It seems like everyone is getting a job this month…

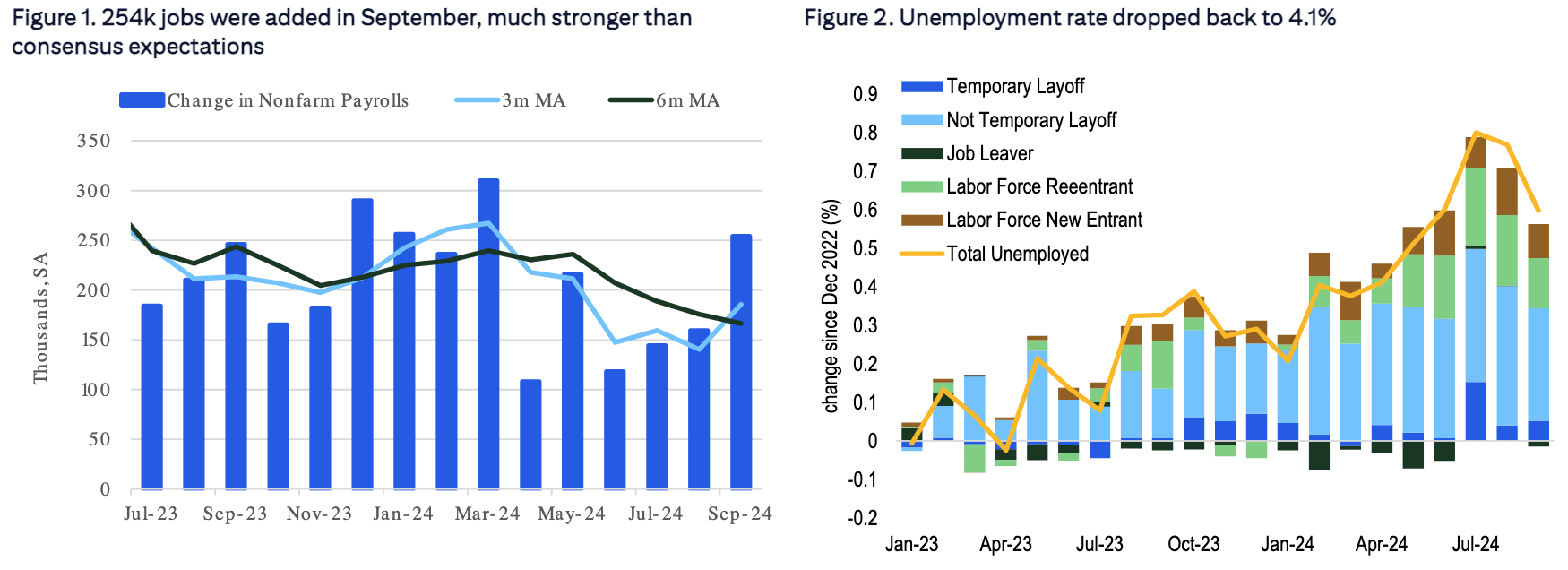

A significantly stronger than forecast NFP raised significant questions on the Fed’s wisdom to cut 50bp last month, as the US economy added 254k new jobs (vs 150k expected), with the unemployment rate falling back down to 4.05% and average hourly earnings staying robust.

NFP Blew Out All Wall Street Expectations

Source: Citi

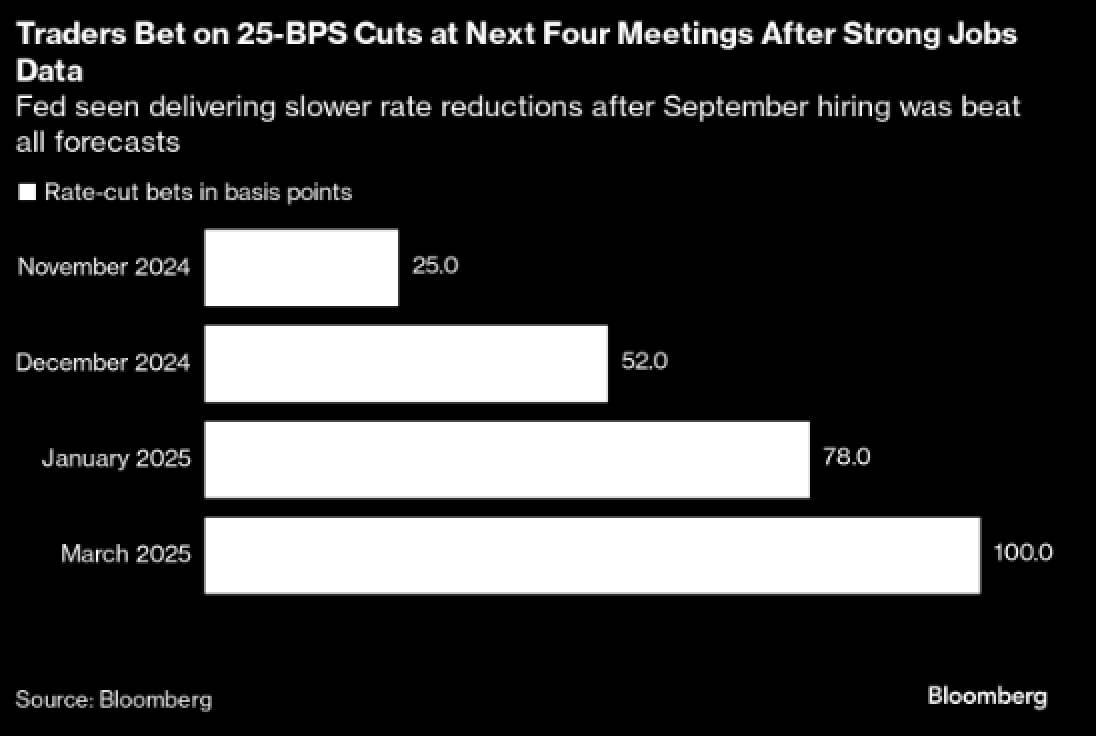

The fixed income reaction was furious – short-dated treasuries jumped 20bp as the yield curve bear flattened aggressively. 10y yields broke upside resistance at 3.93% and looks to be on the way to print above 4%, while terminal rates spiked 25bp to nearly 4.25%, and rate cutting odds fell back to single 25bp cuts over the next 4 FOMC meetings.

10y Yields Appear to be Heading Back Above 4% in the Near Term

Source: Bloomberg

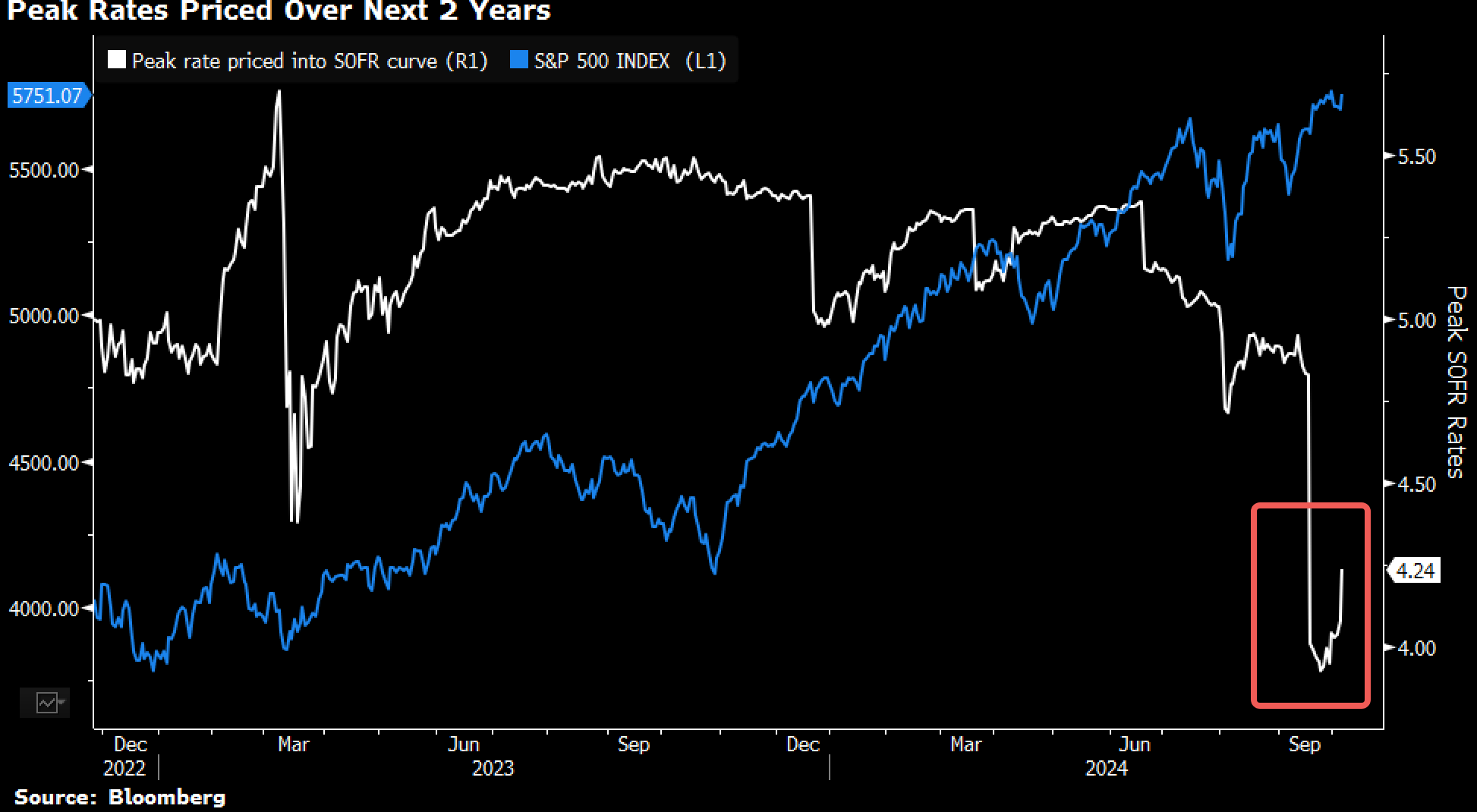

US Rate Cutting Odds Dropped Significantly After the Strong NFP Print

Source: Bloomberg

While fixed income struggled, the USD strengthened against all major currencies, and in particular the JPY, after the incoming PM Ishiba appears to be toeing the party line to maintain an easy monetary policy along with new stimulus package plans.

USDJPY Rebounded Aggressively Following the Strong NFP and Promises from the New PM to Maintain an Easy Monetary Policy

Source: Reuters

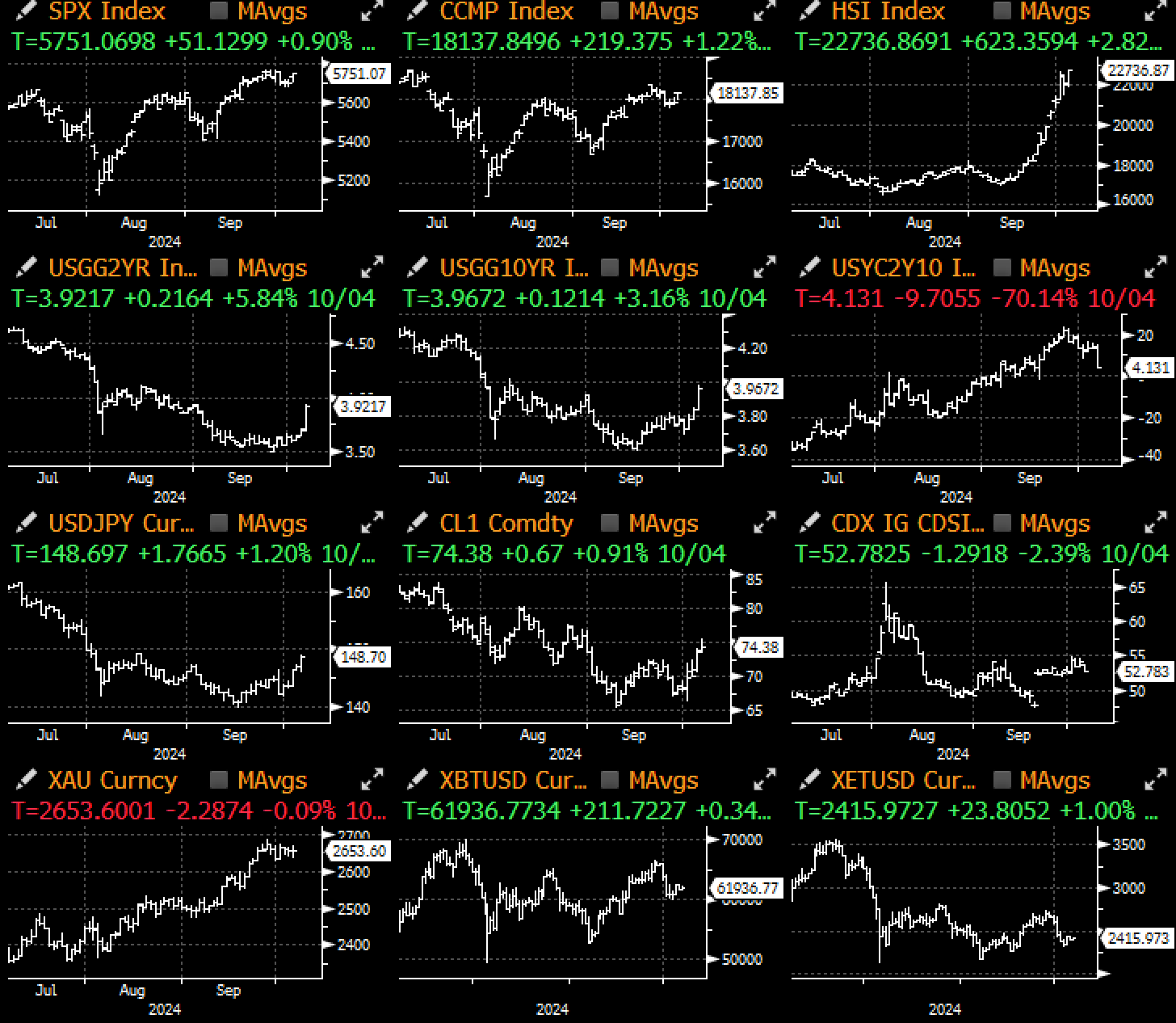

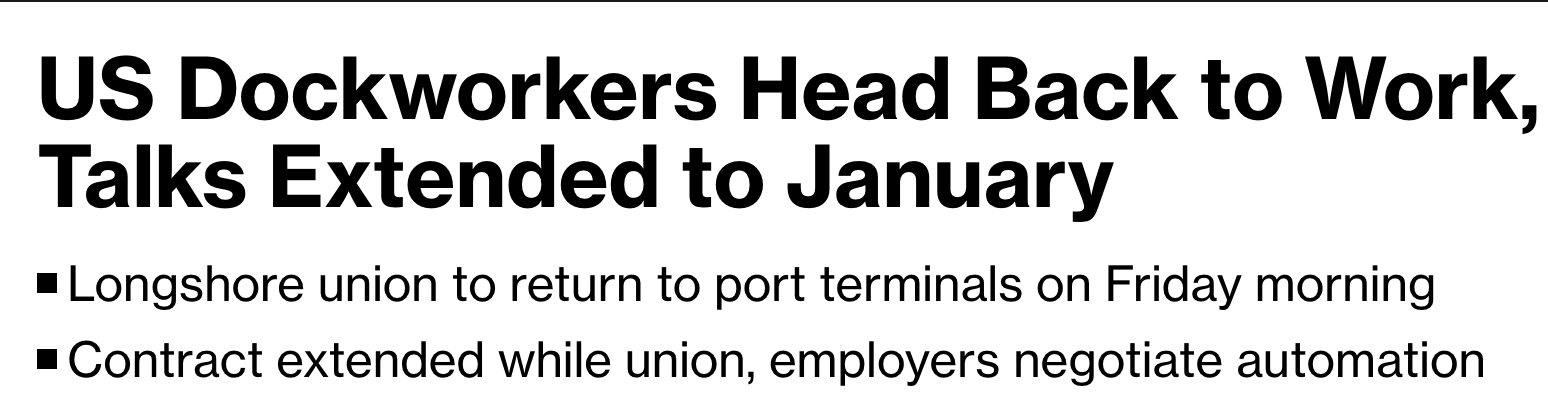

Unsurprisingly, global equities enjoyed another strong week with most indices in the green led by an outperformance in Tech, as the strong economic data, friendly central bank support, and even a timely halt to the US dockworkers strike to give investors full latitude to stay risk-on in the meantime. Furthermore, a record breaking $1.4bln in China inflows (via the FXI ETF) has reignited animal spirits in the world’s 2nd largest economy, adding further fuel to fire in the ongoing risk melt-up.

It’s Getting Increasingly Tough to be a Macro Bear…

Source: Bloomberg

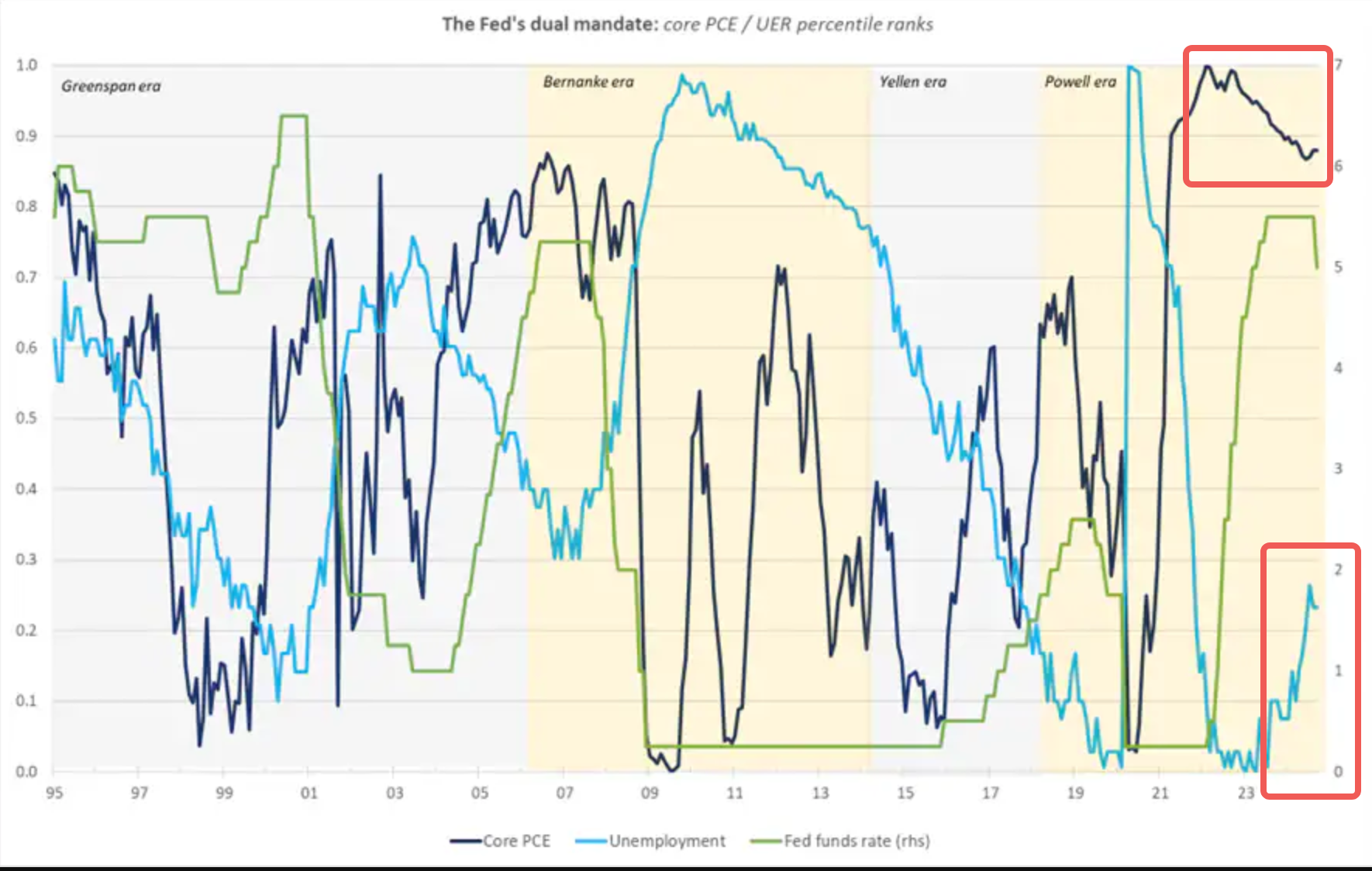

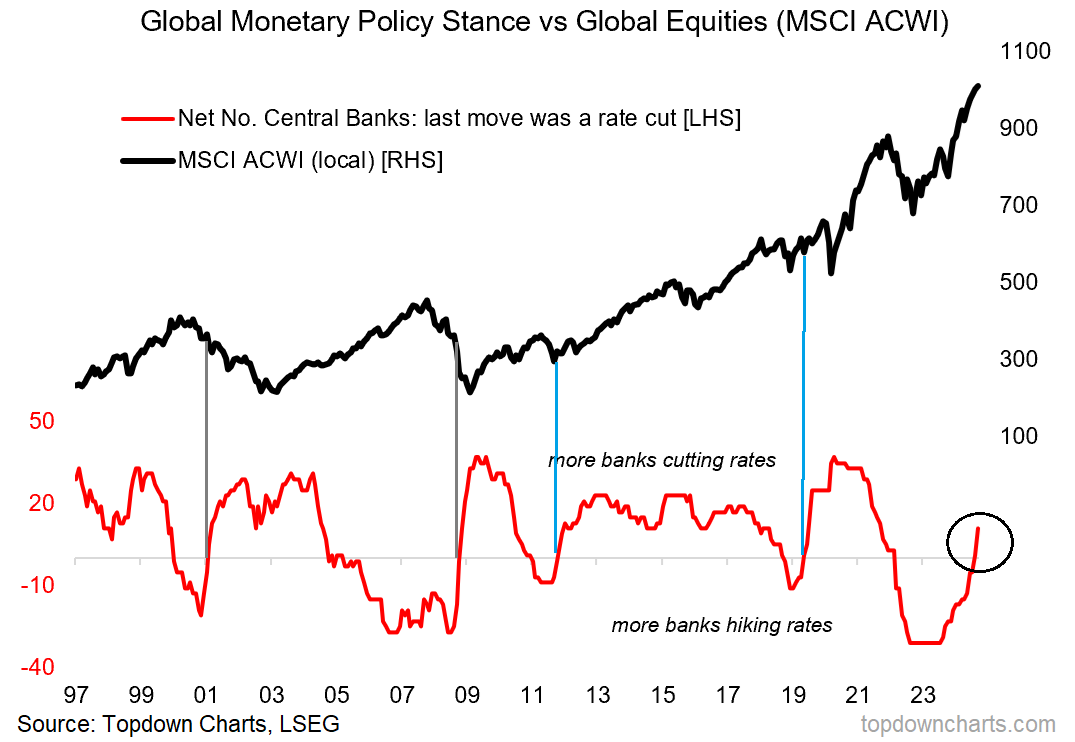

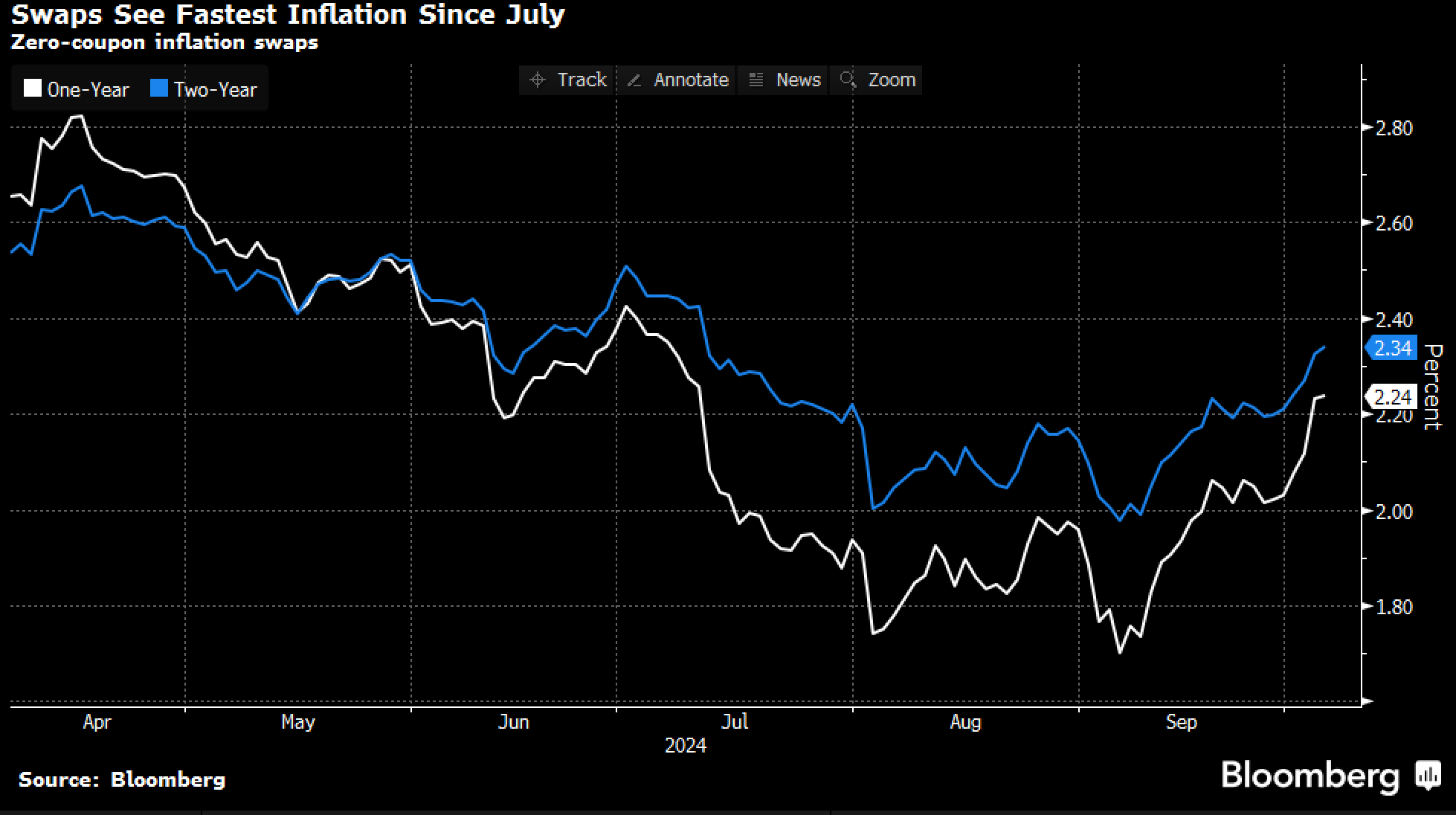

In retrospect, Powell’s 50bp move is even more dovish when viewed in the historical context, with both inflation and unemployment remaining close to historical extremes in terms of strength. On a standardized basis, PCE is still hovering at around the top 15%-percentile levels while unemployment remains near decade lows. Furthermore, similar to 2020, global central banks are cutting rates while stocks remain on a one-way uptrend, which is causing inflation expectations to finally start rebounding higher over the past few weeks.

Did the Fed Really Cut 50bp with Core PCE at Decade Highs and Unemployment at Decade Lows (on a Standardized Basis)?

Source: Bloomberg

Central Banks are Cutting Rates Again With Stocks Remaining on a One-Way Melt-Up Trend

Will the China Stimulus Plus US Economic Rebound Lead to an Unwelcomed Return of Inflation?

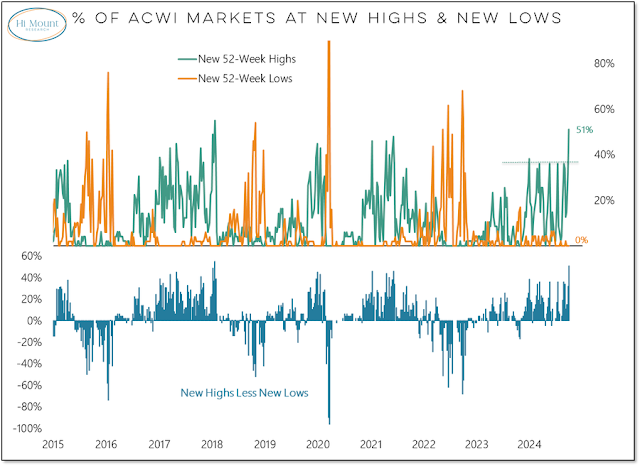

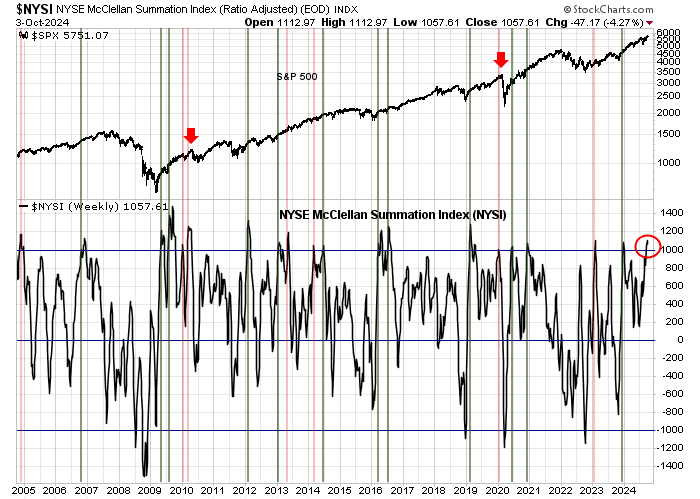

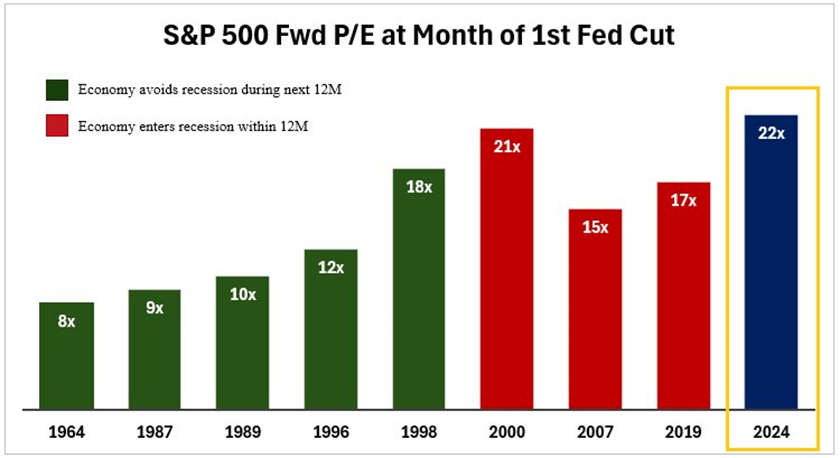

Technically speaking, charts are looking very positive for US equities, with indices seeing new 52 week highs at a pace rarely seen over the past decade, and other momentum indicators also signaling a breakout higher. Valuations are undoubtedly rich, with SPX forward multiples trading at the highest levels during the start of the Fed easing cycle, but since when did valuations matter for price action anyway?

US Equity Technicals Look Very Bullish and are Signaling a Further Push Higher

Source: Cam Hui

Valuations are High… But Does It Matter?

Source: Cam Hui

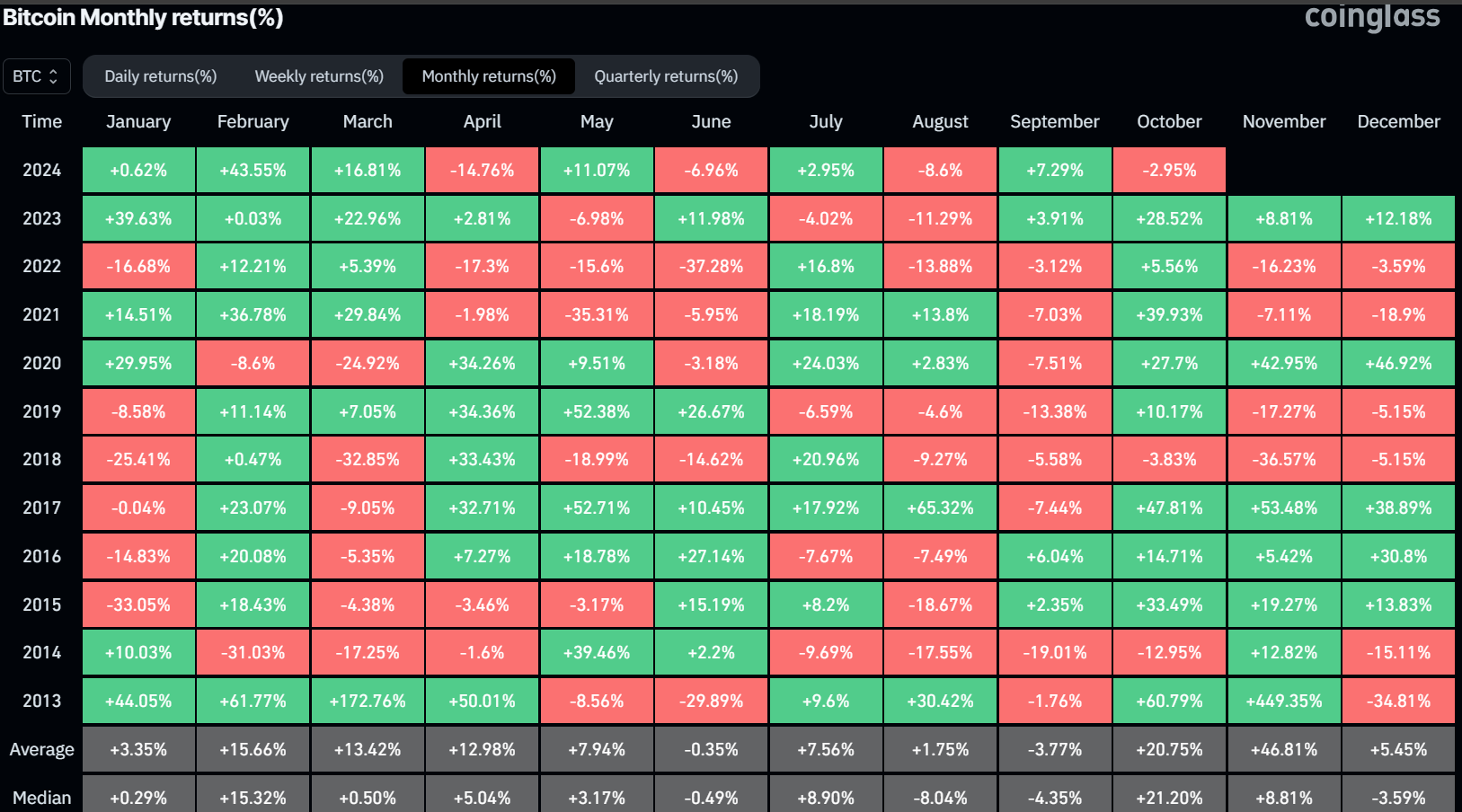

While the rest of the macro complex are celebrating new highs with the latest soft-land scenario, crypto has suffered mightily and is up to its worst October start since 2019, with BTC trading as low as 60k to begin the month. The rest of the altcoins didn’t fare much better (-10% on the week), as some of the local FOMO energy must be losing out to the surging in A-shares. In fact, Coinglass data reported nearly $500mm in long-futures liquidation over the first few days of October.

So Much for Uptober… But the Month is Still Early

Source: Bloomberg

Crypto is Seeing Red Everywhere You Look

Source: Messari

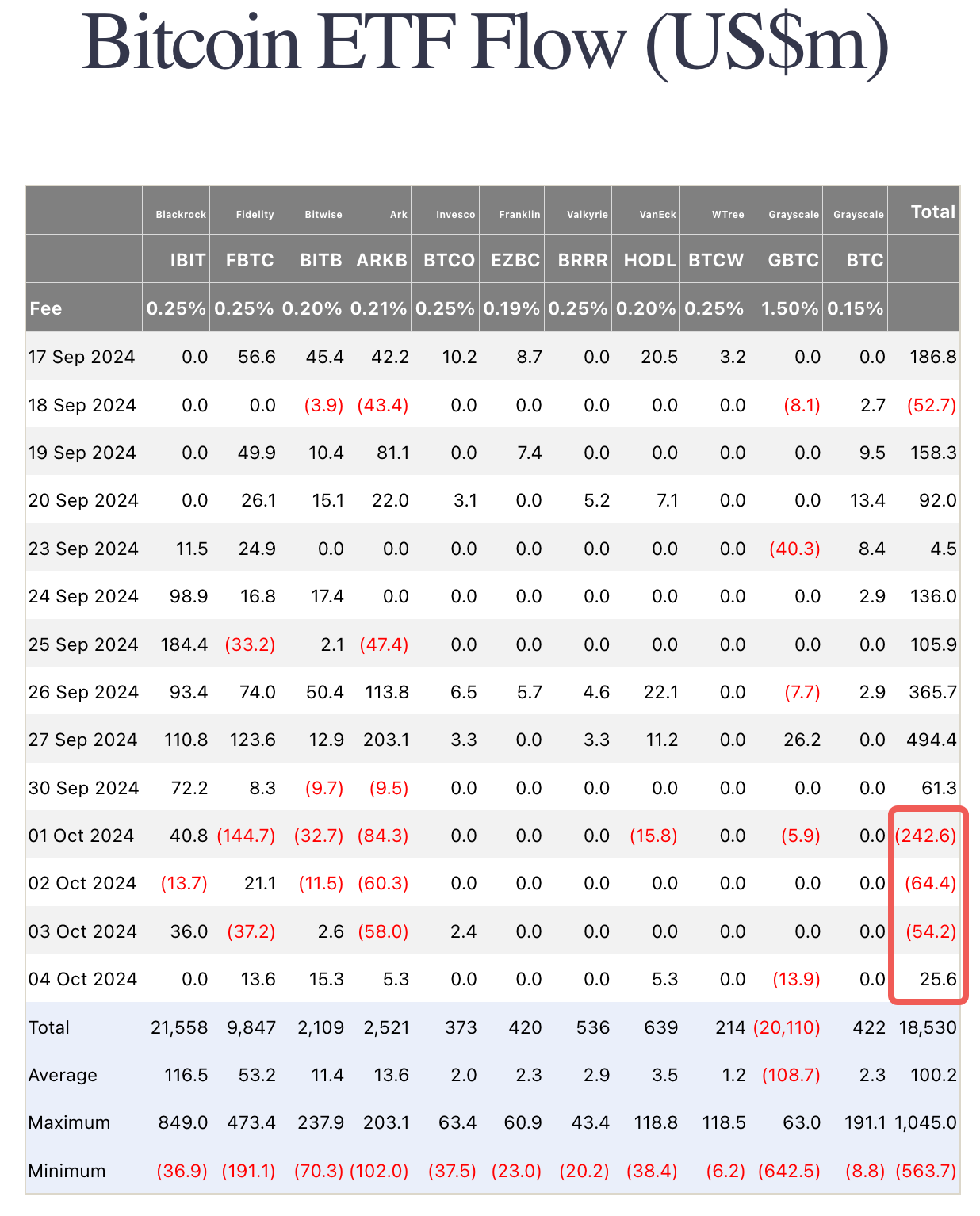

Markets Saw Significant Long Liquidiation in Early October

Source: Coinglass

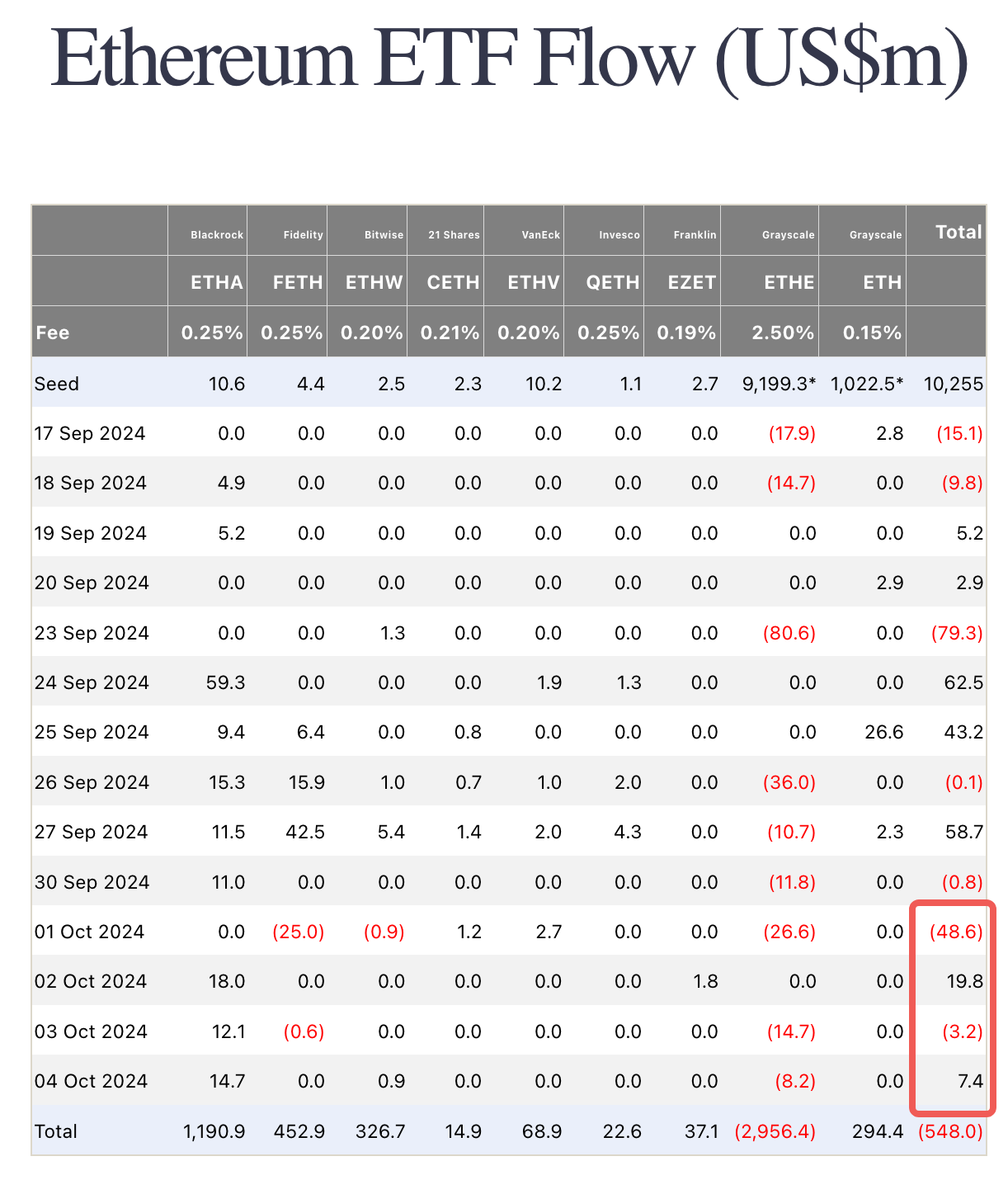

ETF inflows have been subdued with a slight recovery on Friday, though the overall trend remains concerning. Furthermore, crypto’s inability to hold on as a ‘risk-hege’ over the latest Middle East tensions have not been noticed, and we will function like a high-beta asset until further notice.

ETF Inflows Remain Disappointing

Source: Farside Investors

Nevertheless, we do expect the combination of easy monetary policy, strong risk-on sentiment, and a rebound in Trump winning odds (given Kamala’s poor handling of the hurricane recovery efforts) to present a strong Q4 for crypto prices in general. While the journey will likely be choppy, we are encouraged by the recent price action which has seen higher lows on each subsequent sell-off, and will remain patient to wait for new highs on BTC before the end of the year. We are still early in October after all!