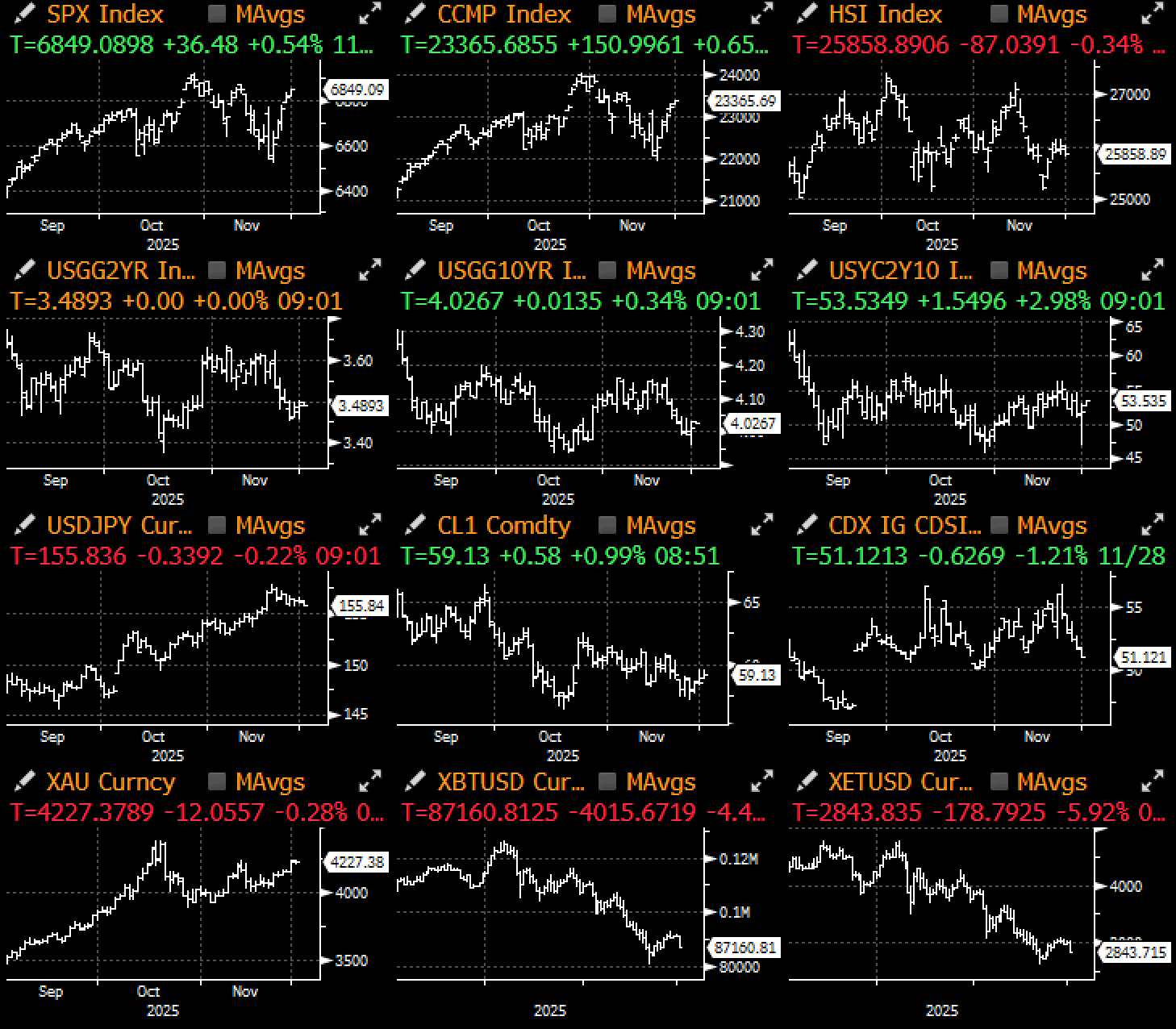

Well… The Last Week was fun While it Lasted…

Source: Bloomberg, Messari

Well that was fast. After a strong risk-on rally to close the week, crypto prices cratered hard to start December, with BTC sliding below $87k on yet another stop-loss run being driven during the thin Asia morning session.

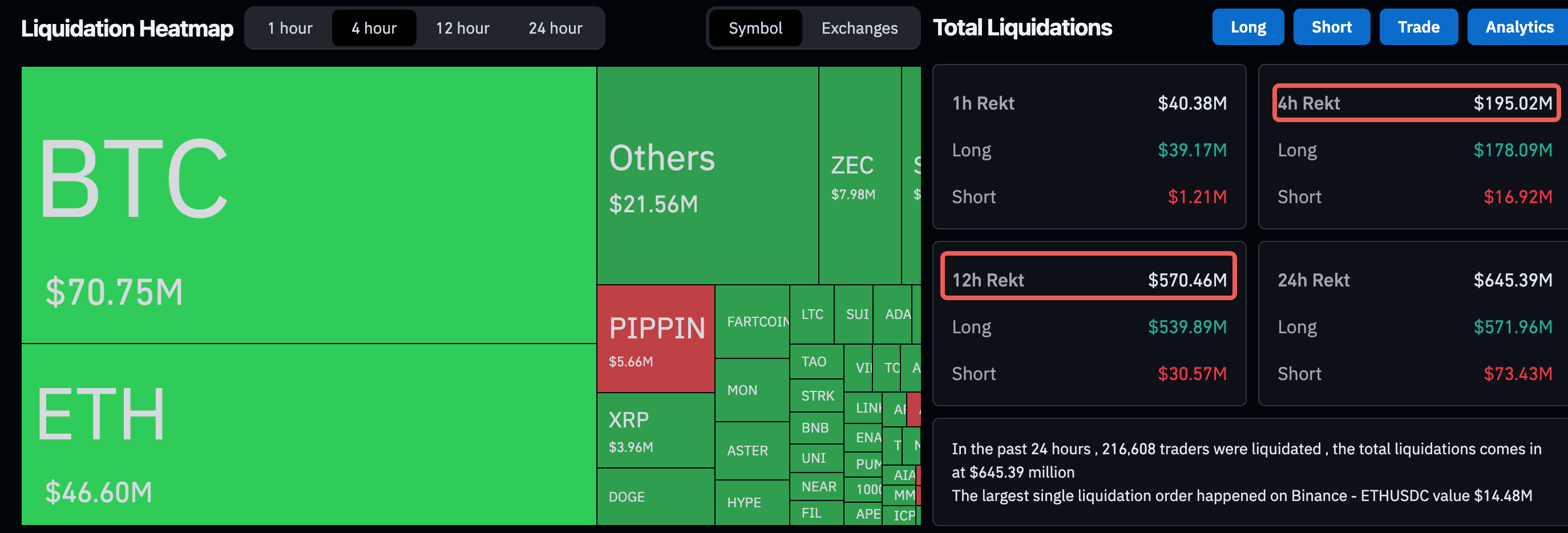

Crypto Saw ~$200M in Longs and ~$150B in Market Cap was Wiped Out in Crypto Over the Past 4 Hours

Source: Coinglass

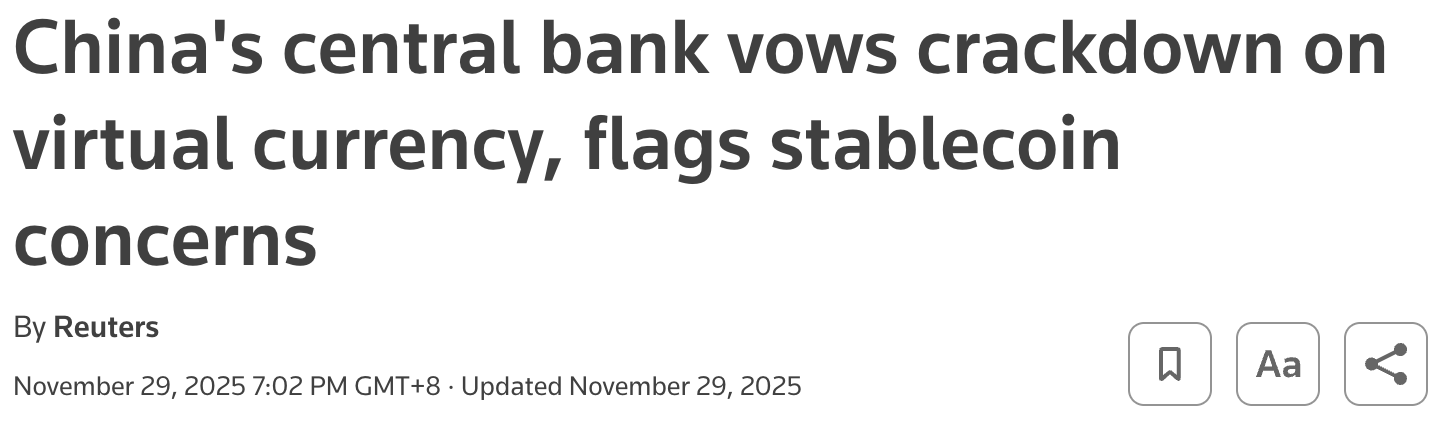

While it’s hard to blame a specific trigger, overall risk appetite remains feeble after the Oct-Nov washout, and worsened by a number of negative headlines that have surfaced over the past few sessions. With yet another DeFi hack on a OG protocol (Yearn staking), a DEX terminal abandoning its much anticipated launch over tough market conditions (Terminal Finance), OG Arthur Hayes openly ‘FUD’ing the recent Monad ICO (99% downside), a S&P ratings downgrade of USDT to ‘weak’ (poor disclosures), and the PBoC reiterating its cautious stance on crypto trading & stablecoins, it’s probably fair to say that we remain firmly in bear market territory until further notice.

I Guess Crypto Didn’t Get the Memo on Being Thankful During This Festive Season…

Source: Reuters, Cointelegraph

BTC/ETH Implied Vol has Retraced, But Put Skews Remain Heavily Bid vs Calls for <1 Month Tenors

Source: SignalPlus

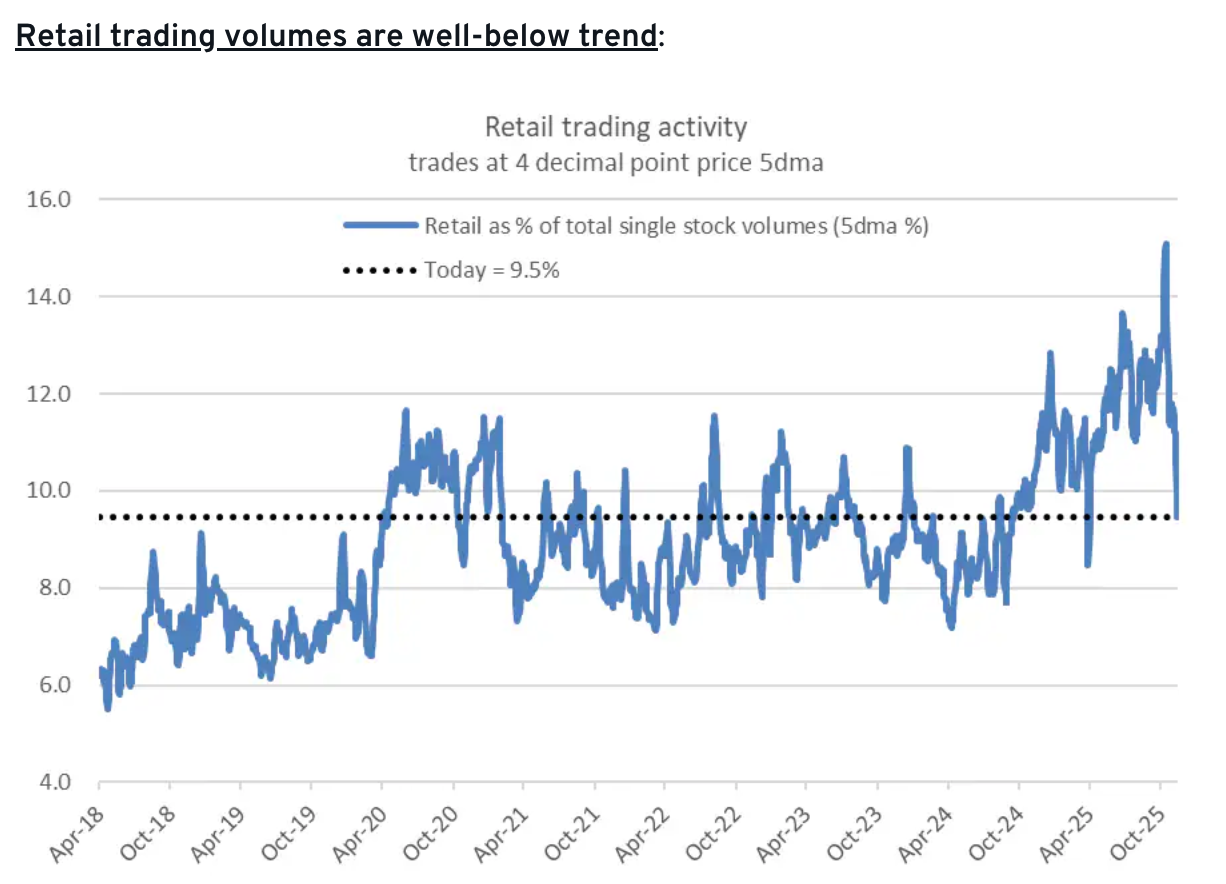

Over in equities, the SPX rallied by 3.7% last week led by semis (+5.4%) and retail (+4.7%), with retail favourite stocks making a strong week on week come back despite an overall drop in retail trading volumes.

Retail Favourite Stocks Made a Strong Comeback Last Week Despite a Drop in Overall Volumes

Source: Citi

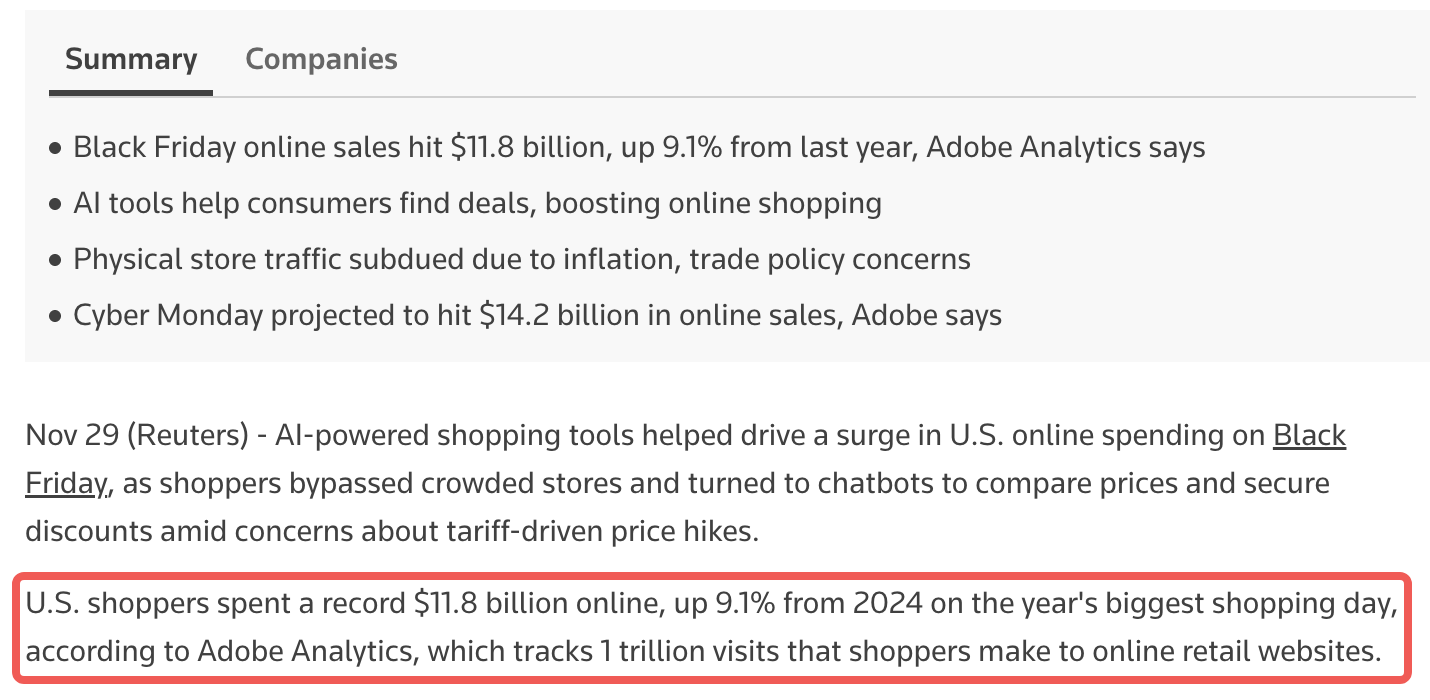

Furthermore, early indications of Black Friday sales suggest that we’ve hit another record, with online sales hitting a record of nearly $12bln (+9% YoY), and Cyber Monday projected to bring in another $14bln in revenues. US consumption appears to remain robust as of now.

Black Friday & Cyber Monday Hit Another Record Weekend as US Consumption Remains Strong

Source: Reuters

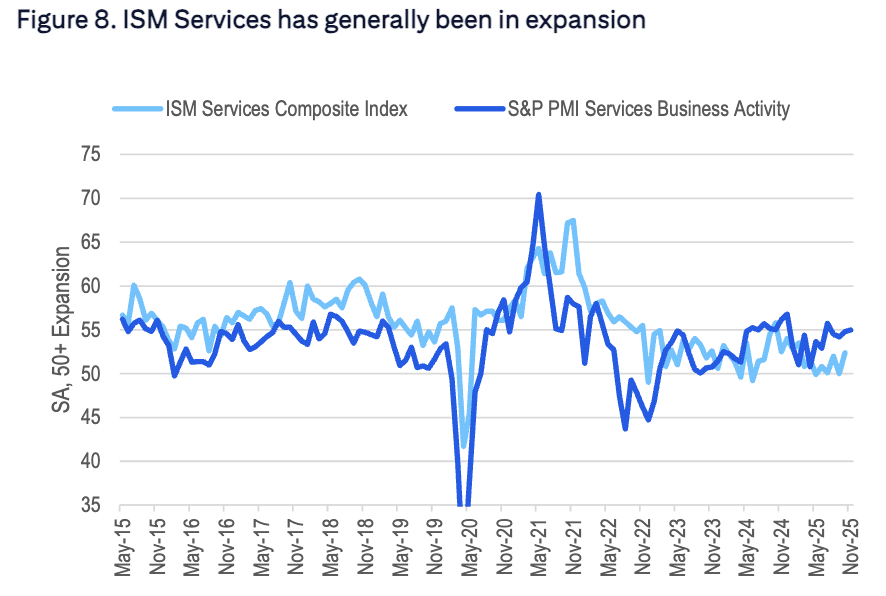

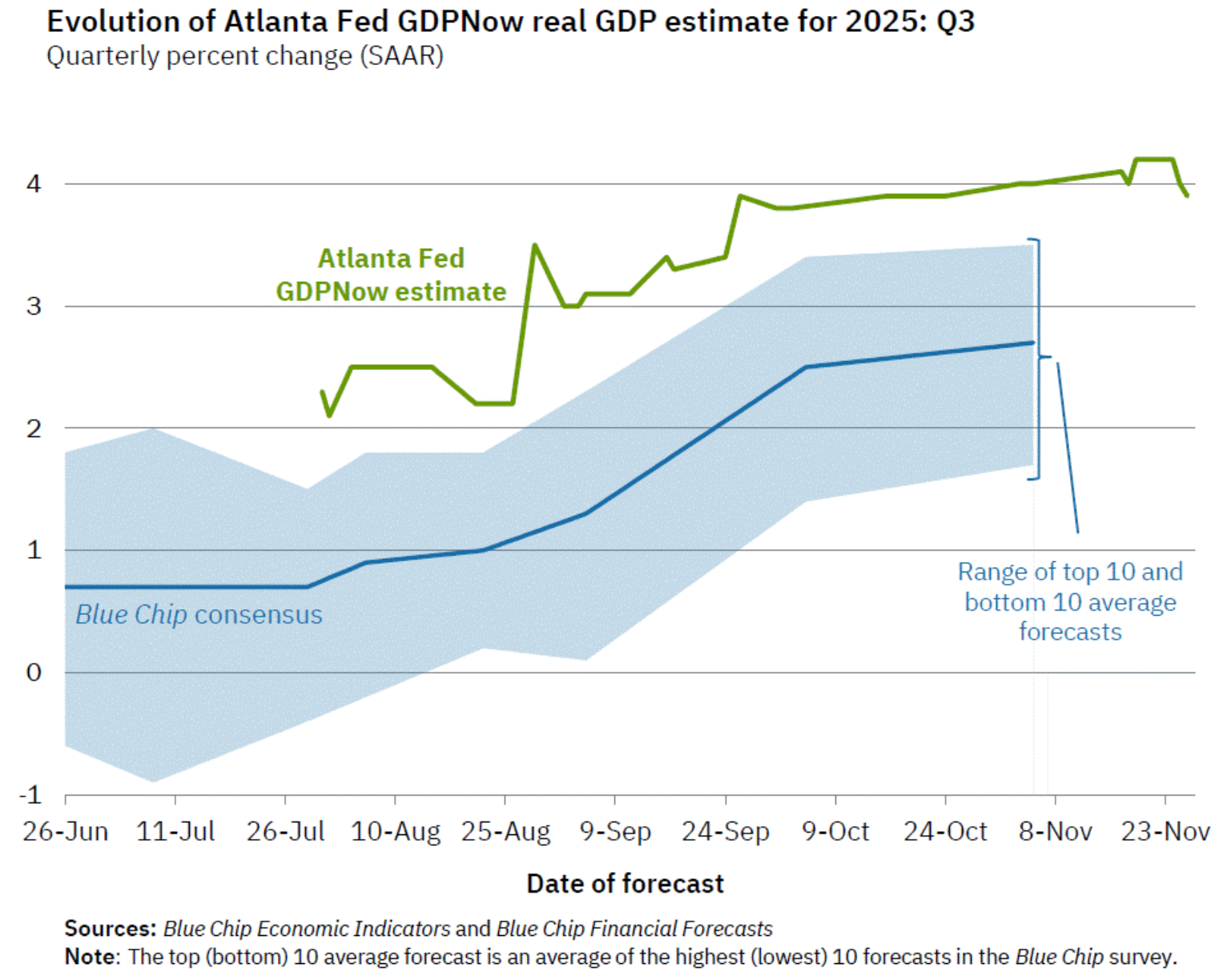

Outside of holiday sales, we’ll have a decently busy economic calendar with ISM, ADP, Claims, PMIs, and UMich confidence on deck this week. Despite all the noise, PMIs have been grinding at a healthy expansion range of 50-55 since 2022, while Atlanta Fed’s GDPNow continues to call for an above Wall-Street growth rate as the economy remains in good shape.

US Economy Remains in Good Shape by All Account

Source: Citi, Atlanta Fed

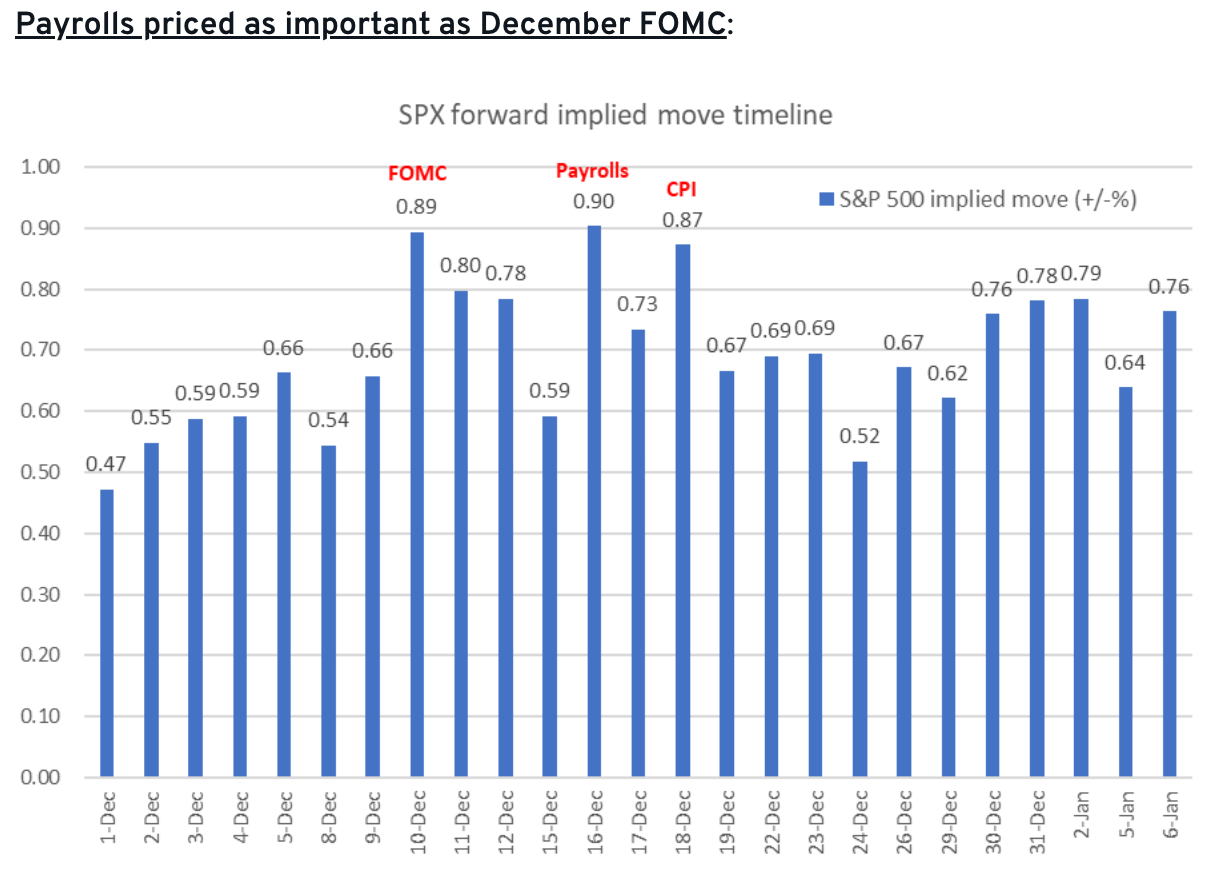

The most important econ dates for the rest of the year will be over the next 2 weeks, with FOMC on the 10th, followed by the delayed NFP on the 16th and CPI on the 18th. Furthermore, it’s worth nothing that there’s basically no tier-1 economic data that will be released between here and the FOMC date, so the ~100% chance of a Fed cut is basically baked in, as the Fed is not prone to surprise market odds, and focus will be on the guiding language for the 2026 trajectory, rather than the rate decision itself.

Specifically, we’ll look for the Fed to comment on their increasing confidence in receding inflation pressures versus weakening labour markets and tightening market conditions to justify a ‘dovish cut’, and vice versa the other way. There will also be scrutiny on the minutes on ‘how many’ participants preferred to keep rates unchanged as a dissent, especially in light of the yet-to-be-released NFP and CPI reports, and how Powell responds to the inflation gap vs unemployment gap questions during the Q&A. We’ll cover more on the Fed meeting later as we get closer to the event.

There are No Significant Data Releases Before the FOMC on the 10th, Suggesting that the ~100% Chance of a Dec Rate is Pretty Much Baked and Priced-In

Source: Citi

Good luck & good trading!