15% – that would seem to be the new ‘official’floor tariff rates for all US trade deals going forward given the most recent announcements with Japan and EU over the weekend. Europe just matched Japan in getting a 15% general tariff, though with some unresolved vagaries over energy purchase and VAT arrangements. Nevertheless, at the end of the day, the deal should translate to ~another $90-100bln of incremental tariff revenue to the US, plus another $600bln of inbound investment due from the European continent. A pretty solid outcome for the administration when it’s all said and done.

At the same time, the US announced another 90-day reprieve on the China levies, though questions remain on how much breakthrough one can expect given the relatively tougher terms assigned to Asia (ex-Japan) trade partners thus far. The story continues.

Current Confirmed Tariff Rates on US Trade Partners

Meanwhile, the equity market continued to rocket to a series of new highs with earnings coming in just ‘good enough’ versus expectations (Alphabet led the way), as well as thawing tensions between President Trump and Fed Chair Powell. Following a photo-op filled visit to the Fed HQ, Trump appeared to amend the relationship by stating:

- TRUMP SAYS FIRING POWELL UNNECESSARY, FED WILL DO RIGHT THING

- TRUMP: POWELL TOLD ME ECONOMY IS DOING WELL

- TRUMP SAYS POWELL IS A ‘VERY GOOD MAN’

President Trump has Recently Dialed Down the Rhetoric on Fed Chair Powell as Tensions Appear to be Thawing

Source: Le Monde

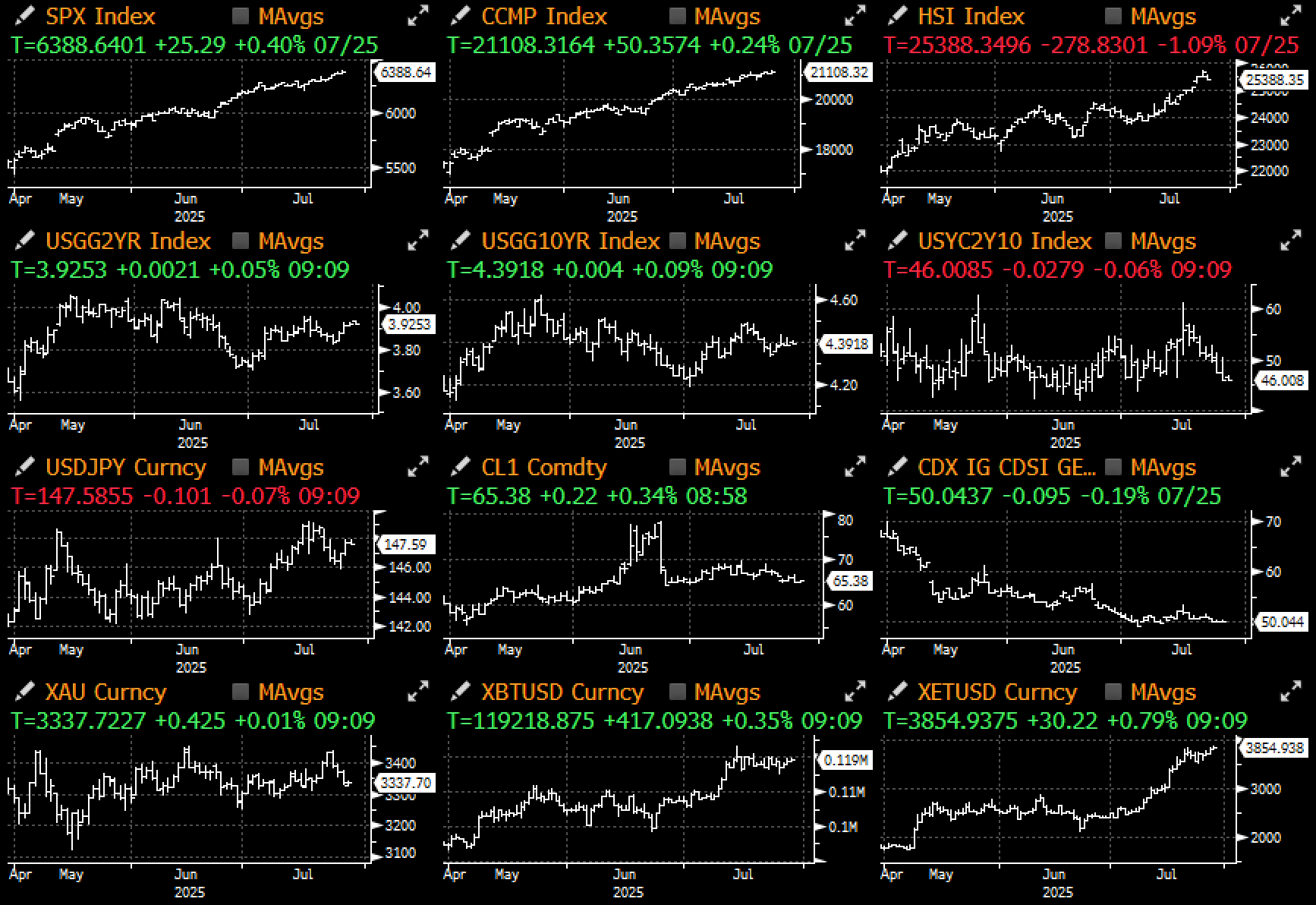

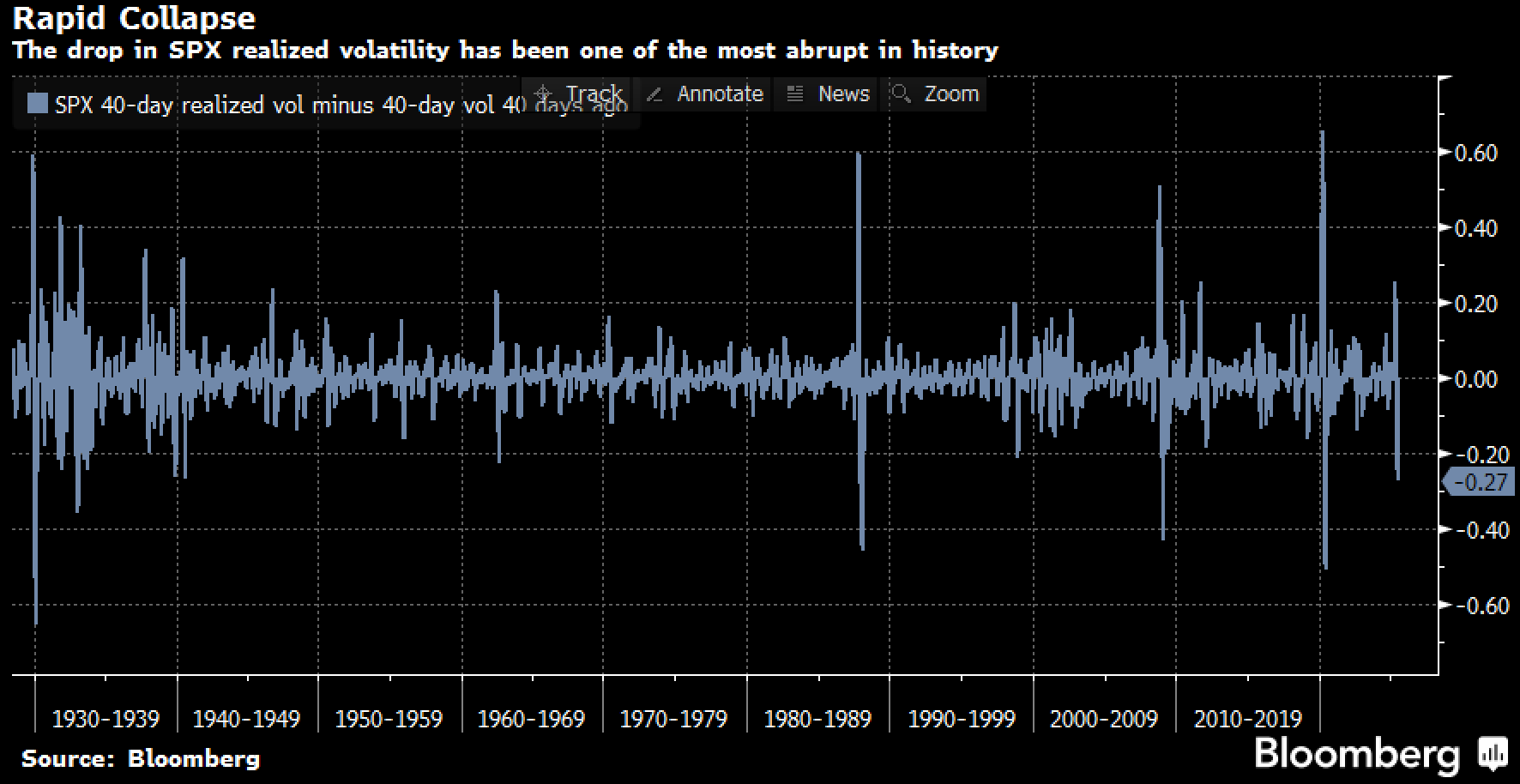

With the easing of one of the largest remaining political overhangs, the US dollar bounced and the yield curve flattened on the week as a reprieve move. Global indices in the EU and Japan also rallied as they reached an ‘acceptable’ trade deal with the US, while equity volatility continued to crater in one of the most sustained moves in history.

Equity Volatility Continued to Crater Against New Record Highs With No Fear in Sight

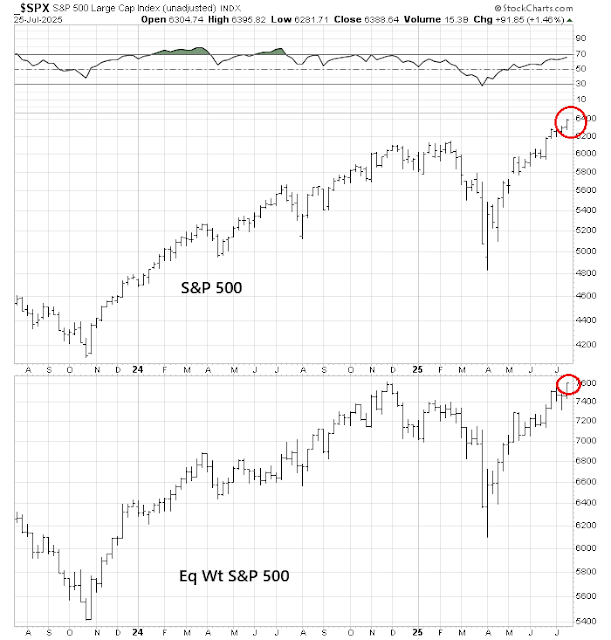

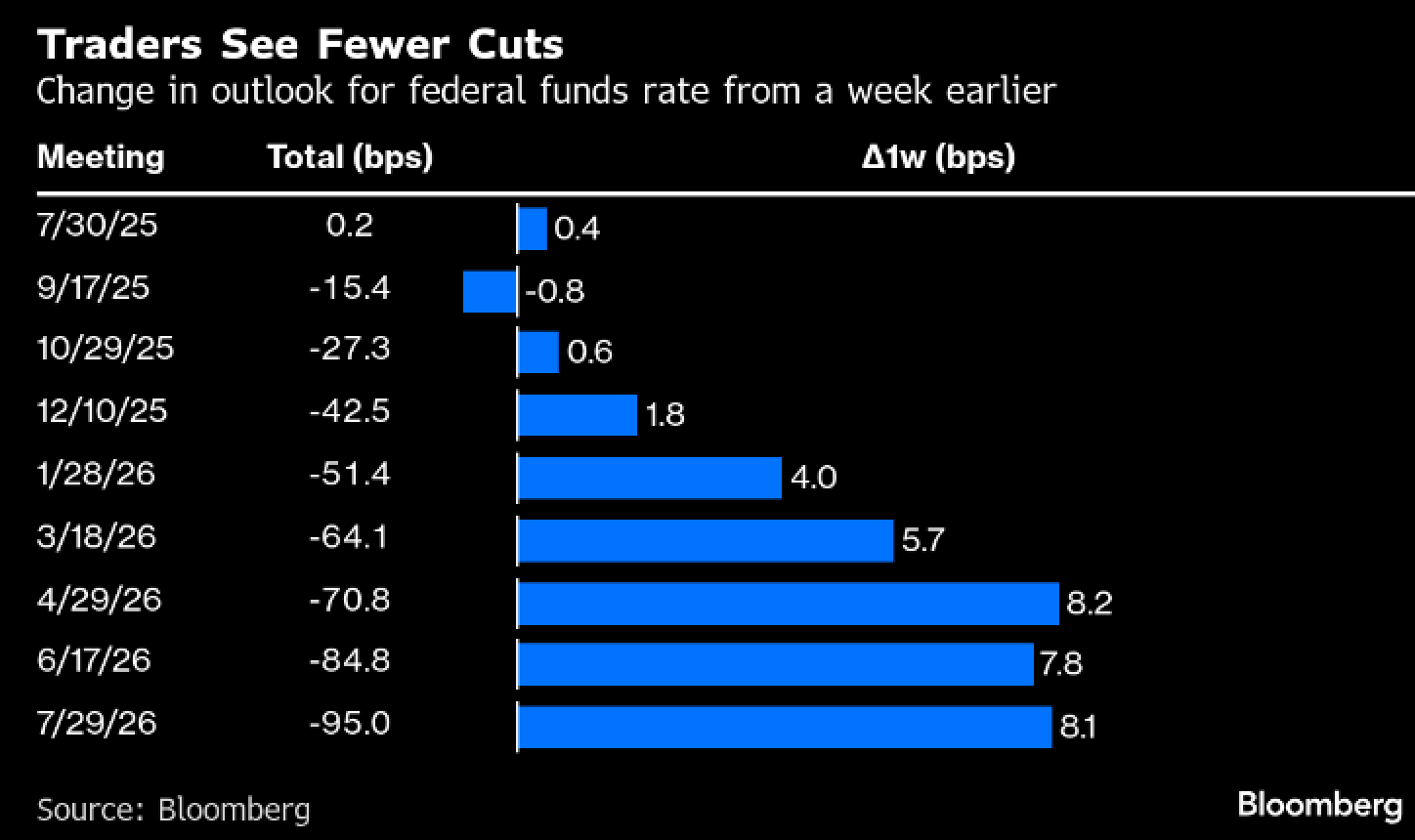

Unfortunately for bears, momentum indicators are breaking out to the upside, with markets seeing impressive breadth with both the benchmark and equal-weighted SPX making new highs last week. Moving averages (13w & 26w) have crossed over to the upside, while bond traders have ratcheted down rate cut expectations as risk sentiment is firing on all cylinders.

Most Momentum Indicators are Flashing Positive for US Equities Everywhere We Look

Source: Cam Hui, Bloomberg

Rate Traders have Dialed Back Rate Cut Expectations Given the Overriding Risk On Sentiment

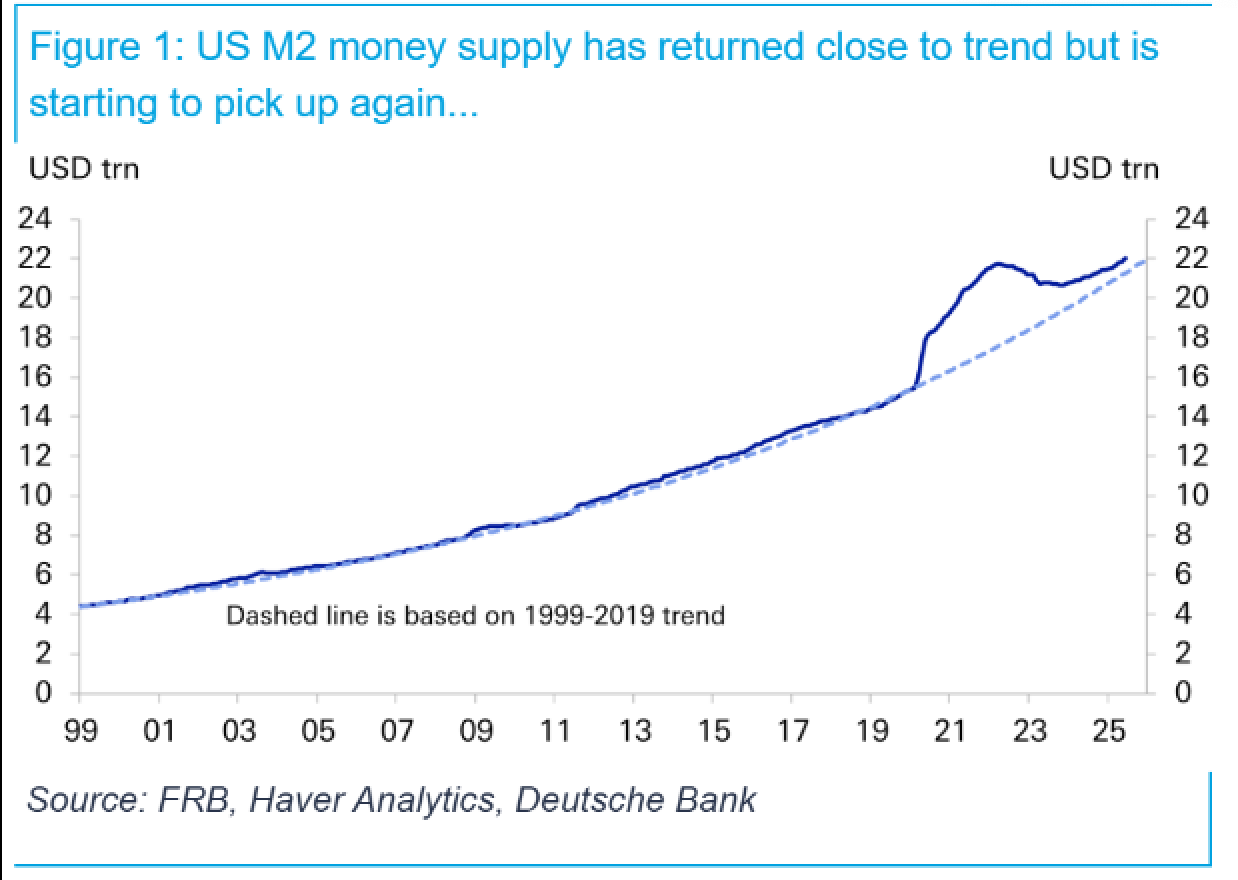

Macro and financial conditions continue to remain favourable as well, with M2 supply growth starting to pick up again with the recent dovish turns across global CBs, in addition to the weaker dollar. This is positive for financial and fixed assets, including commodities and crypto.

M2 Money Growth has Quietly Started to Accelerate to the Upside Again

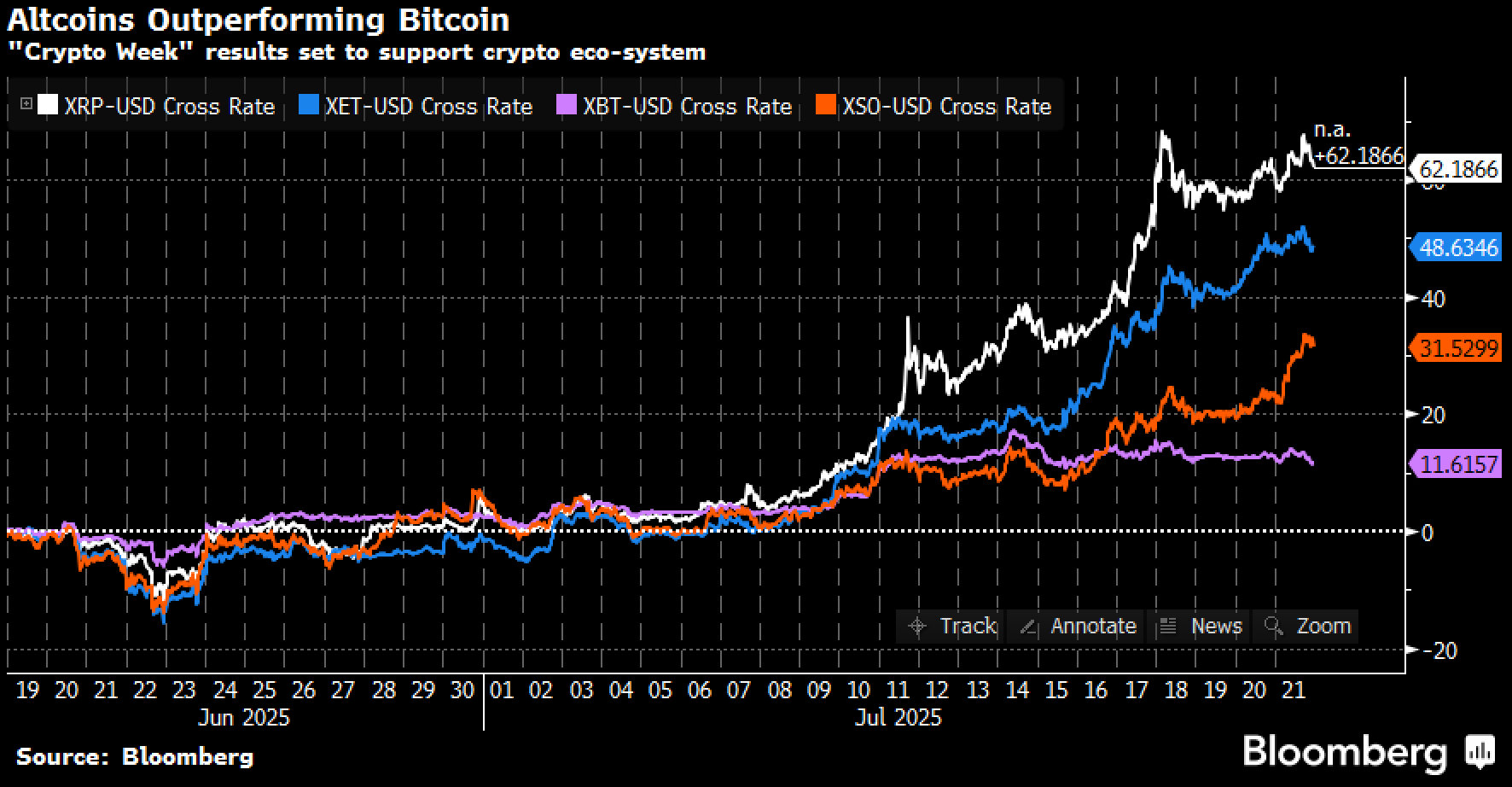

Speaking of crypto, despite a well advertised $9B profit-taking sale from a ‘Satoshi-era’ investor as reported by Galaxy Digital, prices barely budged with BTC hovering around $120k and ETH back to $4K. Whatever OG outflows we saw were matched against ATH weekly inflows in spot ETFs, with digital assets seeing the 14th consecutive week of inflows and bringing YTD totals to $27bln, and weekly inflows of nearly $4.4bln.

The Crypto Rally has Finally Spilled Over to Altcoin Overperformance After a Long Doldrum

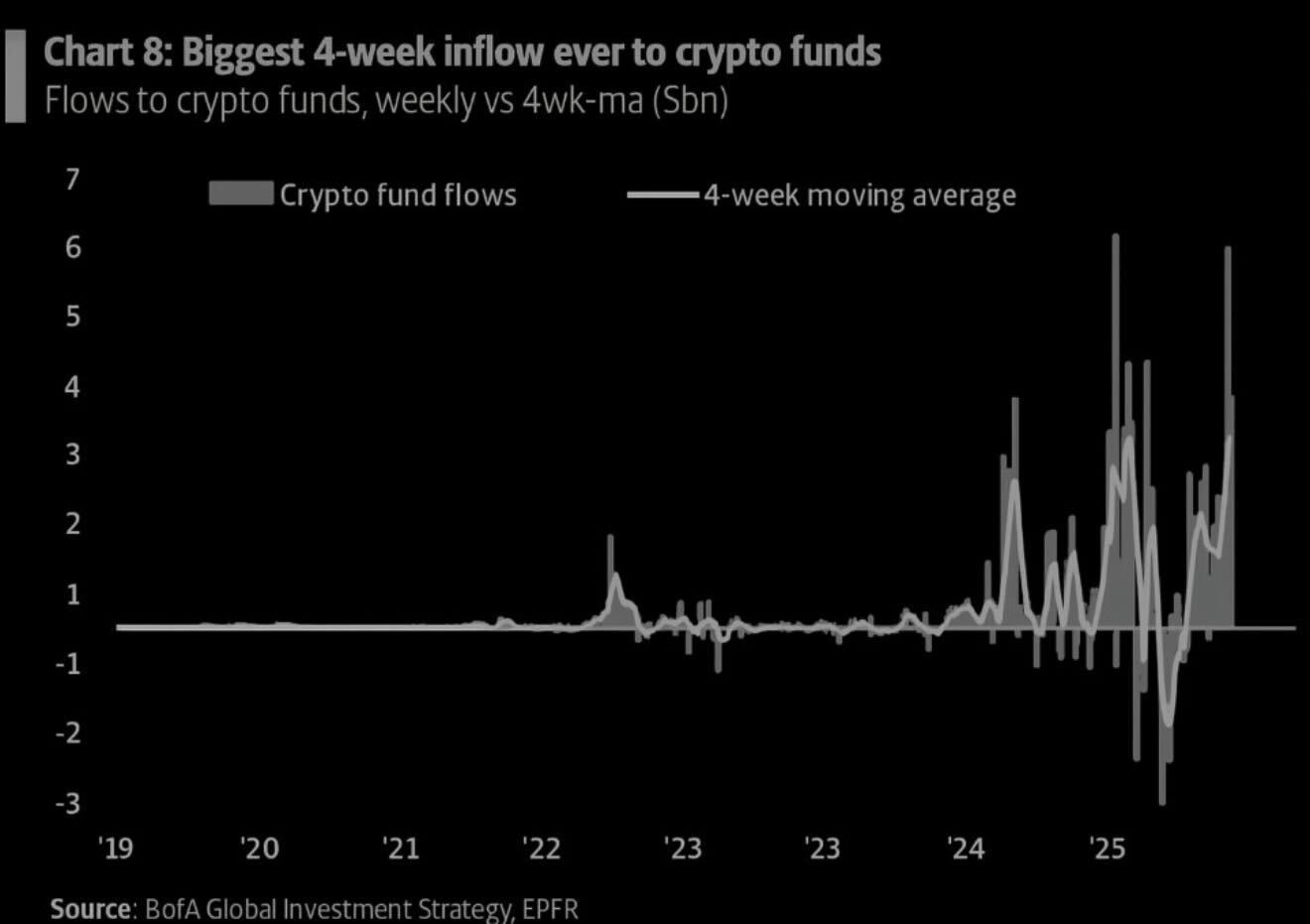

Weekly trading ETF turnover also reach record levels at nearly $40bln, with ETH stealing the show the show as of late with a $2.1bln haul, nearly doubling its previous record and bringing YTD inflows to $6.2bln. ETH ETFs have gained nearly 25% in total AUM over the past 3.5 months alone.

Crypto ETFs Continue to See Record Inflows

ETF inflows continued to be dominated by the US, accounting for well over 97% of the weekly inflows. The mainstream adoption narrative remains red-hot, with GS & BNY Mellon teaming up to use the former’s ‘GS DAP’ platform to handle certain tokenized BNY funds on-chain. While that is certainly a positive development for the space, the key statement to us is:

BNY will continue to “maintain the official books, records and settlements for the funds within currently approved guidelines,” the company said in the statement. — Bloomberg

Ie. The ultimate arbiter would remain within current ‘paper’ methods, not exactly the DeFi/on-chain future natives might have envisioned. But that’s the price one has to pay for mainstream adoption.

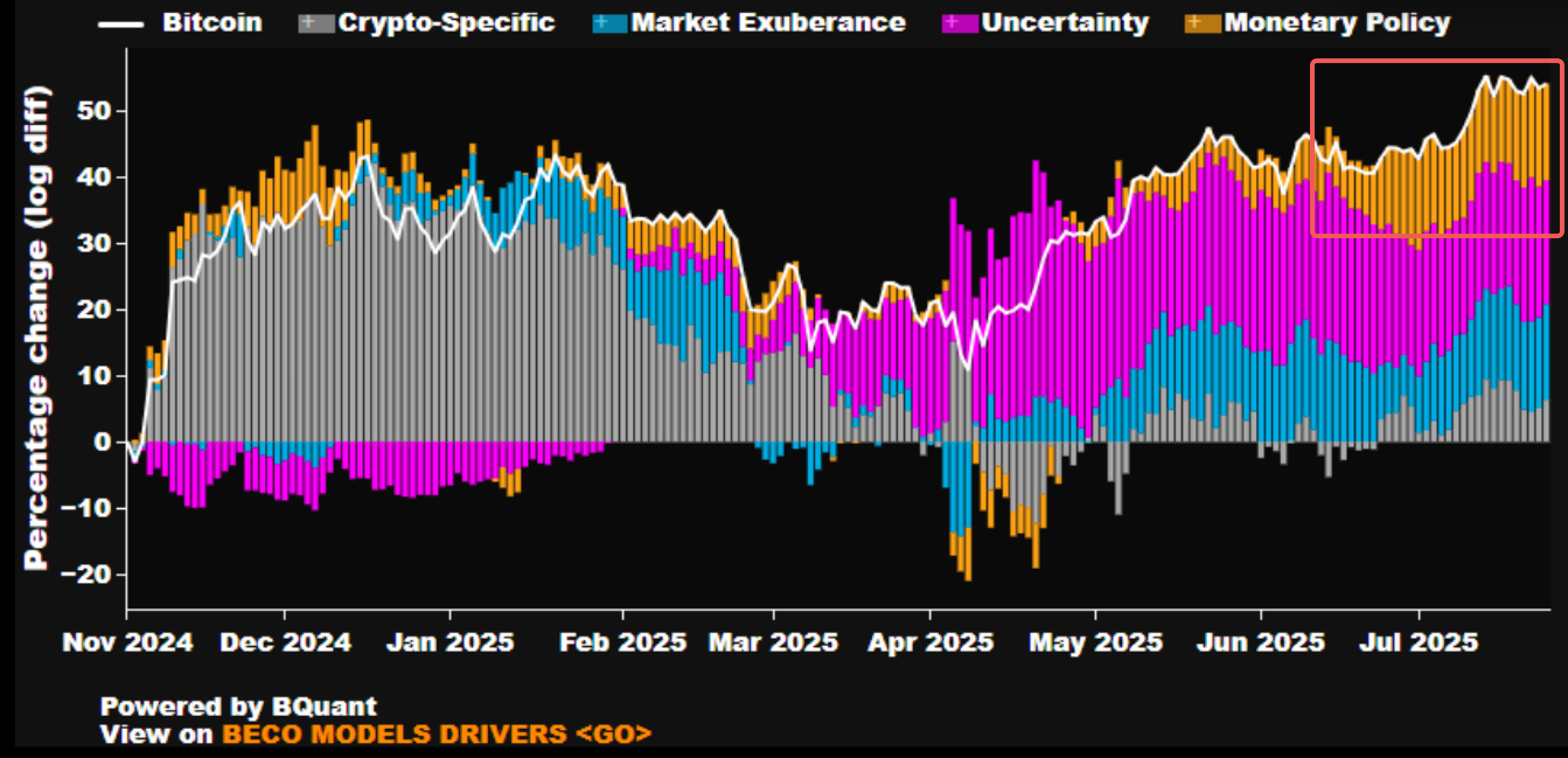

Looking forward, while things certainly look frothy (what asset class isn’t?), with Bloomberg reporting that an increasing portion of the current BTC rally is driven off ‘monetary policy’ contributions – ie. a dovish liquidity outlook. We don’t attest to having a strong opinion on this breakdown, though we would note that gold prices look vulnerable after failing multiple breaks to the upside, which might serve to be a drag for BTC prices in the near-term should we see the yellow metal retrace back to the 3000-3200 area.

Bloomberg’s Model is Attributing an Increasing Part of the Rally to Favourable Monetary Policies

A Short-Term Break to the Downside for Gold Might be a Potential Risk to Look Out for in the Near Term

With that being said, the trend remains your friend (DYOR) and we would continue to caution against fighting the uptrend. Stay strong and enjoy the summer until further notice. Good luck & good trading everyone!