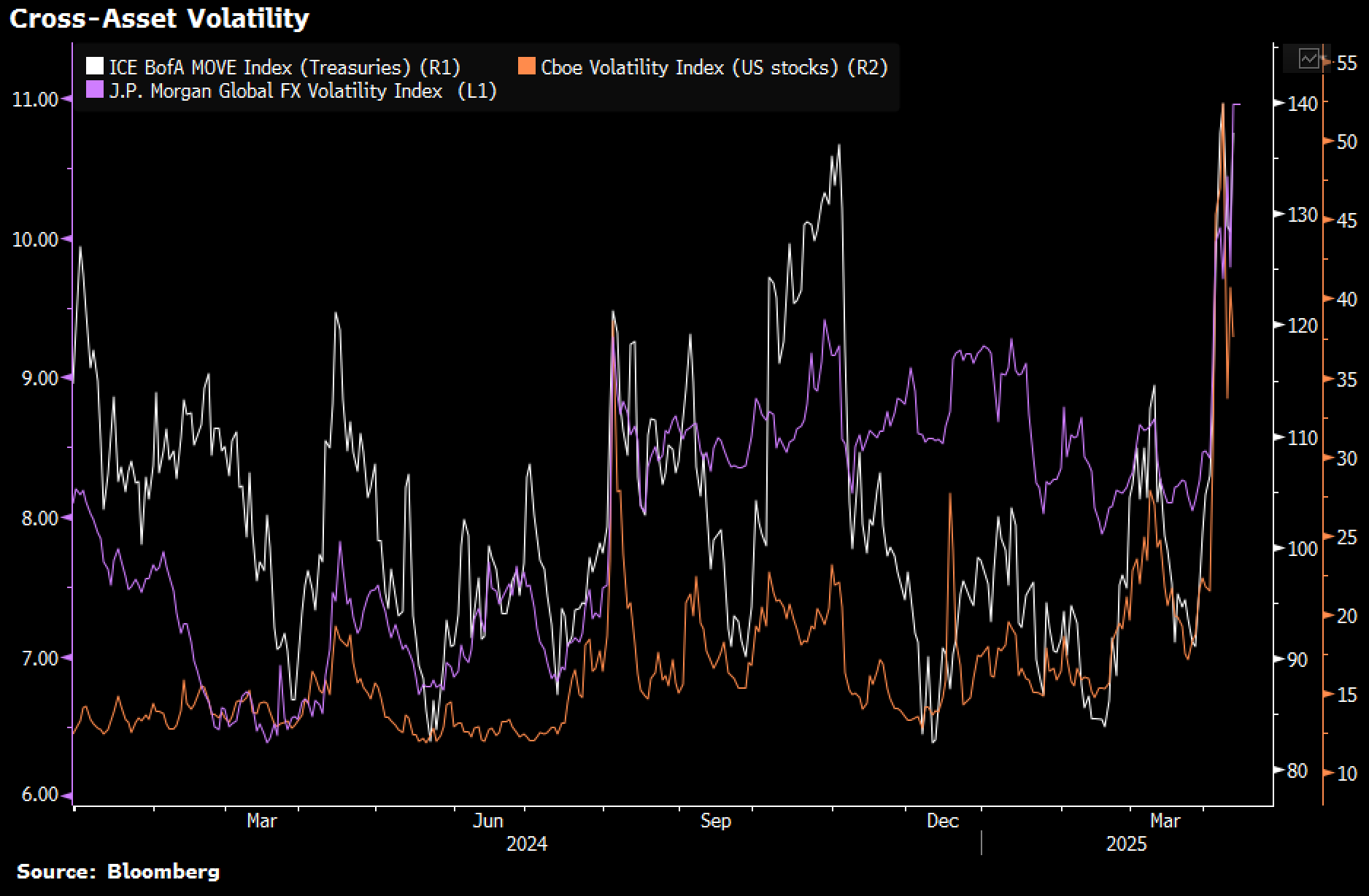

Cross Asset Volatilities have Spiked from the Tariff Saga

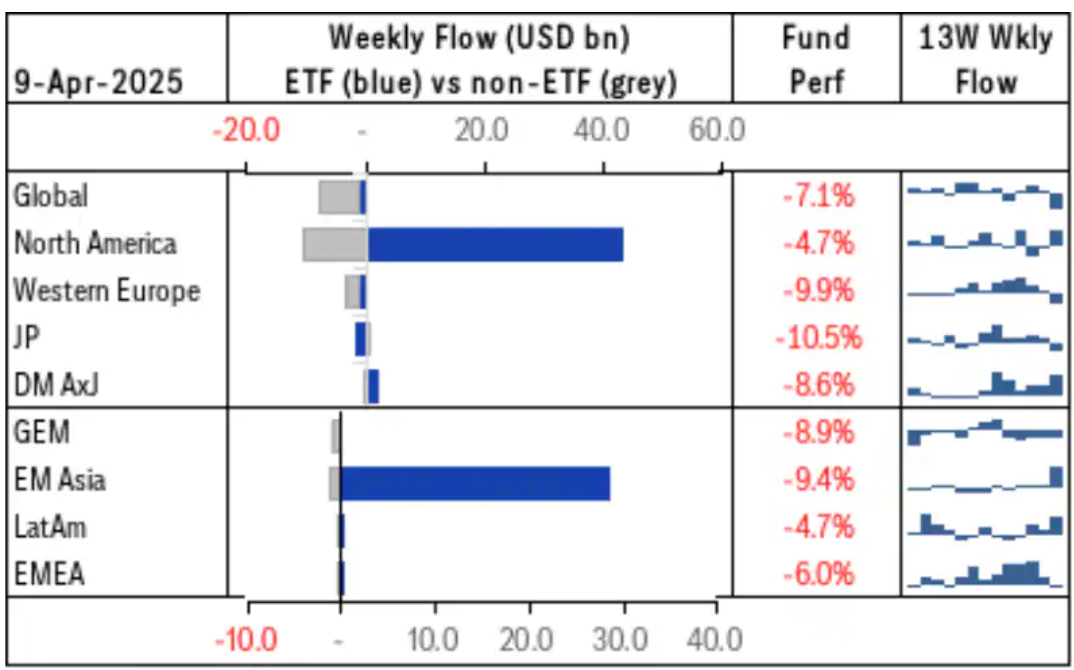

Net international official demand for US stocks cratered over the past month, as Central Banks divested out of their USD holdings as a tariff response; however, retail demand for US & China equities remained healthy as investors remained in buy-the-dip mode, offsetting much of the aggressive selling from HFs that pushed US equities into deep oversold territory.

Foreign Official Accounts were Large Net Sellers of US Equities, vs Still Healthy Buying from US Retail

Source: LSEG, Citi

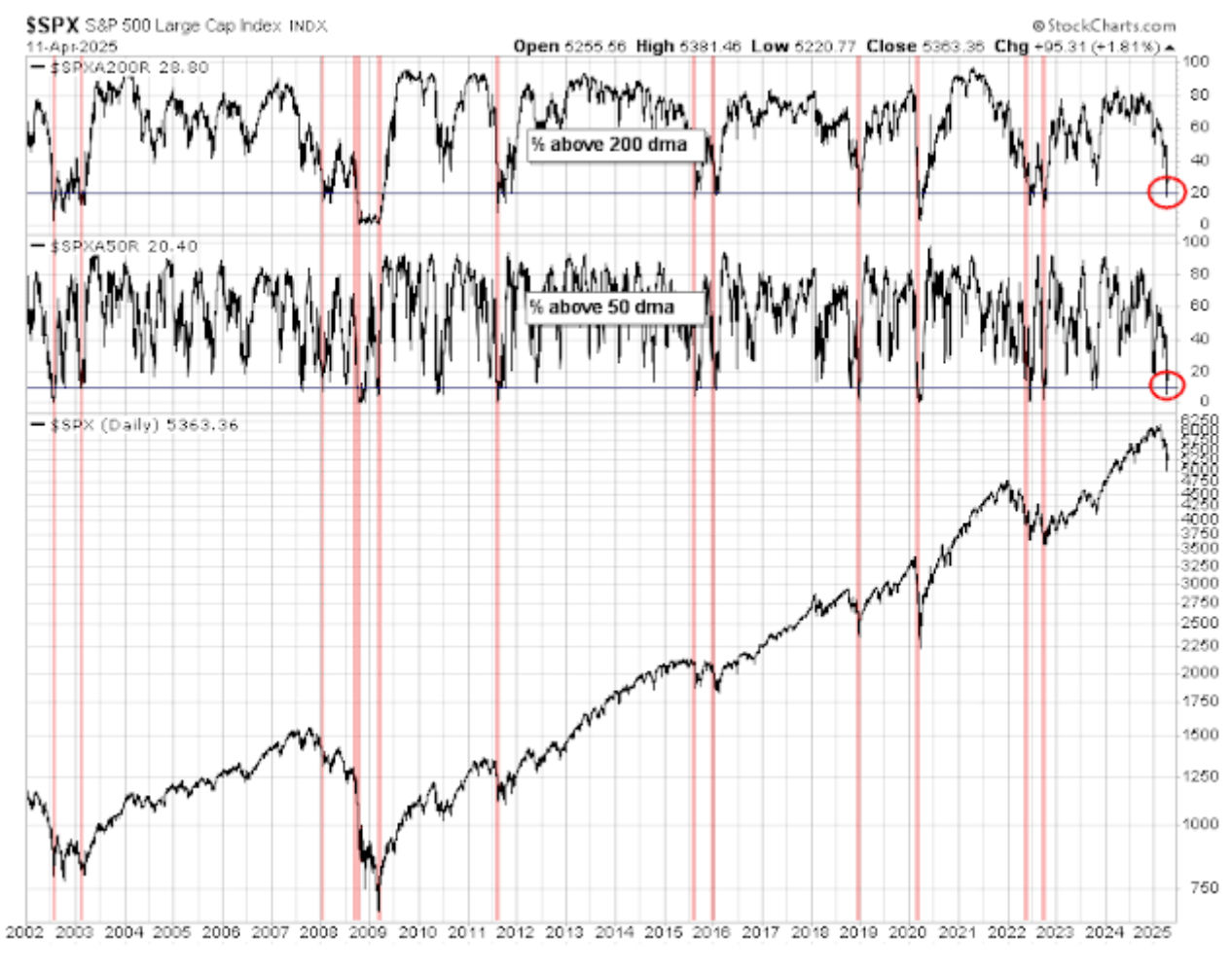

SPX went into Deep Oversold Territory as Hedge Funds Derisked Aggressively Across the Board

Source: Cam Hui

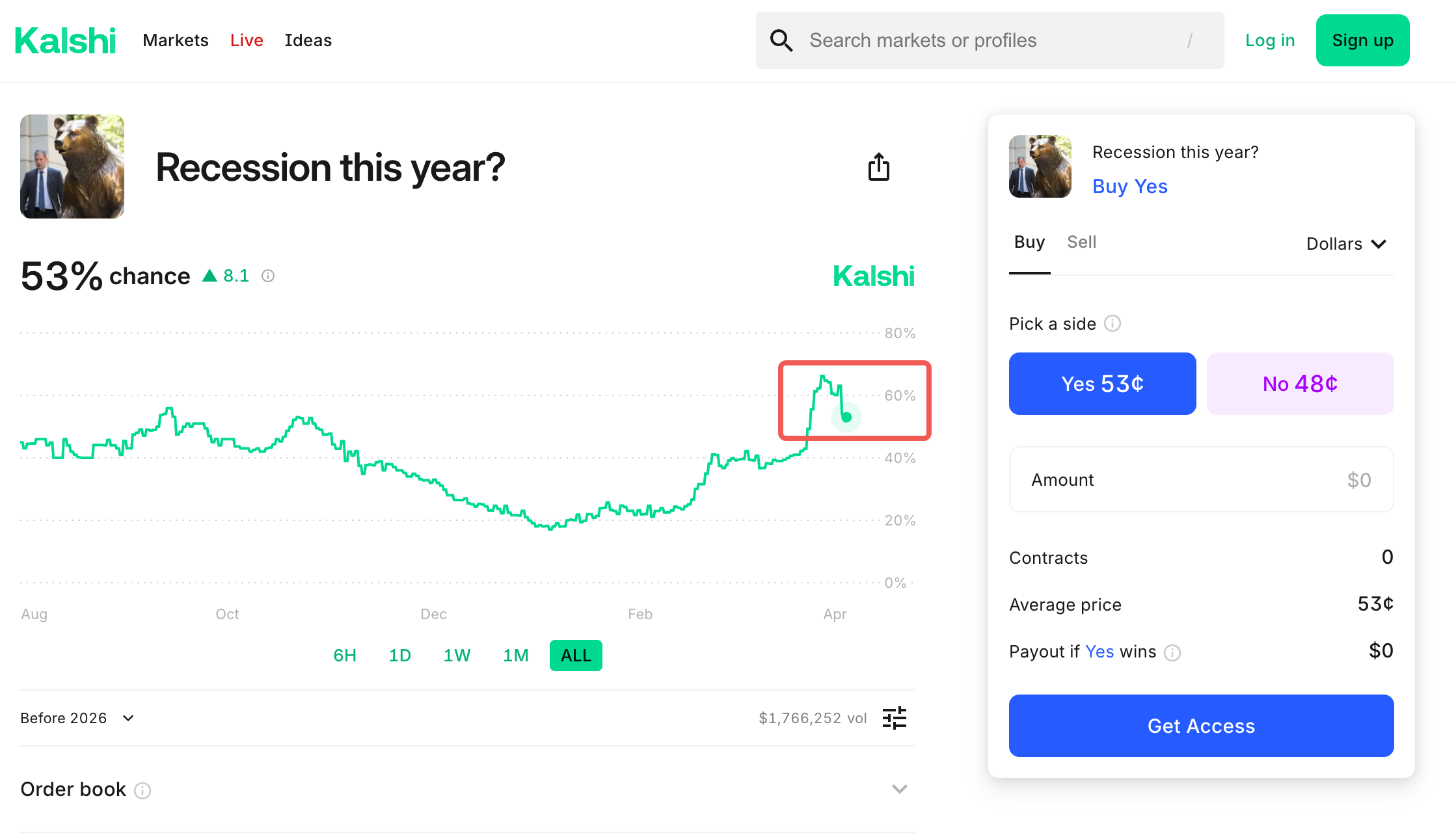

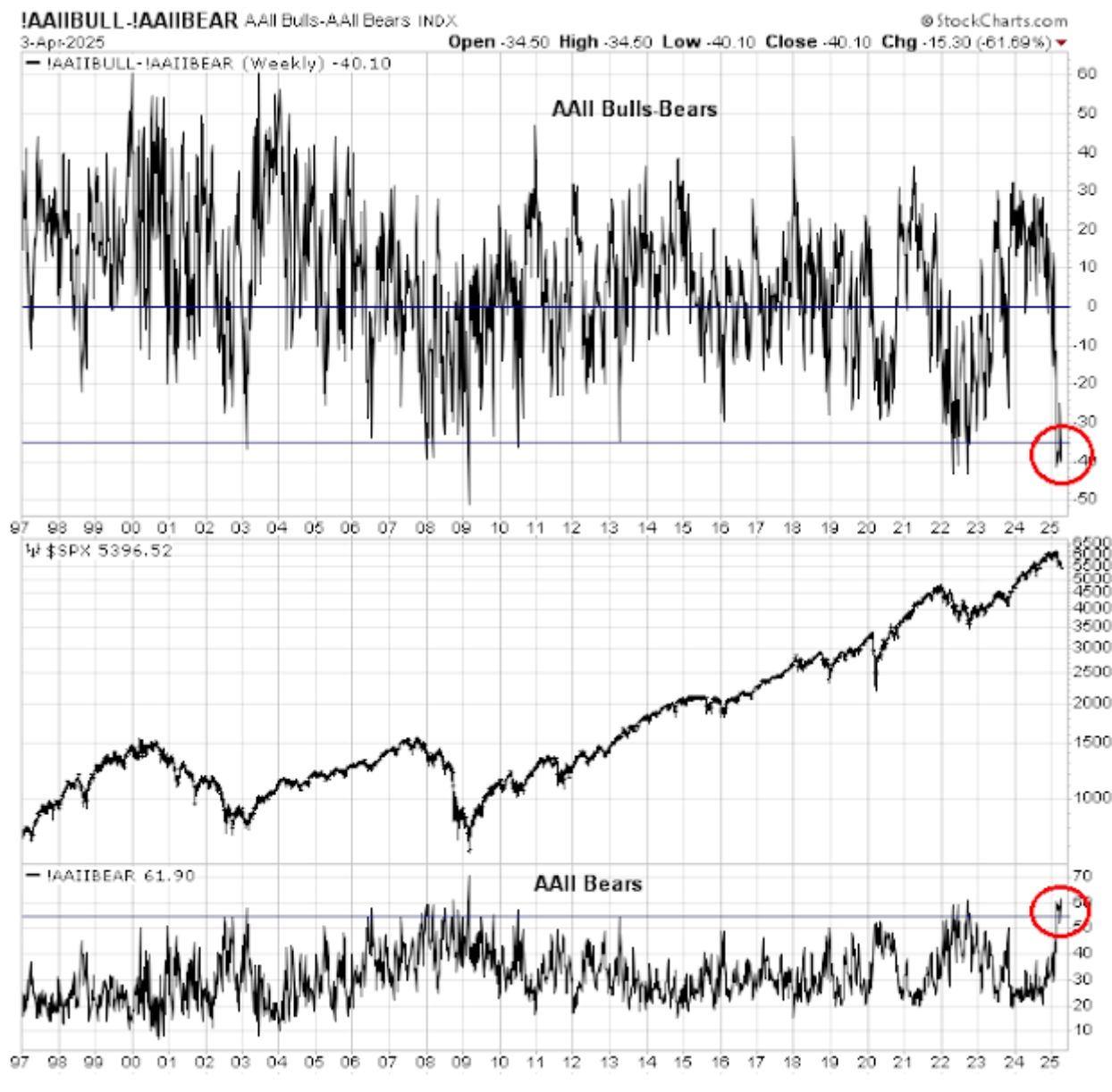

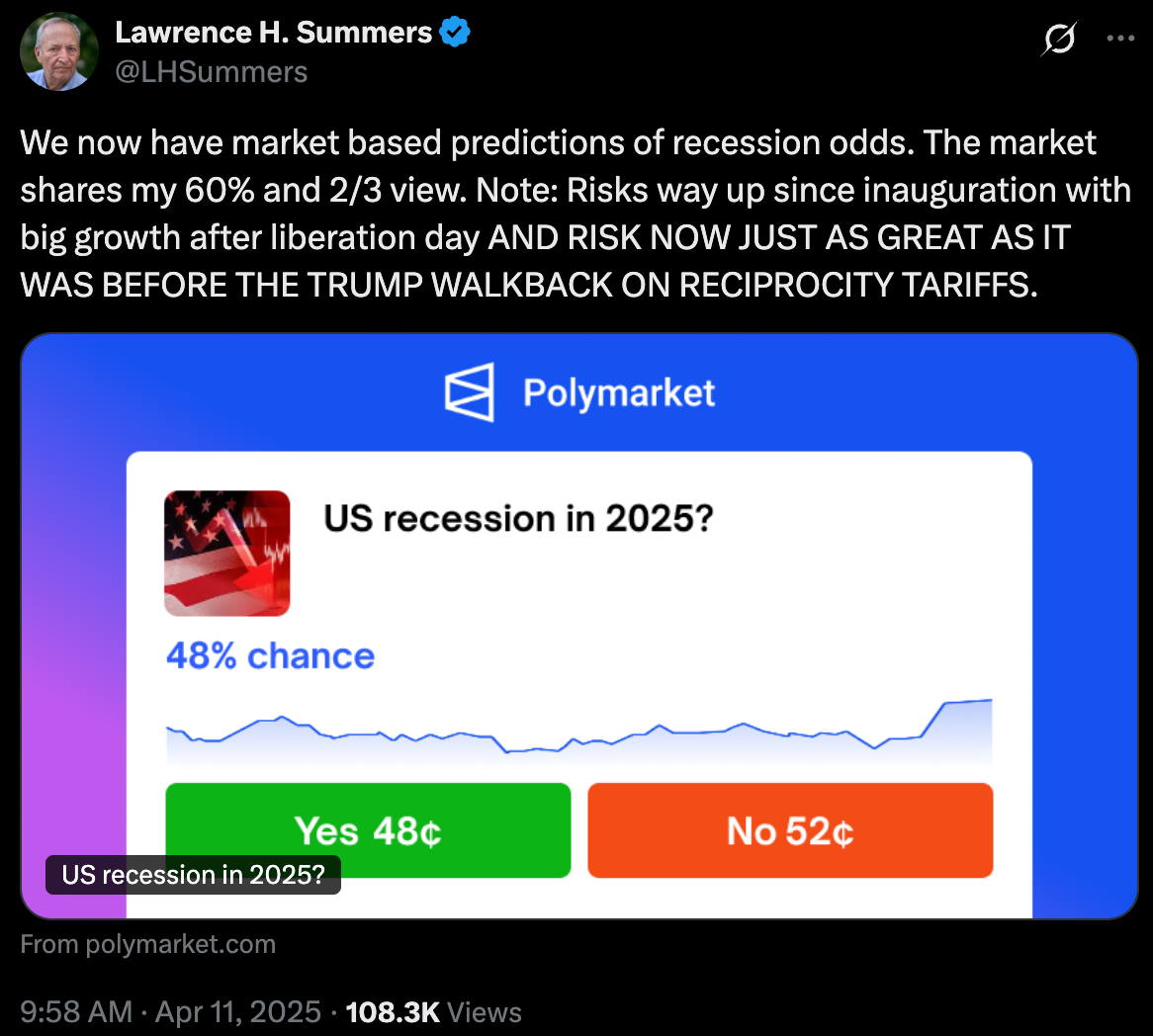

Outside of tariffs, the most important question for equities is whether the US economy is heading into a recession. Prominent financial figures have started to warn that the US is heading into an imminent recession, with betting markets placing 40% to 60% odds of one happening in 2025. Is this just a Wall Street scare tactic to convince the President to dial down trade aggression, or a genuine concern over the economic outlook? Our view is that it probably doesn’t really matter, as sentiment often frames reality, not the other way around.

Calls for a US Recession has Risen Substantially in Recent Weeks

Source: CNBC, X, Kalshi

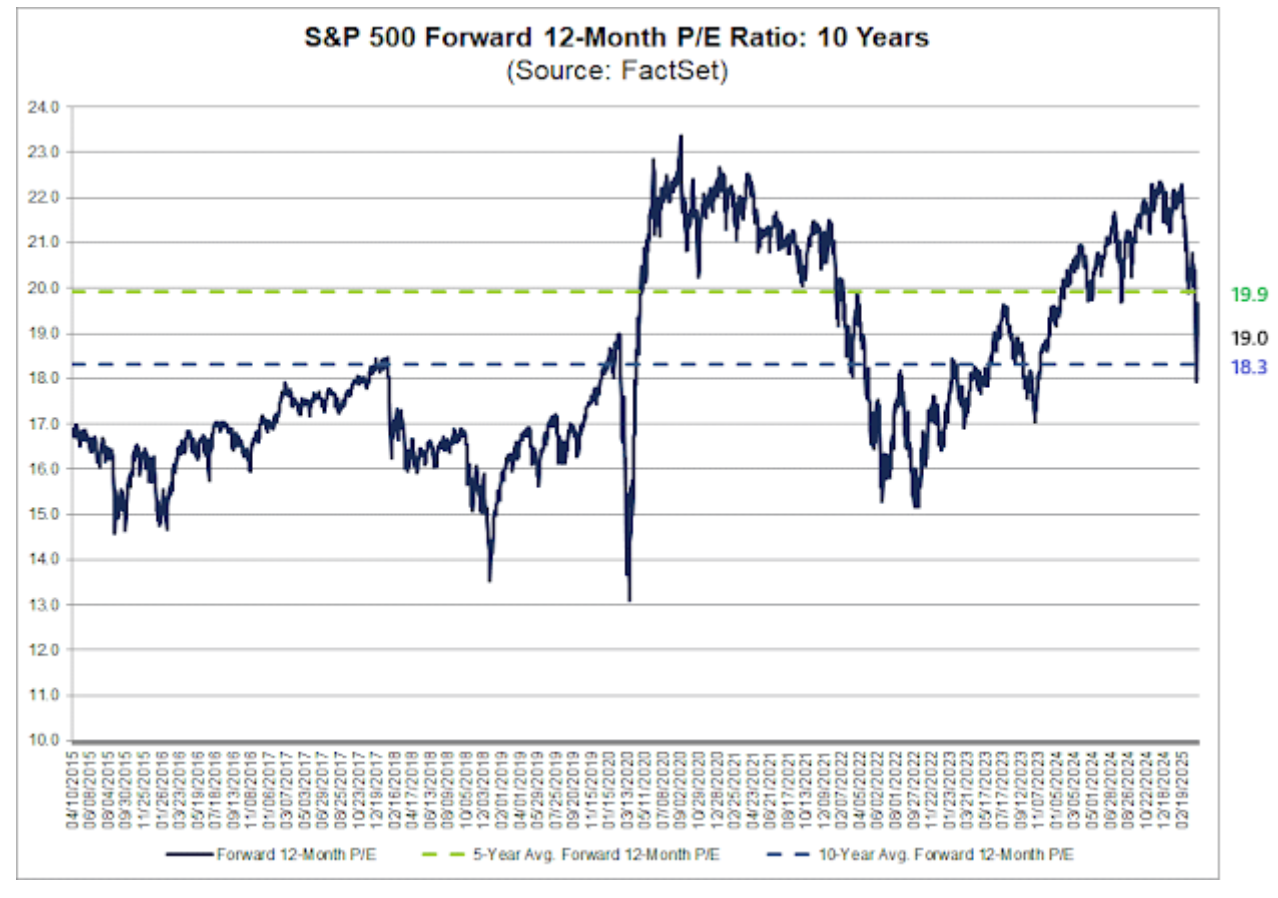

With US earnings season starting to kick into gear, valuation will be a focal point and any considerations of fair market value will depend on whether the economy falls into a recession. The current forward S&P 500 forward P/E ratio is at around 19, well within the historical range, and a further correction to the lower end range of ~15x would imply a further 25% to 30% downside from here.

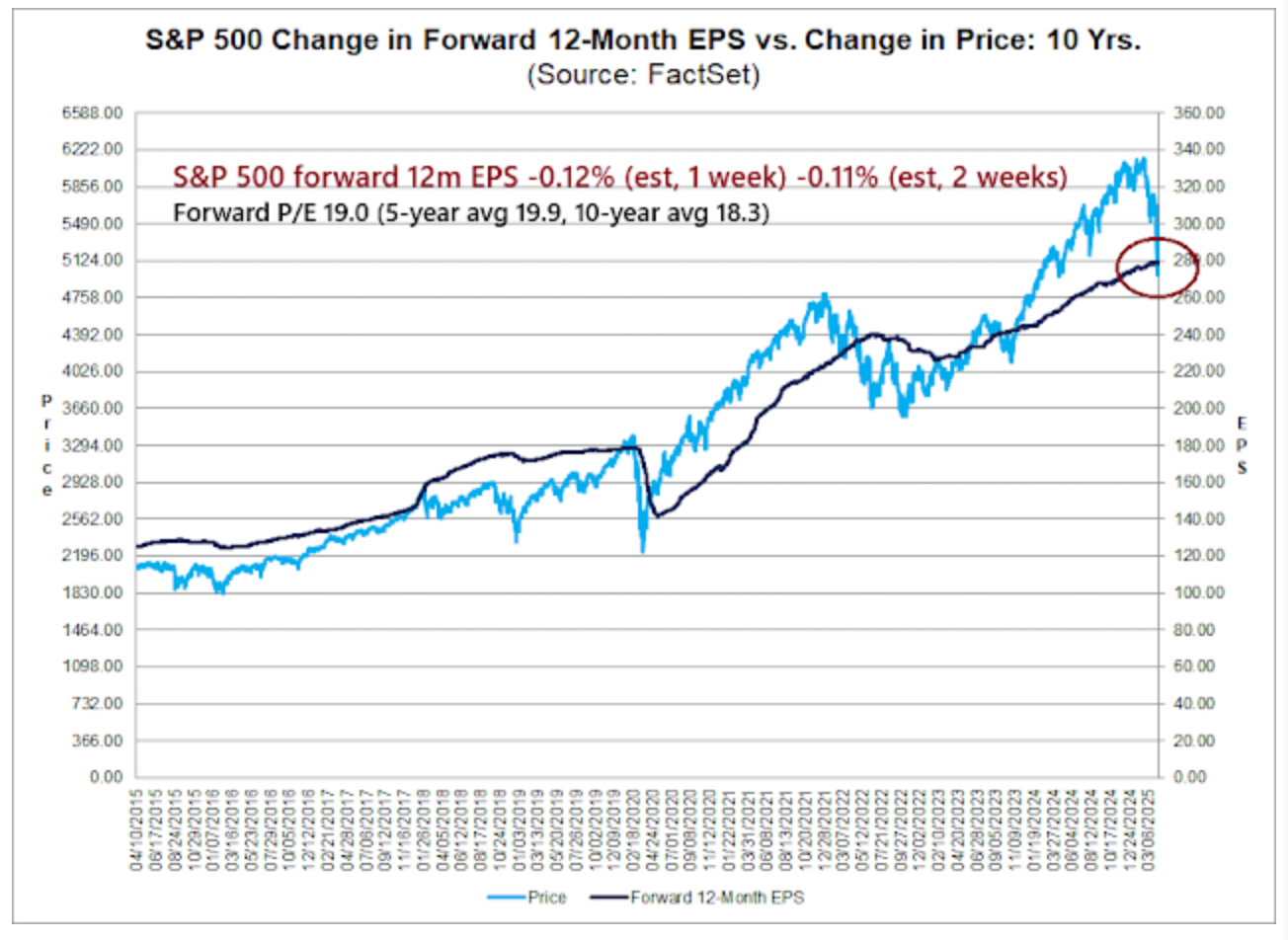

However, if a recession were to happen and corporate earnings dropped by a further -15% to -20%, the valuation floor for the SPX could fall into the sub-4000 area for the SPX. EPS revisions have already started to come down ahead of the earnings season.

Current SPX Forward P/E is Within the Historical Average… Assuming Earnings Stay Here

EPS Revisions have Already Started to Come Down Even Before a Recession has Started

Source: Cam Hui

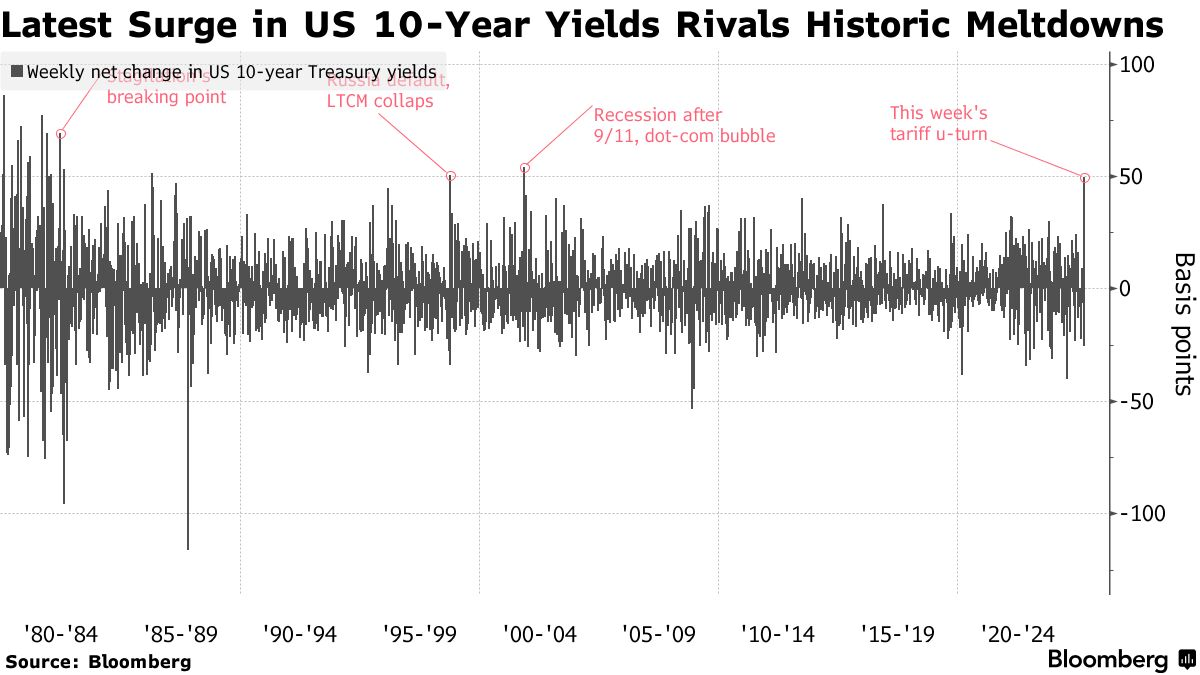

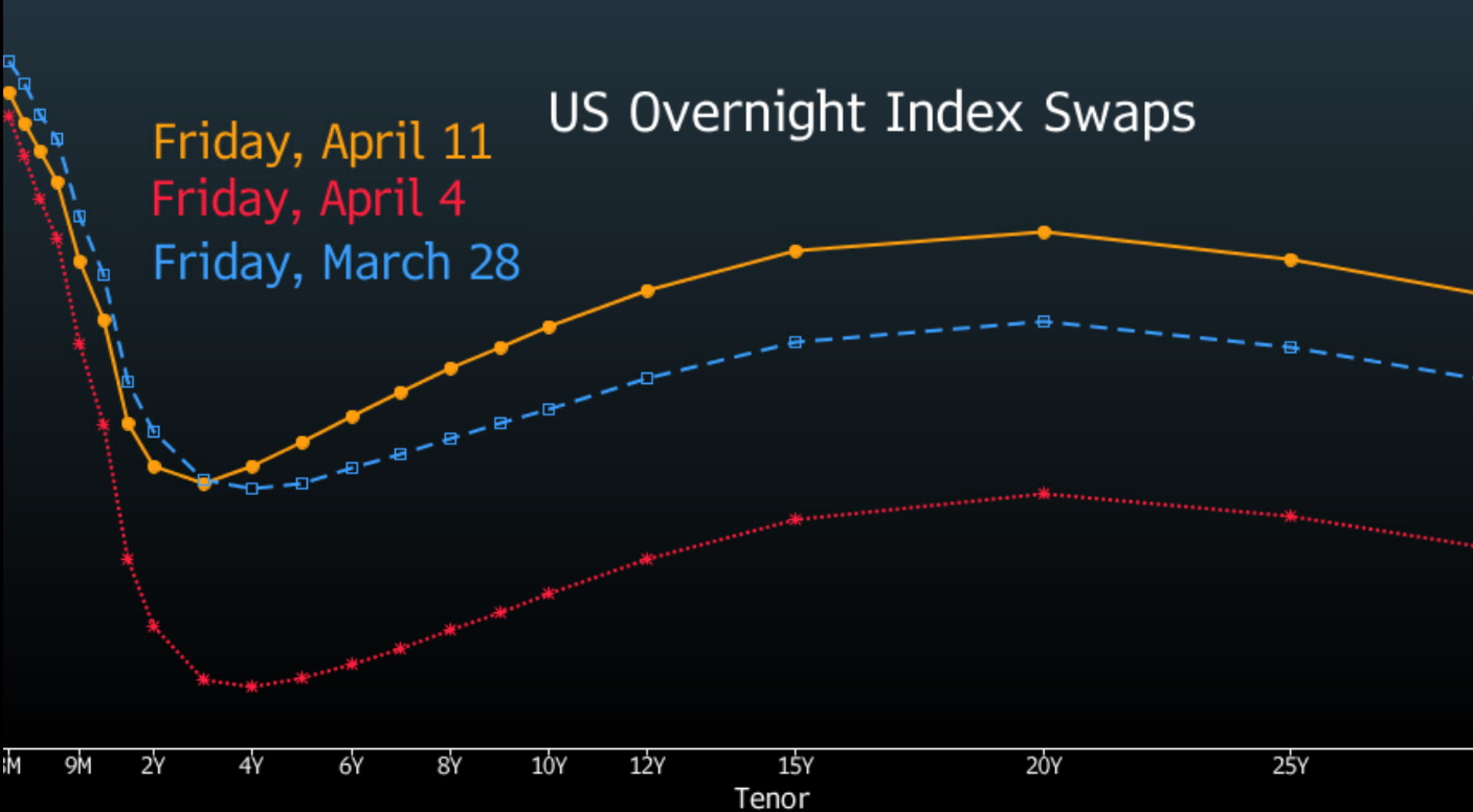

Away from equities, the biggest concern last week was actually over the dramatic sell-off in fixed income, calling into question whether Trump’s aggressive actions have damaged treasuries’ heralded status as a global safe haven. Treasury yields saw the largest weekly jump in over 20 years as concerns swelled over foreign central bank selling as a tariff response, with the supposedly Japan-led treasury selling from last Wed triggering Trump’s initial tariff compromise.

Concerns Over Treasury Yields Took Center Stage as Their Safe Haven Status was Called into Question

Source: Bloomberg, Citi

Bonds Markets Show Once Again Who’s Really in Charge

Source: Washington Post

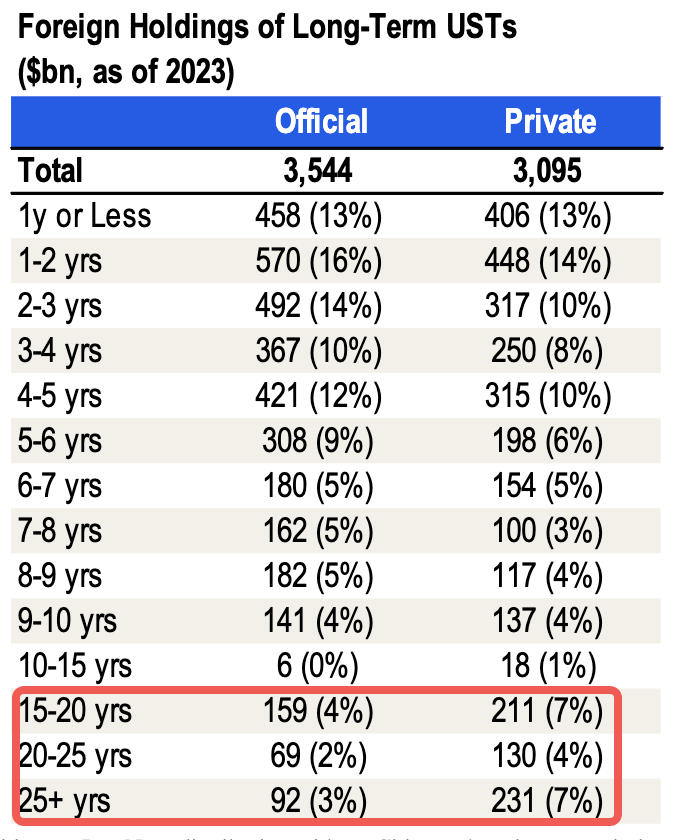

While there have been numerous suspicions and concerns about China aggressively selling USTs, we are skeptical of that view given that their holdings have already been dropping over the past decade, and that central banks actually own very little of the long-end (20-30yr bonds), which is where most of the recent damage was on.

Foreign Central Banks Actually Own Very Little Long-Dated Treasuries, Relatively Speaking

Source: Citi

Nevertheless, regardless of who did the initial selling (we suspect it’s Japanese life insurance companies and pensions), the divergence of USD and 10yr yields is concerning and flashes early warning signs. Capital account surpluses go hand-in-hand with current account deficits, so any normalization of the latter will mean less dollars being recycled into debt funding.

Are There Any True Safe Haven Assets Left in the World?

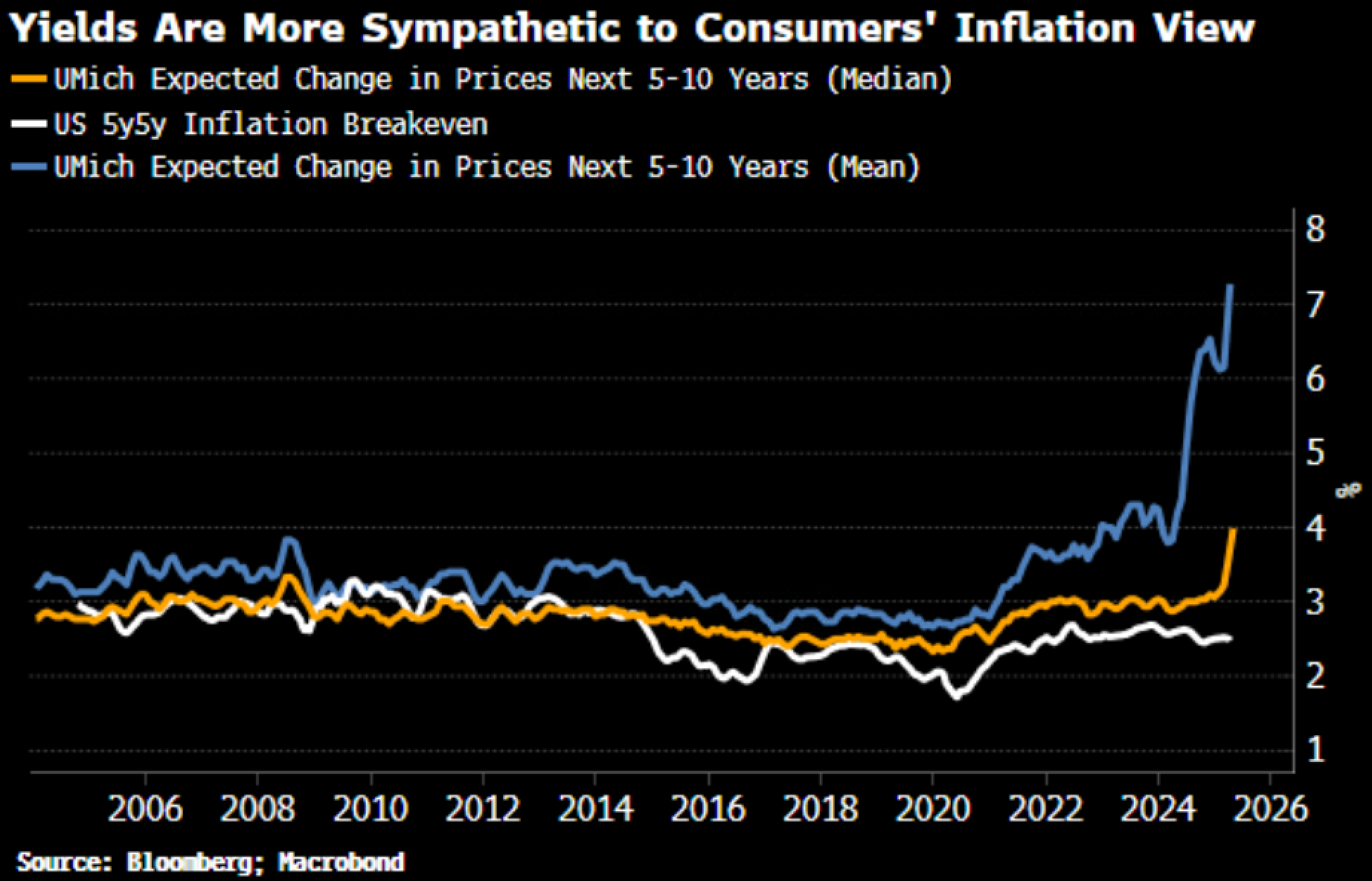

To add fuel to fire, a jump in UMich inflation expectations is making things tricky for the Fed and bond observers as consumers’ view of inflation is diverging with recent underlying data. Short-dated rate pricings have repriced higher (less cuts) in the past week as the market is questioning the Fed’s ability to stay dovish against inflationary headwinds from incoming tariffs. A rock and a hard place indeed.

Inflation Expectations are Starting to be Baked into Investor Expectations

With Fed Cuts Being Priced Out Despite a Weakening Economy

Source: Bloomberg

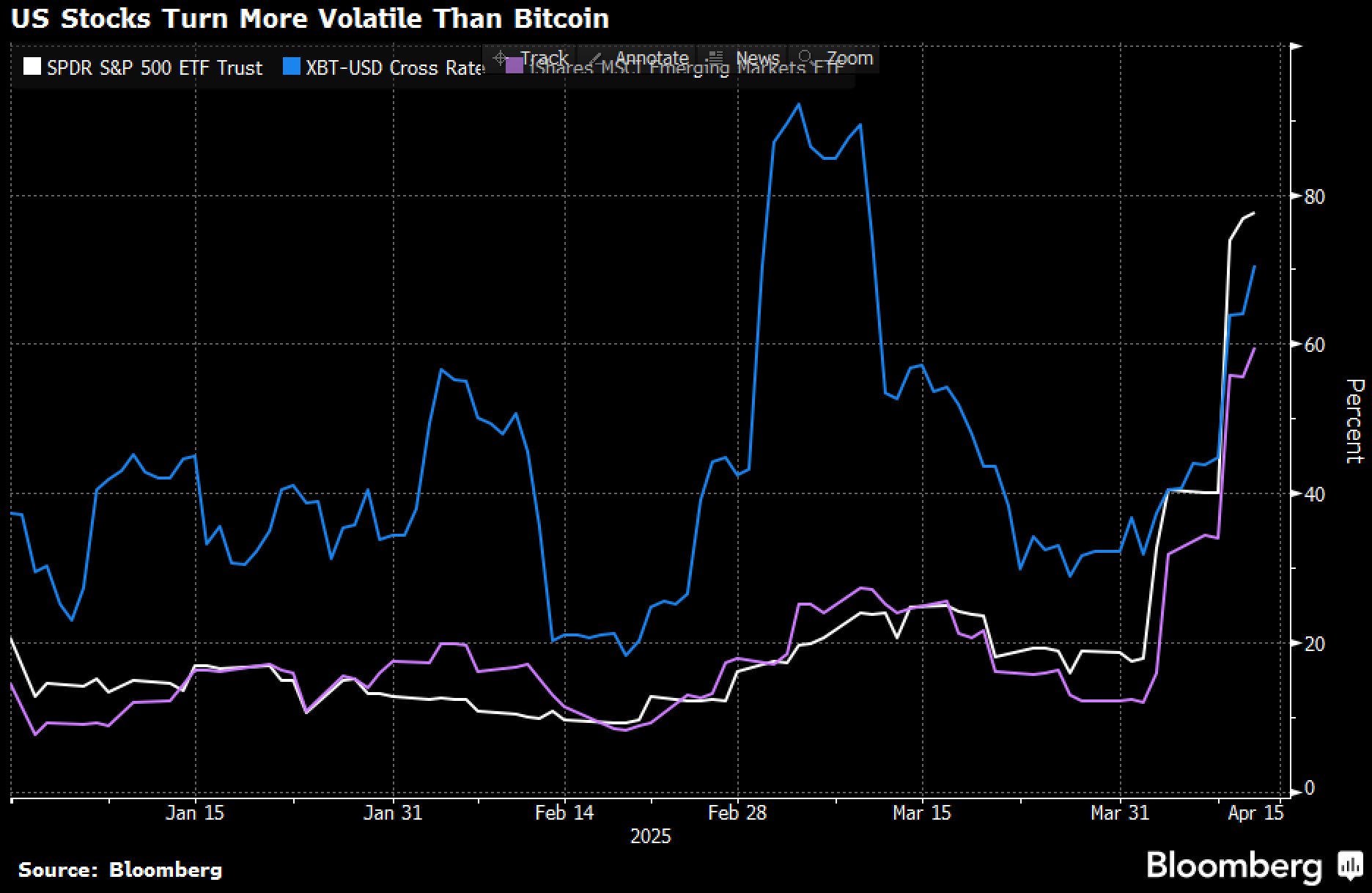

Ironically, crypto has been a benefactor from the recent shake-out, as equities have been realizing higher volatility than Bitcoin through the risk-off move. A beggar-thy-neighbour policy with tariffs has pushed spot gold to ATHs, with BTC finally regaining some of its long-lost ‘store of value’ narrative.

The BTC ‘Store of Value’ Narrative has Regained Some Traction in the Recent Move

Allowing BTC to Benefit from the Spot Gold Rally in the Past Week

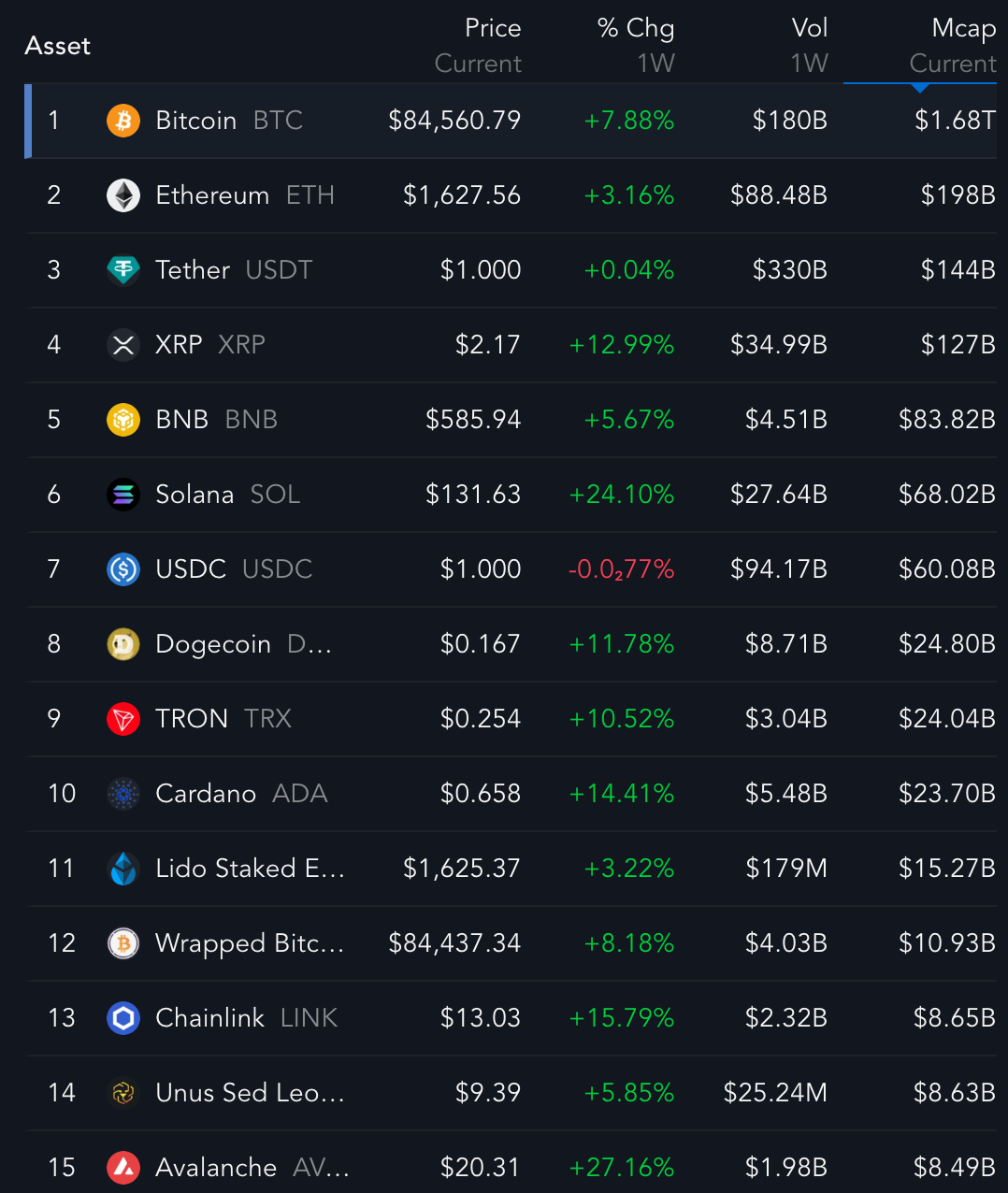

Chart technicals look good with BTC breaking out from its YTD trendline and looking to reclaim the 90-95k area as its next target. Furthermore, for the first time in months, memecoins and alcoins appear to be catching a bid once again, with a number of native-favourite memecoins seeing 100%+ gains over the past week.

BTC has Broken Out from Its YTD Trendline with Major Tokens Enjoying Double Digit % Gains Over the Past Week

Source: Messari, Bloomberg

Altcoins and Memecoins Have Been Enjoying a Surgence Over the Past 2 Weeks as the Crypto Rally Takes Hold

Source: Coingecko

Finally, on a longer-term basis, structural fundamentals continue to argue for higher long-term prices, with WSJ reporting that Binance is seeking to make a deal with the US and Trump’s crypto company in exchange for looser government oversight. Meanwhile, Bloomberg reports rising expectations for perpetual futures to be offered on US exchanges in the coming quarters, putting them on par with existing offshore offerings, dramatically increasing the secondary liquidity and leverage available on regulated US venues as mainstream adoption continues.

WSJ Reports That Binance is Seeking to Make a Deal in the US and with the Trump Family

Source: WSJ, Bloomberg

Better Late than Never – Perps Coming to a Regulated US CEXs Soon?

Source: Bloomberg