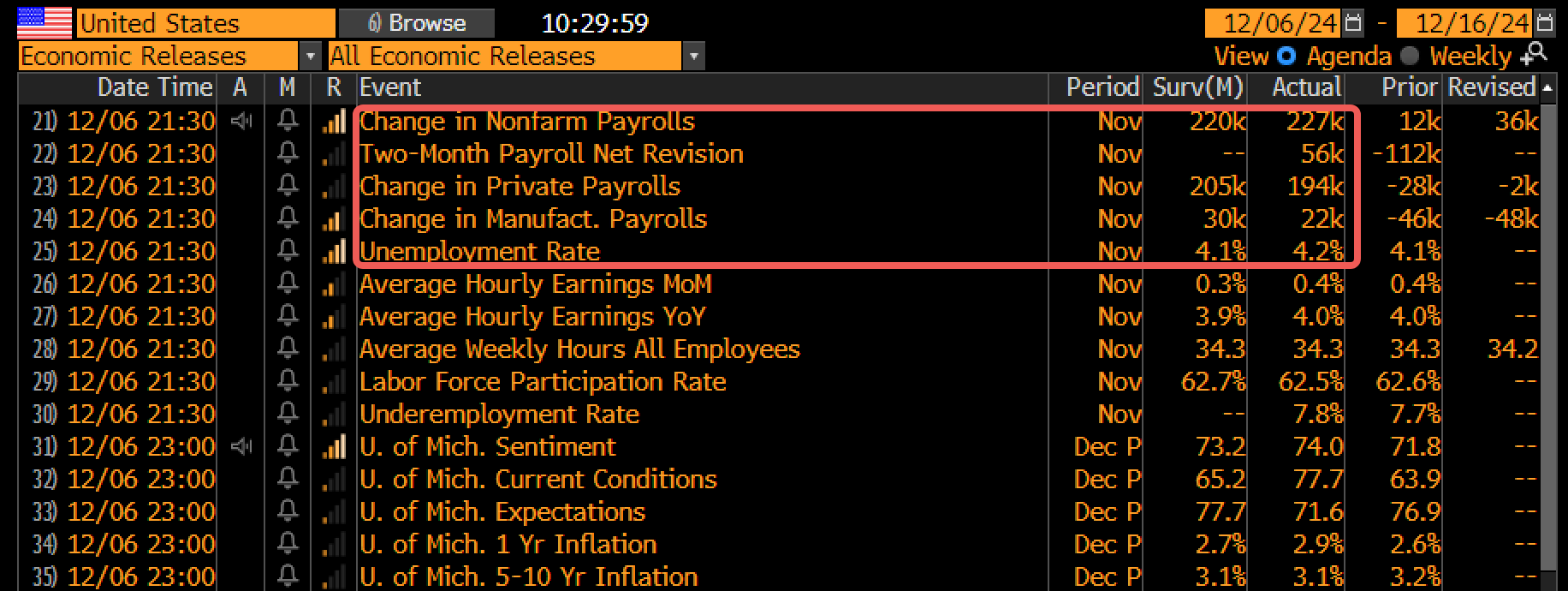

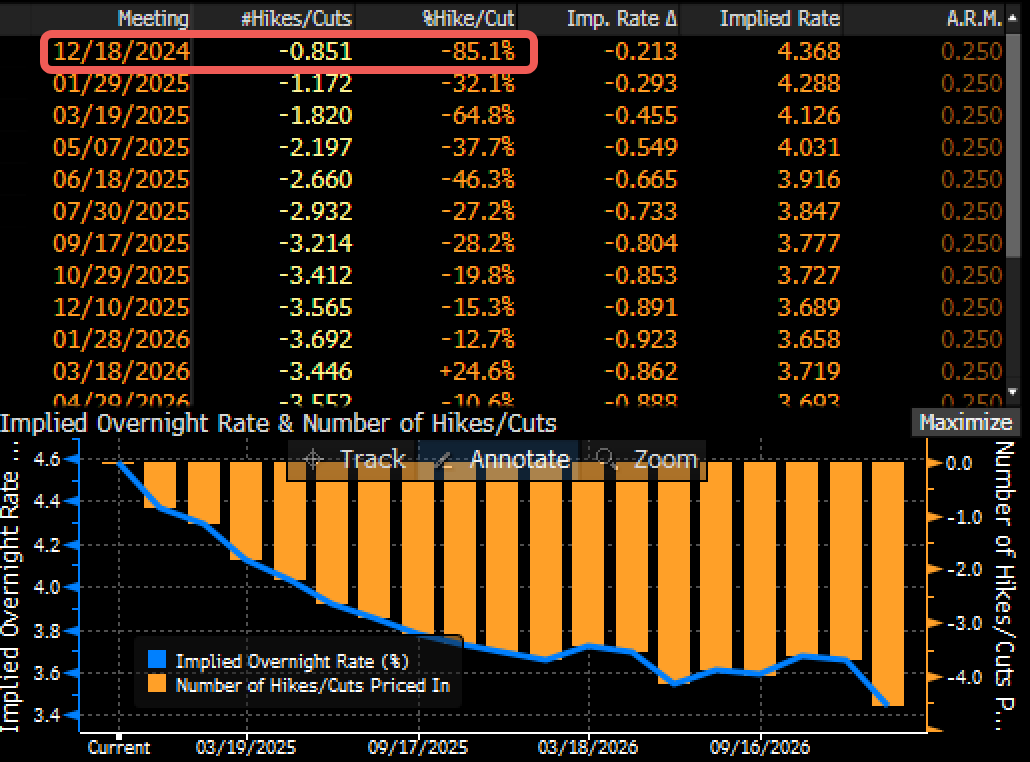

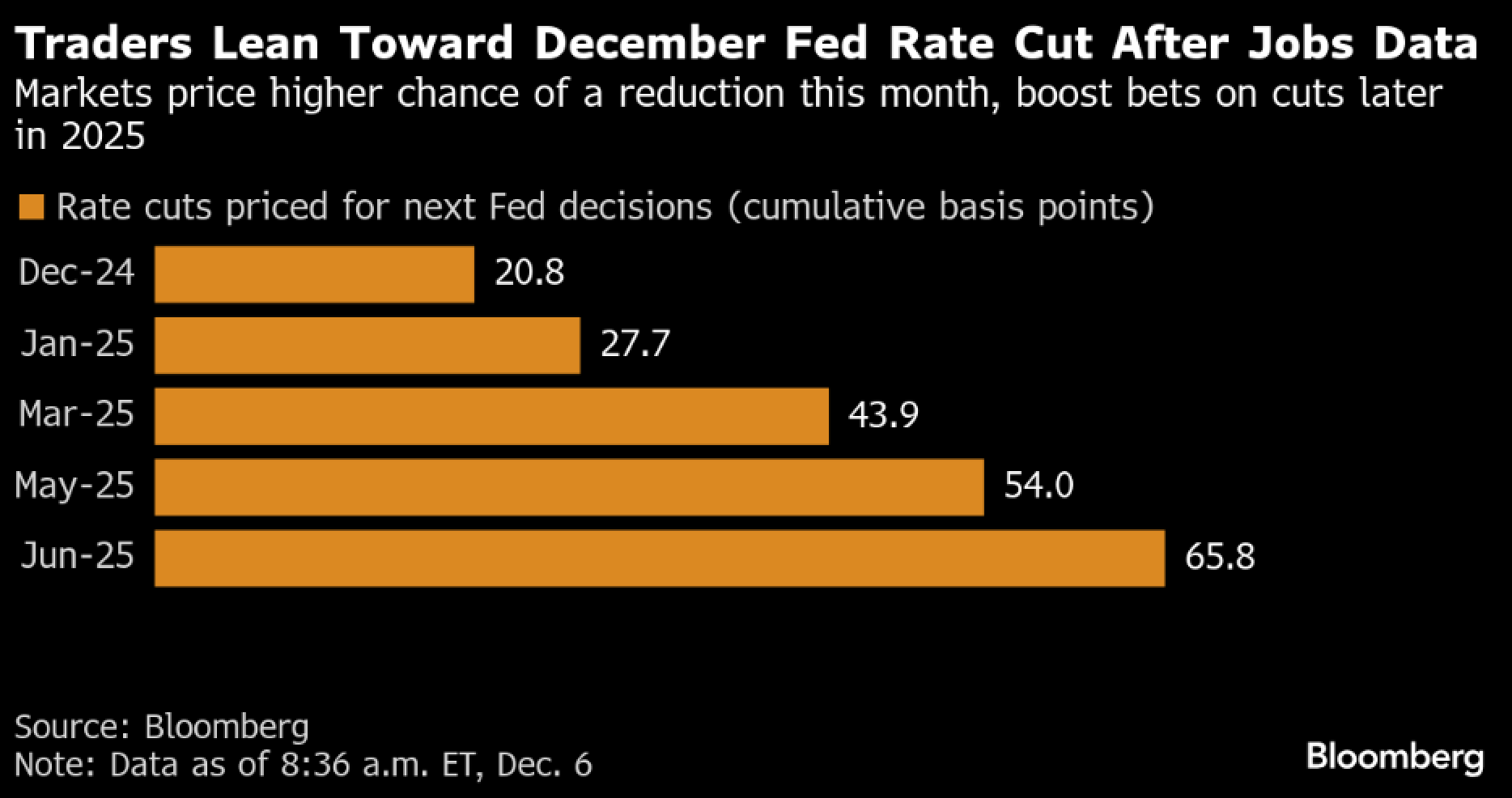

A somewhat lukewarm NFP kept December rate cuts alive, with headlings slightly beating estimates, but last month’s poor figure (12k) saw little upward revisions, pointing to some factual weakness in the job market. However, a slightly high unemployment rate suggests that the labour market is cooling gradually without significant deterioration, offering cover for the Fed to cut rates once again in December against a positive risk backdrop. Traders are now pricing in 85% of a 25bp cut in December, and ~30% chance for another cut in January.

A Lukewarm NFP Suggested that the Labour Markets Remain on a Gradual Slowing Path

Source: Bloomberg

Markets are Pricing in 85% of Another Rate Cut Next Week

Source: Bloomberg

Yields descended lower with 2yr yields nearing 4% and 10y yields back at 4.15%, as bond volatility collapsed back to multi-year lows with markets auto-piloting through in goldilocks mode. Markets will see CPI and PPI ahead of the FOMC as the final meaningful releases before year-end, where markets might see a push to push the yield steeper once again as Trump 2.0 policies begin to take form.

Bond Volality Collapsed as Fears of Over-Supply and Inflation Subsided with Recent Developments

Source: Bloomberg

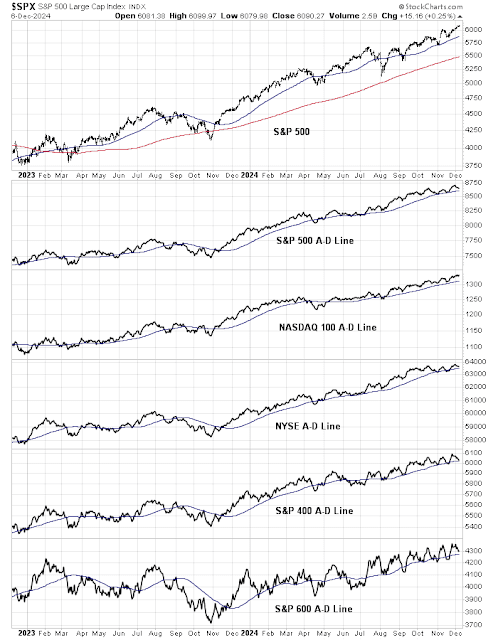

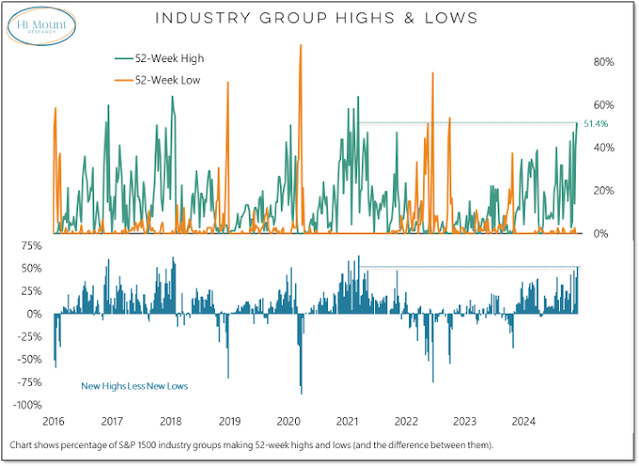

US equities inched higher towards ATHs again thanks to the cooperative data set and dovish fixed income moves. Technicals remain supportive with advance-decline lines still moving to the top right, while new 52-week highs continue to outpace lows with equities gaining across the board.

Technicals on US Equities Continue to Pain a Supportive Picture

Source: Cam Hui

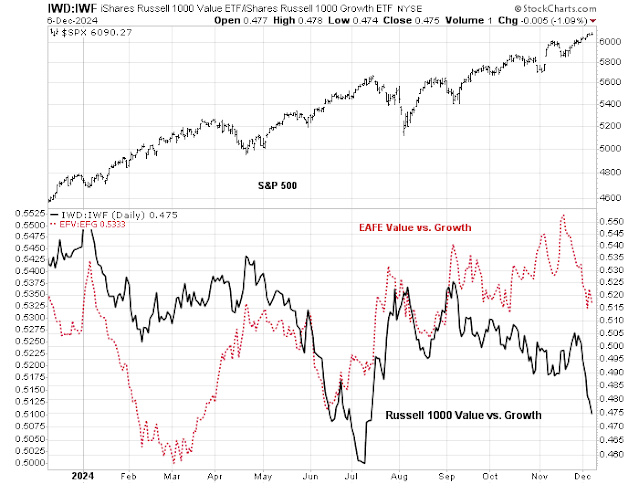

Interestingly, the risk-on action has been so pervasive that growth names have started to outperform value once again, a relatively rare occurrence at this late growth cycle. Is this a contrarian signal of the current excess, or the tentative beginning of yet another leg up in risk come January? One thing is for sure, it’s certainly hazardous to be any form of a bear in this market…

Growth Stocks are Leading Value on the Current Leg Up

Source: Cam Hui

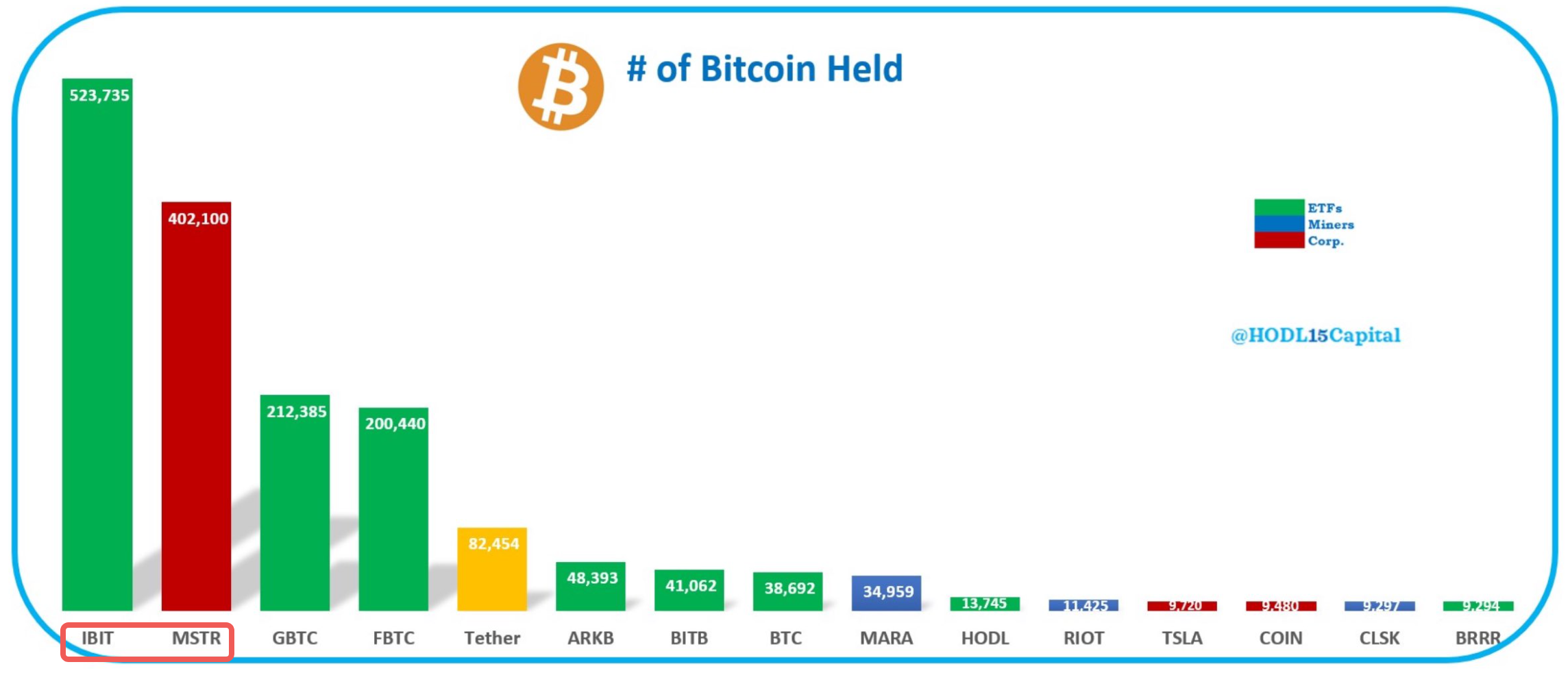

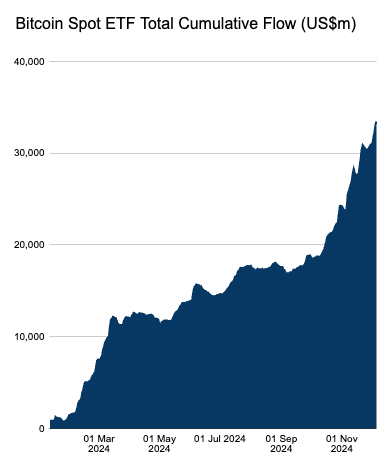

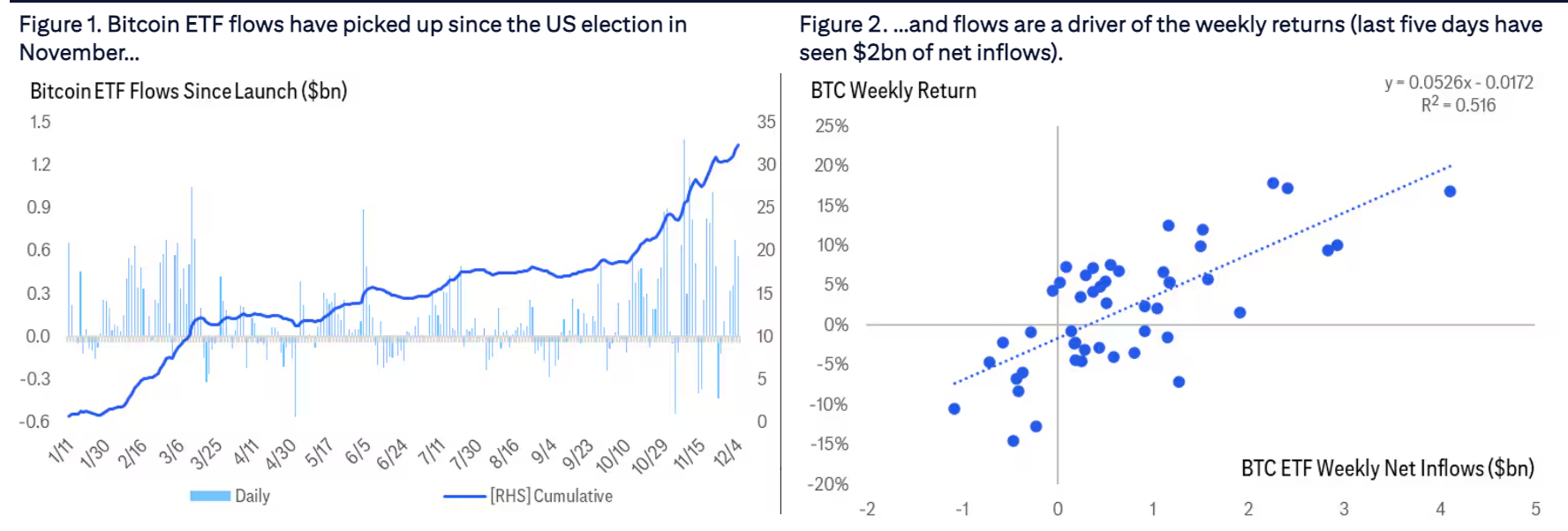

Over in crypto, all lights are flashing green with BTC closing in at $100k once again and ETH looking to crack $4k. ETF flows were massive with $2.7B and $0.8B of BTC and ETH new buying, respectively, and good for a 10th consecutive day of positive inflows. As is the case for most of the year, TradFi inflow remain the dominant factor behind spot performance, with ~$12B of cumulative buying since the election. At the same time, Blackrock and Microstrategy have quietly become the largest BTC holders in the market, holding nearly 1M coins between the both of them and permanently altering the supply/landscape in the process.

Crypto Notches Up Another Strong Week of Gains Across the Board

Source: Messari

BTC and ETH have Seen 10 Consecutive Days of Positive Inflows

Source: Farsight Investors

Follow the Money… TradFi Flows Continue to Drive Spot Performance

Source: Citi

Blackrock and Microstrategy are Now the Largest Holders of BTC in the Market

Source: X

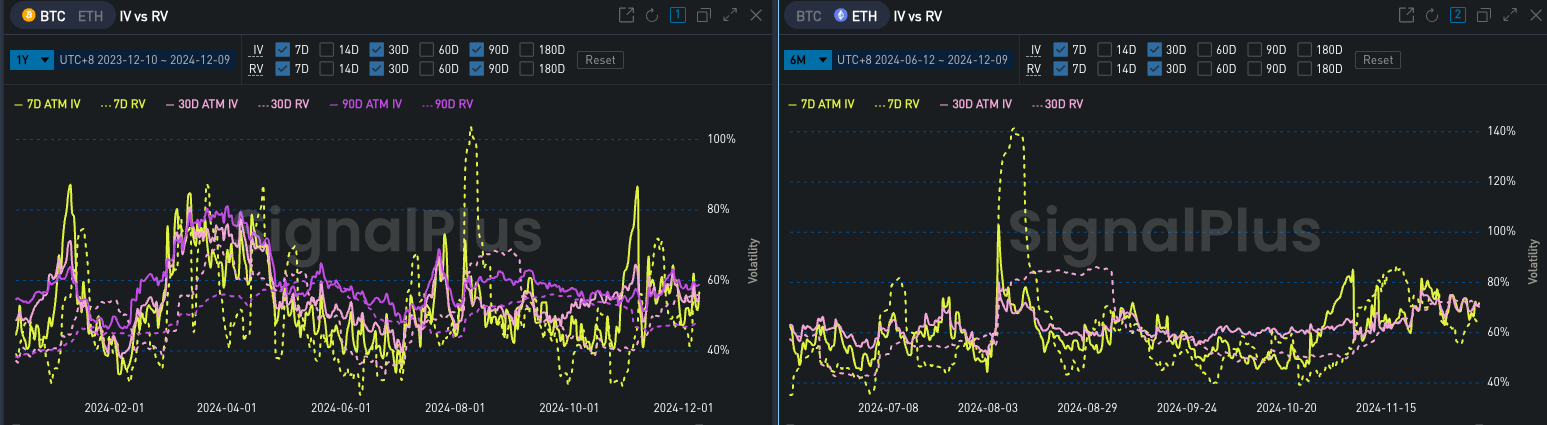

Finally, perpetual funding rates remain relatively high as the bullish sentiment carries on, with annualized rates upward of 20% on major CEXs. BTC call skews are showing a similarly bullish tilt, with smiles greatly skewed to the upside, even as underlying vol remain held steady with vol-selling strategies remaining popular.

Perp Funding Rates Remain High as Levered Buying Interests Remain Rampant

Source: Coinglass

BTC Vol Smiles are Substantially Skewed to the Upside

Source: SignalPlus

Though Overall Volatility Remains Contained with Vol Selling Strategies Remaining Popular

Source: SignalPlus