US continued their tariff brinkmanship with the world, with Trump most recently declaring that ‘over 200’ trade talks were taking place and that he’s spoken on the phone with President Xi most recently. However, that statement was quickly refuted by the Chinese Embassy in Washington, who officially declared that “China and the U.S. are NOT having any consultation or negotiation on #tariffs”, and that “The U.S. should stop creating confusion”.

Political analysts believe that low-level talks are probably on-going and taking place, but it’s doubtful that any serious deals are being made, with the effective trade embargo dragging economic growth lower in first half. We don’t expect to see a clean resolution of any China-US trade talks in the foreseeable future.

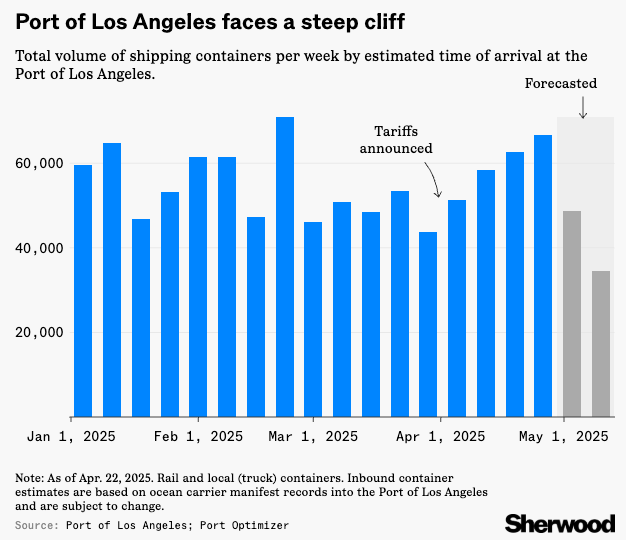

Shipping Volumes Have Started to Drop Off Following the Tariff Embargo

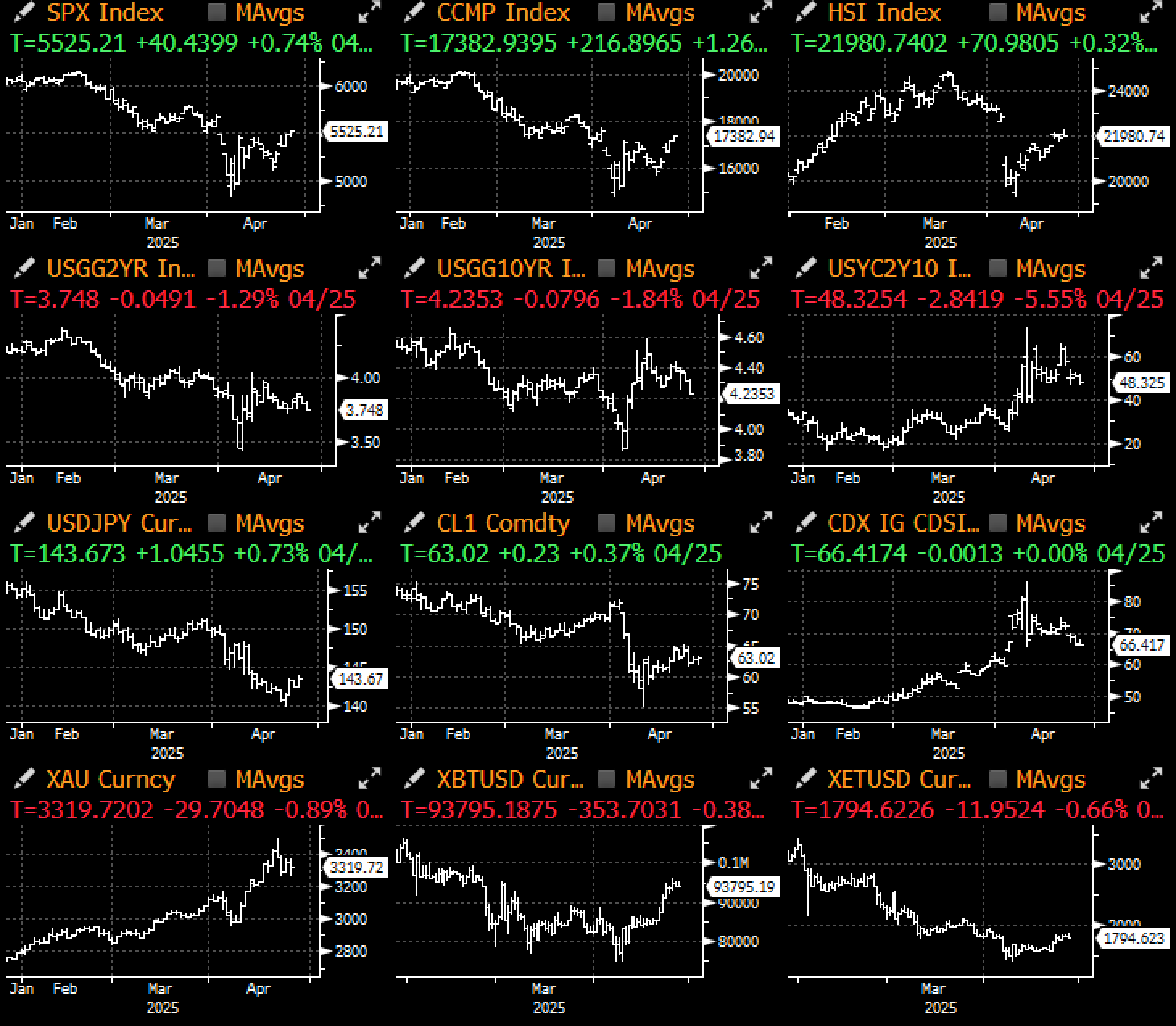

The news (or lack of bad news) was good enough for equity markets to stabilize, which saw US stocks post their 2nd biggest weekly gains YTD, and for most non-USD macro assets to recover much of their drawdowns since liberation day.

US Equities Enjoyed Their 2nd Best Weekly Gain Last Week

Most Non-USD Based Macro Assets Have Recovered Much of Their Post Liberation Day Drawdowns

Source: Citi

The Administration Comeback Tour….

Source: X

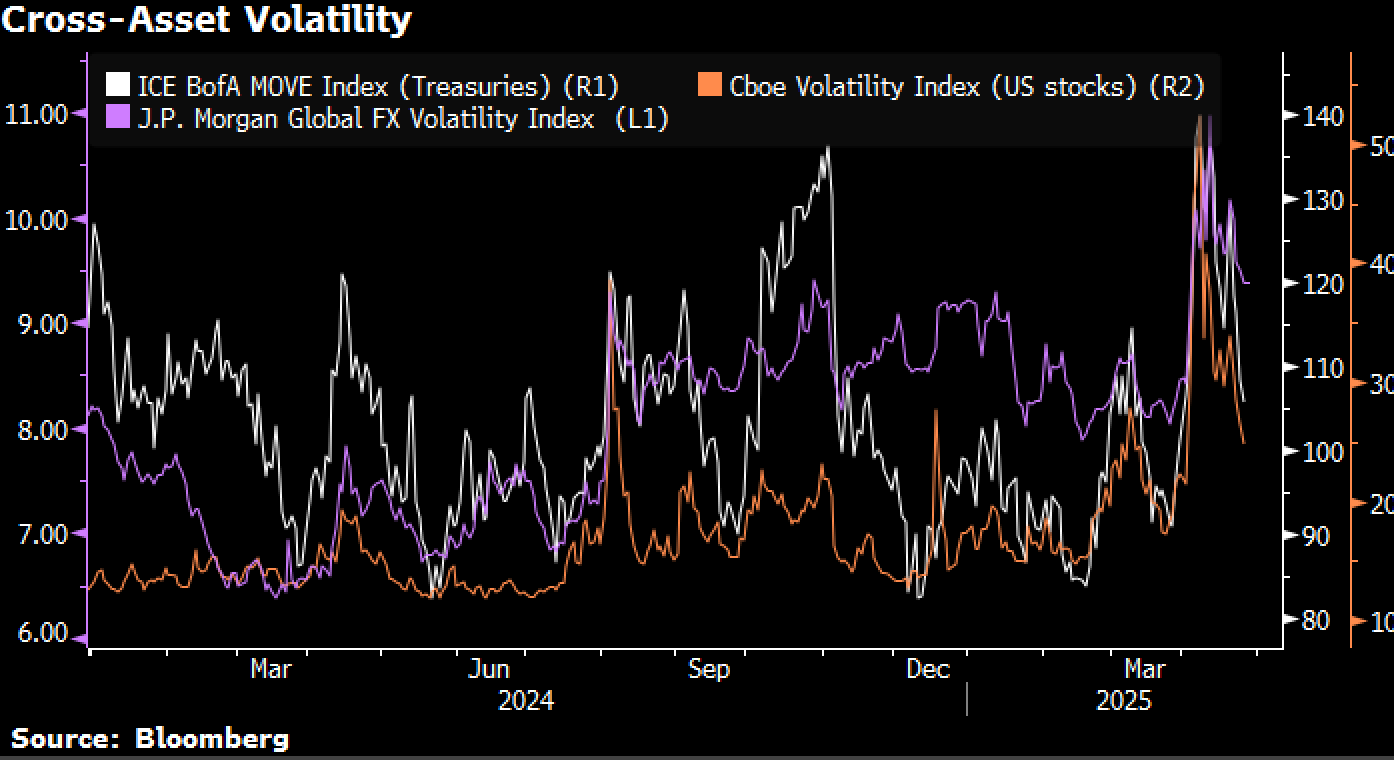

Volatility and credit spreads have made a similar recovery, with expensive tail hedges rolling off and the worst scenarios have not (yet) been realized. We expect that risk markets could continue to squeeze higher a bit more to ‘illogical’ levels before we resume on a more pronounced bear market later on in the 2H of the year.

The breaks in trade relationships and growth damage are very real, with the respective countries cutting off their supply chain dependency on one another. Global portfolios will be reconsidering their USD dependency as well if the current account-funded deficit begins to reverse in the years ahead.

Volatility Has Fallen Significantly Along with Tighter Credit Spreads

Source: Bloomberg

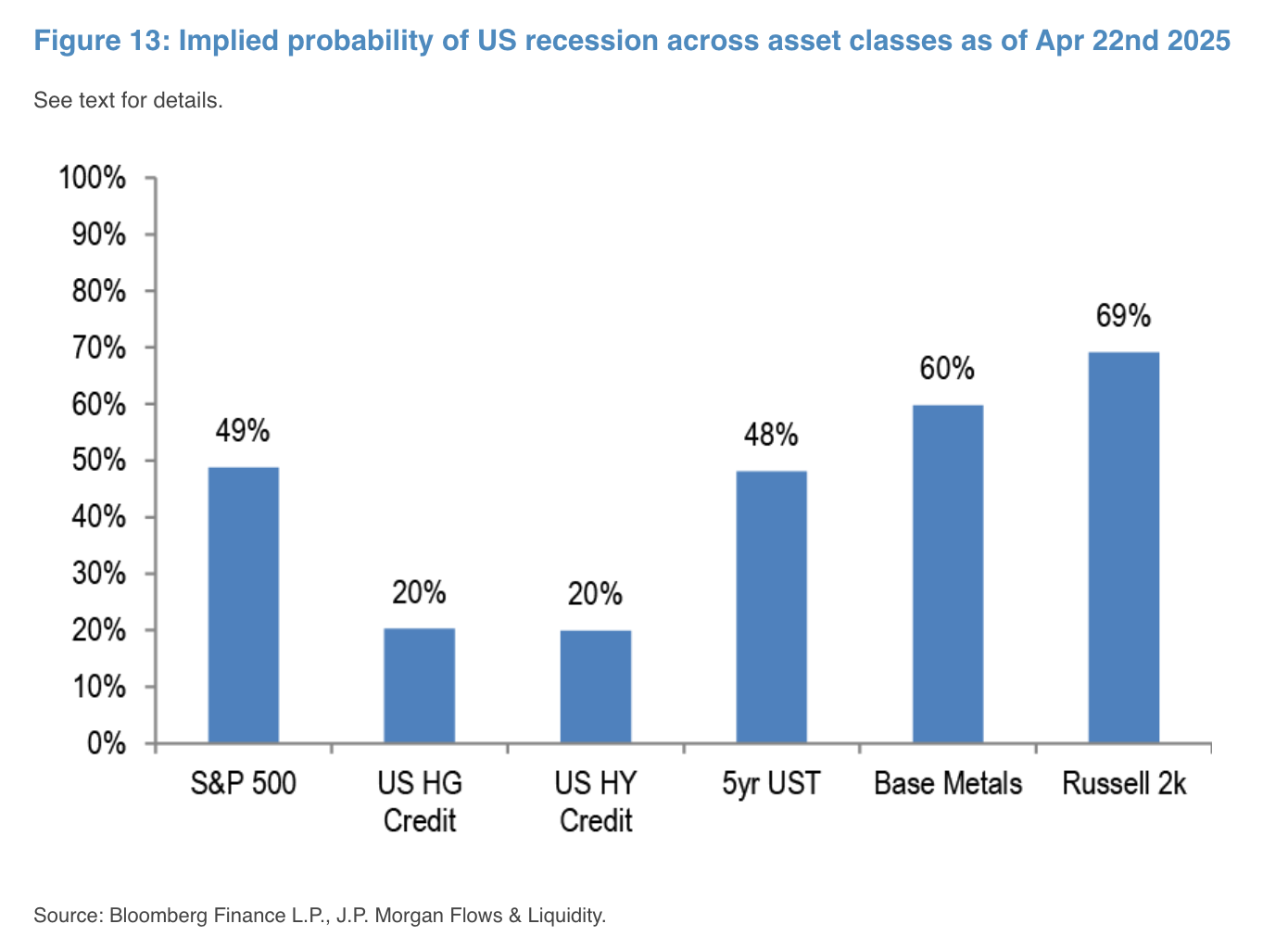

Interestingly, the recovery in credit spreads is now pricing just ~20% chance of a US recession, based on historical modelling. On the other hand, the poor performance of small caps is suggesting ~70% of an imminent slowdown, with treasuries and SPX looking at basically a coin-flip. Different strokes for different folks.

Is a Recession Coming? Depends on Who You Ask…

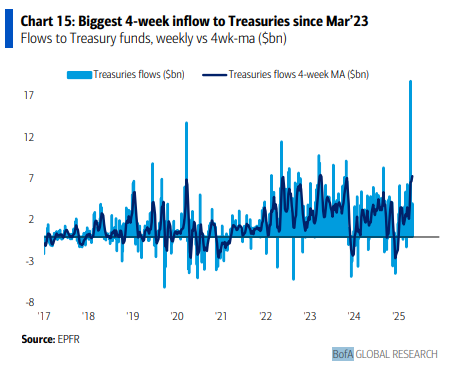

For now, normalcy is returning as even US treasuries saw its biggest 4-week in nearly 2 years, with investors purchasing bonds en masse ahead of an imminent economic slowdown and continued softening in spot inflation.

As our long-term readers are aware, expectations of any near-term demise of treasury bonds are always greatly exaggerated, with private holdings of treasuries increasing in 2024 to make up for any drop in official (central bank sales), and non-US holdings still at elevated levels.

False Alarm? US Treasuries Enjoyed Their Largest 4 Week Inflows (Purchases) in Over 2 Years

Source: BoA

Private and Non-US Holdings of US Treasuries Remained Very Health Into Year-End

Source: Money Inside Out

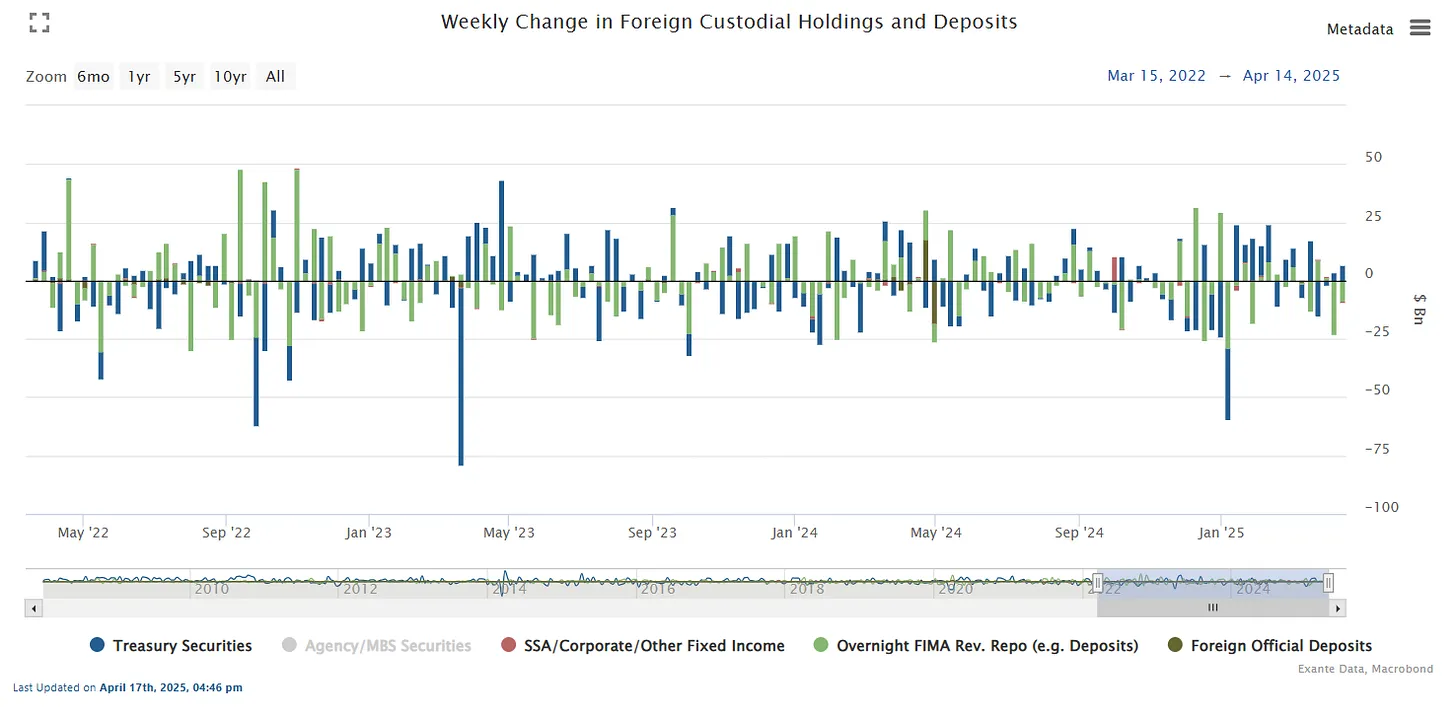

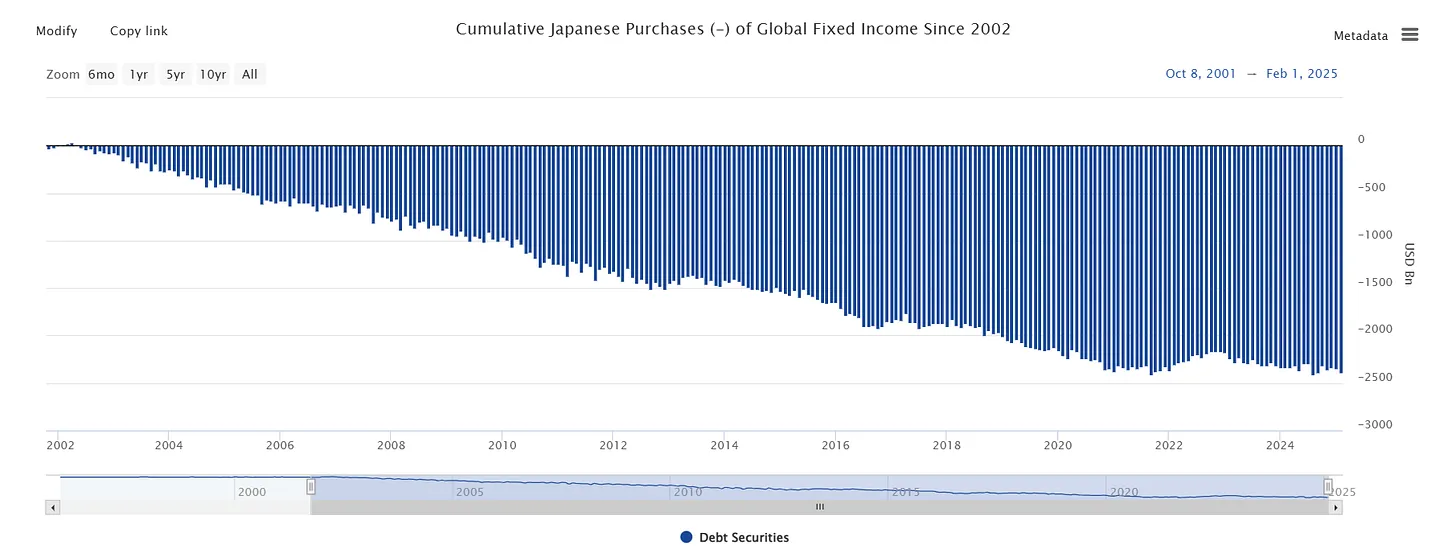

The most recently available data on weekly official activity suggests that there hasn’t been any significant selling of treasuries, with cumulative Japanese purchases also looking stable despite concerns otherwise.

Most Recently Available Data on Foreign Central Bank Activities Suggest No Significant Change in Net Treasury Purchases and Sales

Source: Money Inside Out

Japanese Cumulative Purchases Remain Stable as Well

Source: Money Inside Out

On the other hand, the recovery in risk appetite sparked the largest daily gold outflow in over 14 years, with dealers reporting over $1.3B of net selling last Tuesday.

Gold Saw $1.3B of Outflows Last Tuesday, Largest in 14 Years

Source: GS, Zerohedge

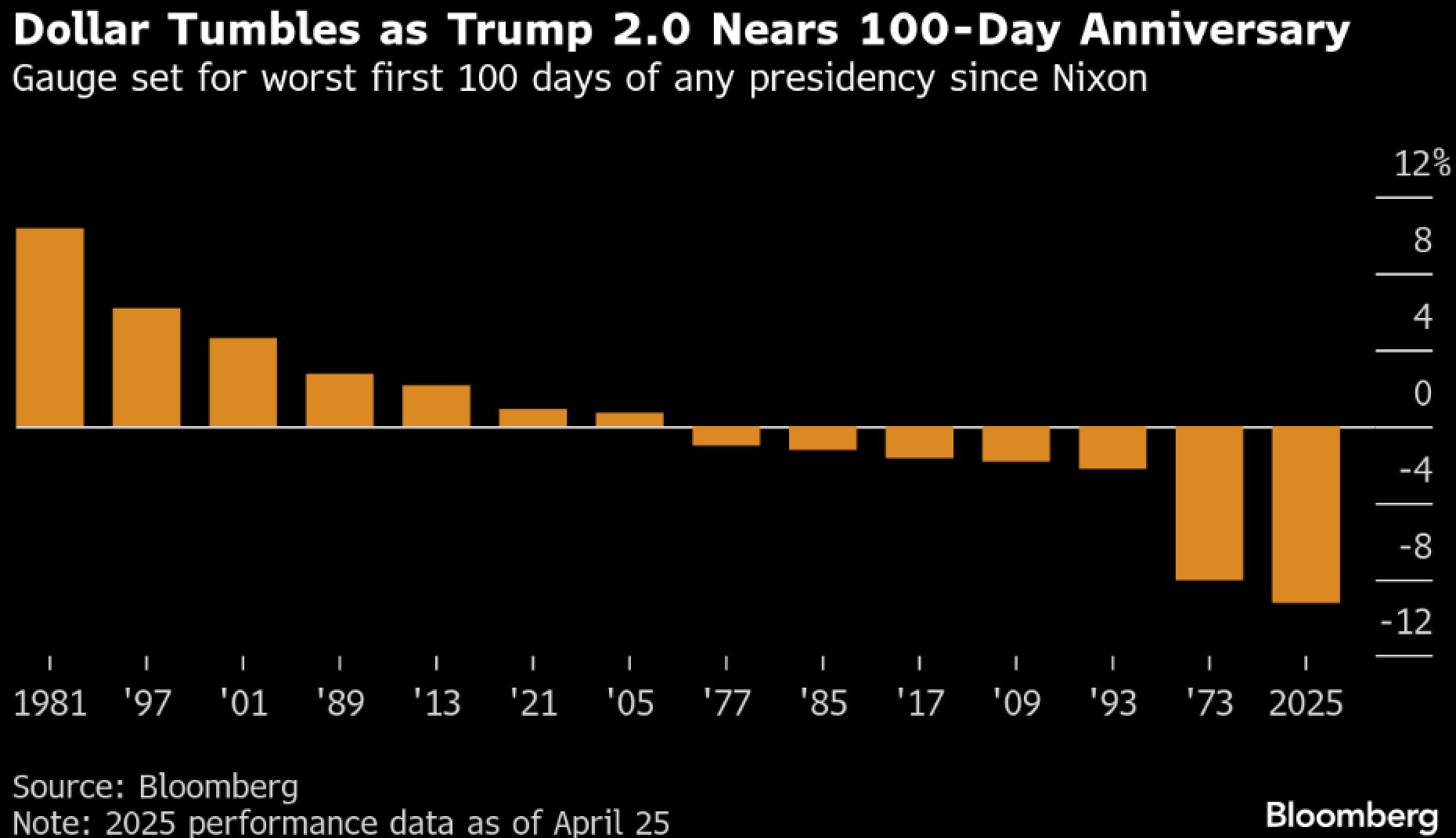

Similarly, the USD index is off to the worst start during the first 100 days of a US presidency, with the dollar falling over 10% vs majors, performing worse than the end of the Bretton Woods era in 1973.

USD is Off to the Worst Start of Any US Presidency in Modern History

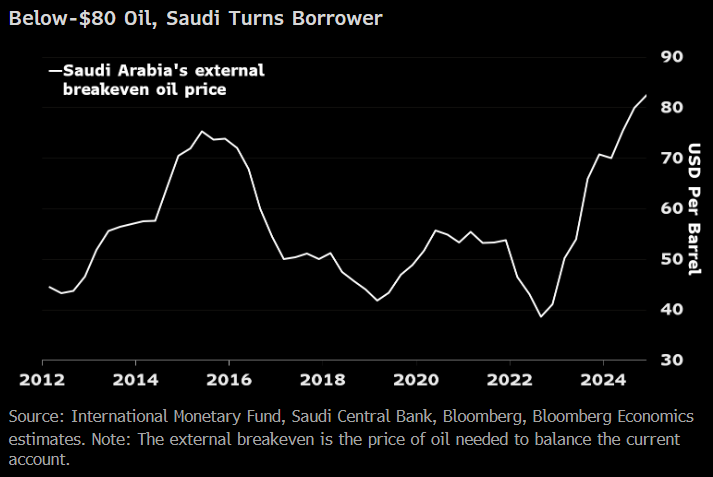

To add insult to injury, Saudi Arabia’s fiscal situation is looking to turn from lender to borrower even with oil price at $80, removing one of the biggest excess capital sources in the world, and raising questions on how much the available pool of capital will be to fund the burgeoning US debt balance in the long-run.

Even Saudi Arabia is Looking to Turn Into a Net Borrower as Their Fiscal Dynamics Change

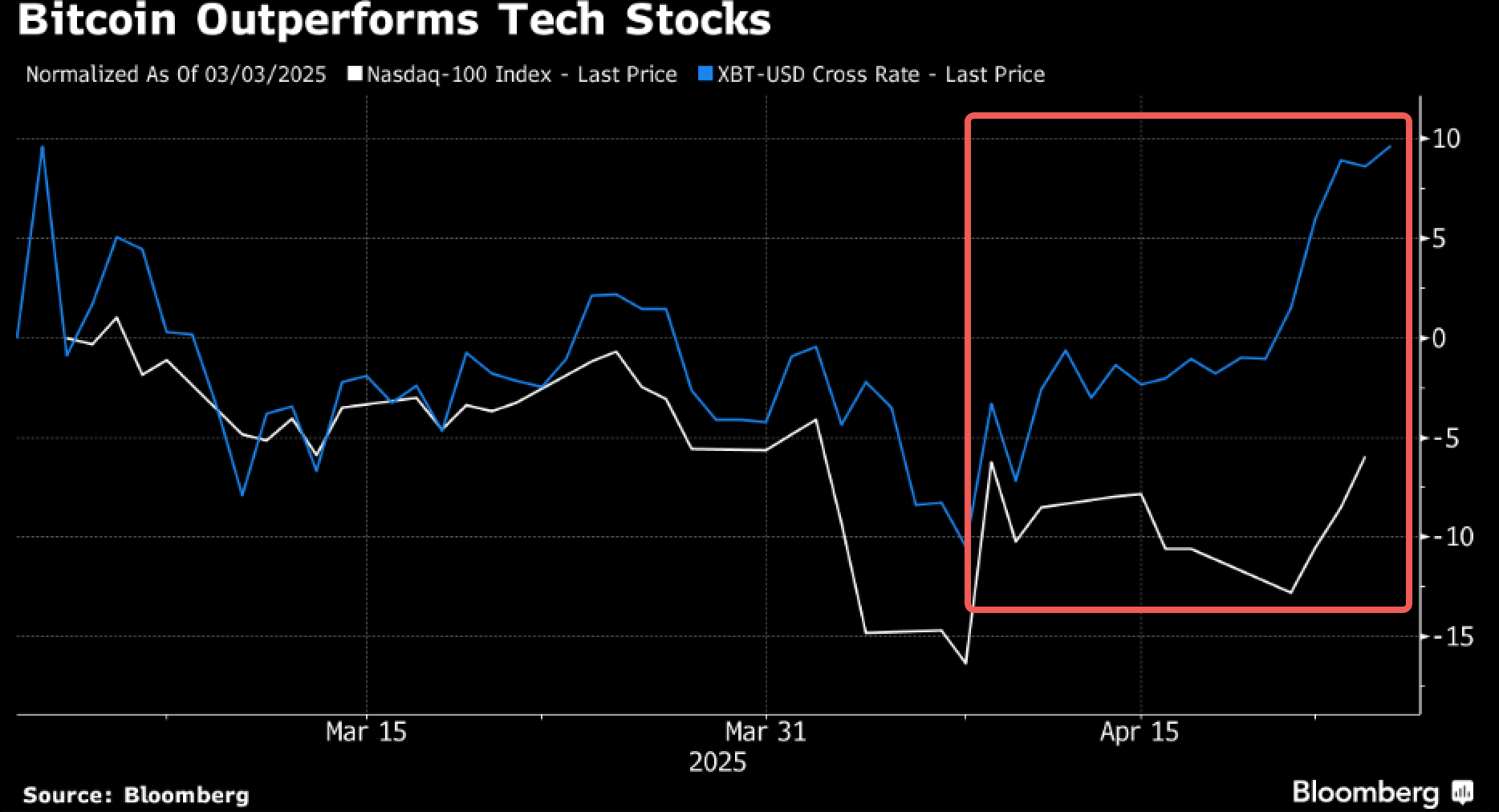

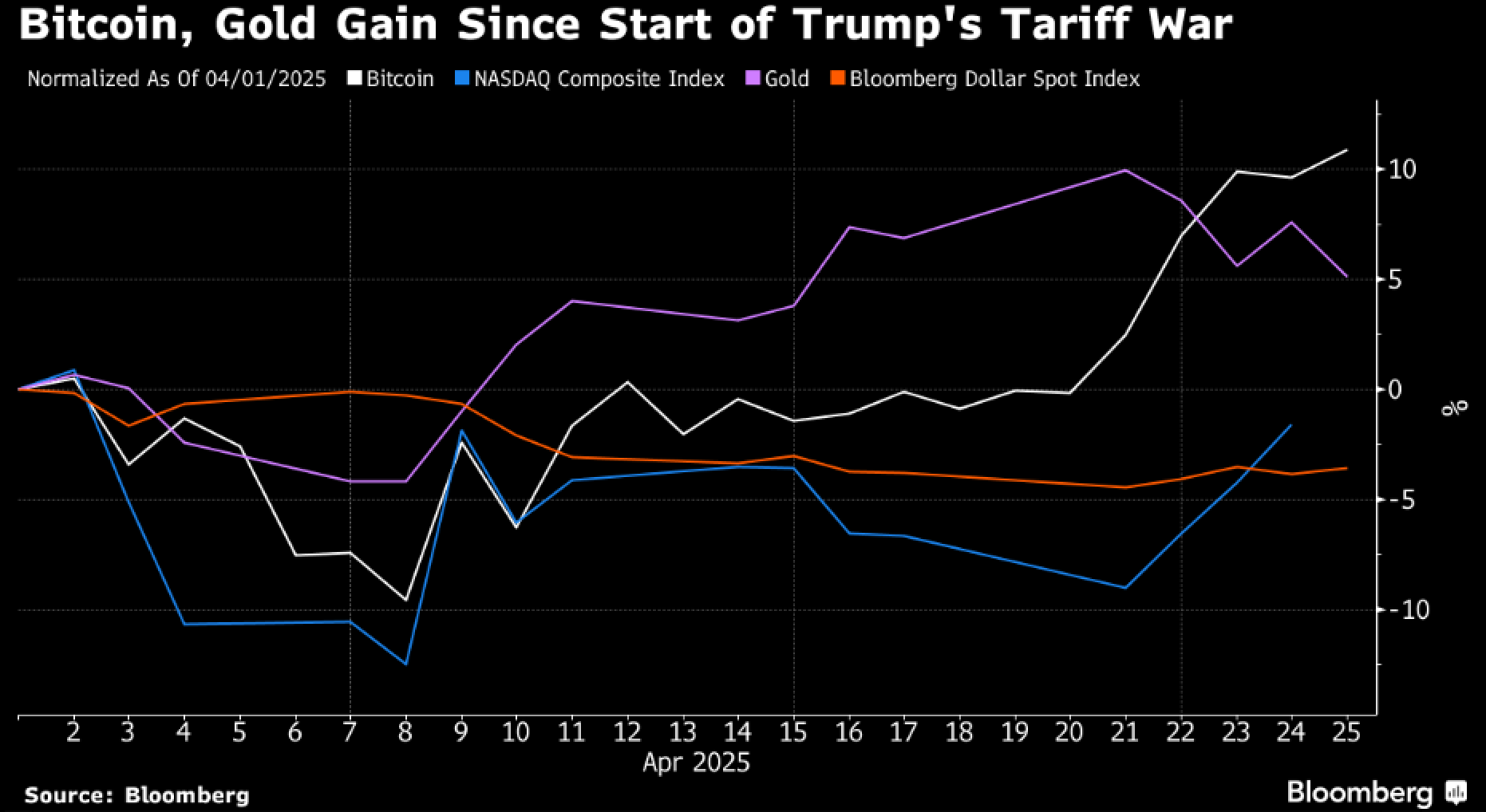

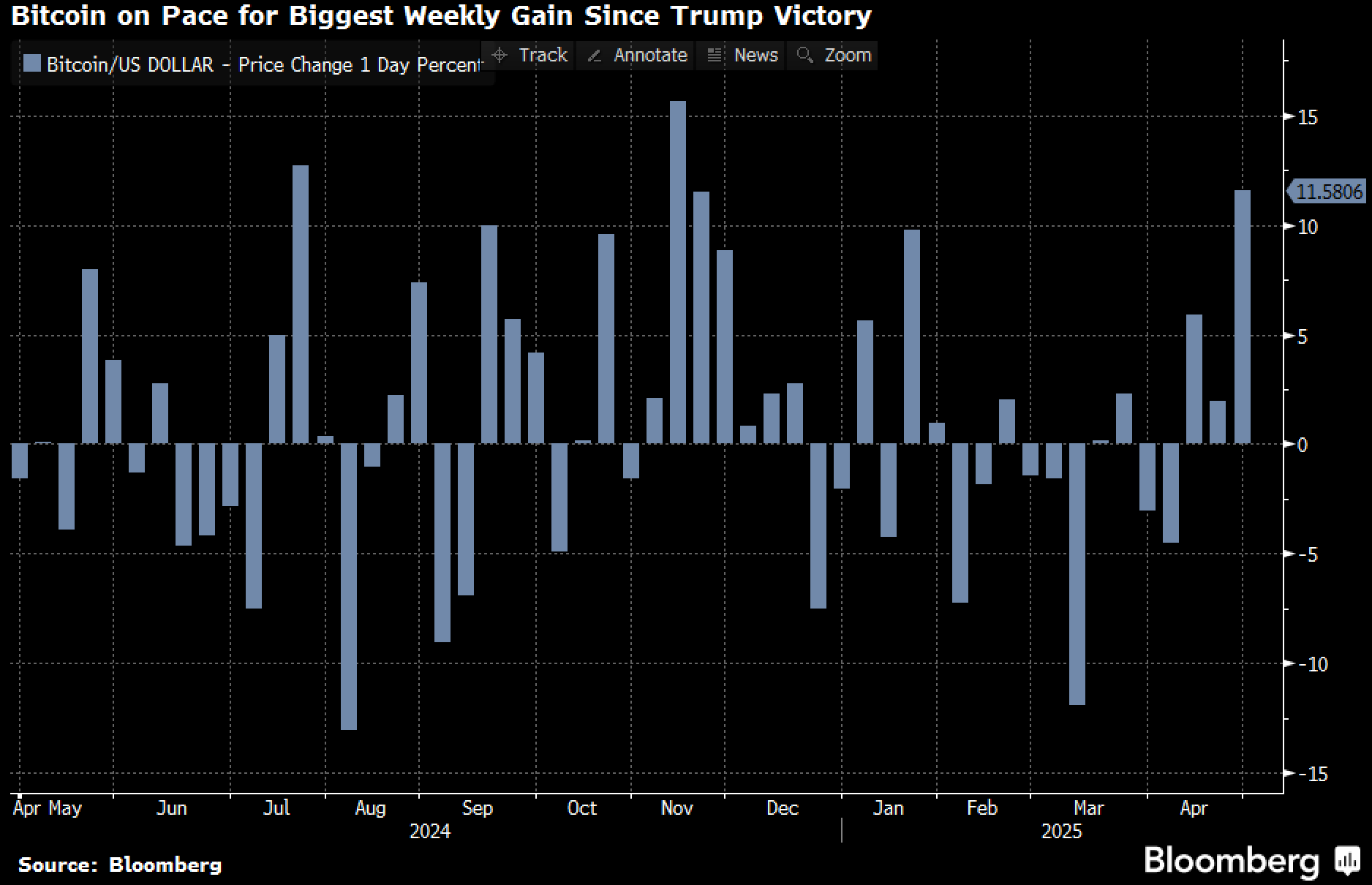

Bitcoin has been a key benefactor of the USD swoon, with BTC outperforming both the Nasdaq and gold in April, enjoying one of the best weeks since Trump’s election victory.

Bitcoin has Outperformed Both Tech Stocks and Gold on a MTD Basis

And for One of the Best Weeks Since Last November

The narrative of BTC as an alternative safe haven continues to grow, as seen from the steady rise in BTC dominance since 2023, indicative of a consistent sea-change in investment narrative, rather than FOMO driven behaviour.

Bitcoin Dominance has Been Trading Up Steadily and Smoothly, Indicative of a Slow But Steady Change in the Investment Narrative

Source: TradingView

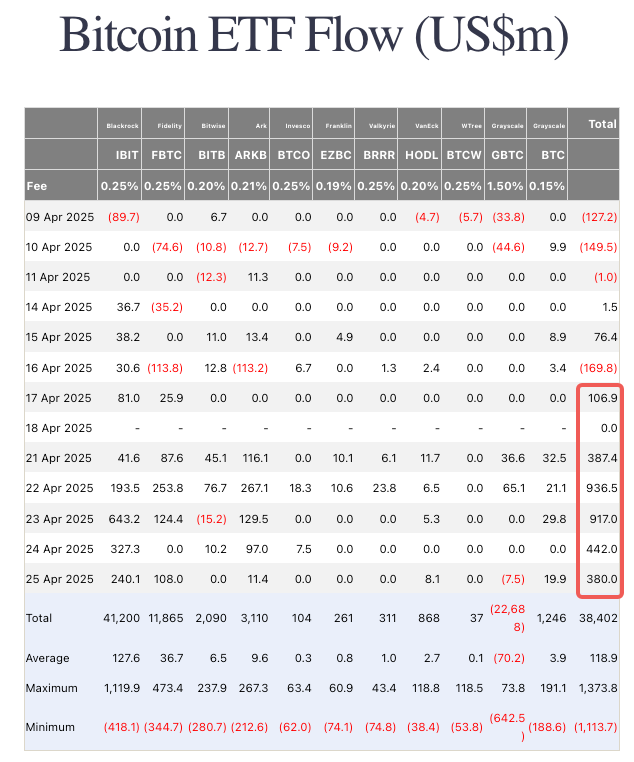

ETF inflows have recovered along with the improvement in risk appetite, seeing 6 consecutive days of inflows to recover from the Q1 swoon, with prices breaking out decisively against the downward trendline at around $88k.

BTC Inflows have Recovered Smartly in the Past Week as Prices Broke Out Against the Negative Trendline

Source: Farside Investors

One of the recent and prevailing narratives suggest that BTC is about to break higher as a delayed reaction to the increase in M2 money supply. While we are not a strict subscriber to this view as there are lot more nuances behind the data, we are bullish on BTC in the medium term due to expectations of monetary and fiscal eases across in response to tariff-driven slowdowns.

This Chart has Been Gaining Attention as Positive Tailwind for Higher BTC Prices

Source: X

In the meantime, we expect to also see some return of FOMO behaviour, though not necessarily in DeFi-native land, as TradFi investors have started to pile into the latest Bitcoin SPAC announced between Cantor, SoftBank, and Tether.

Keep an eye out in this space for FOMO behaviour to flow back into crypto from TradFi markets, rather than vice versa, as future mania will likely be driven by mainstream investor behaviour crypto-beta assets become more prevalent across traditional venues.

The Next MSTR? The Latest Cantor-Softbank-Tether SPAC has Seen FOMO-Like Behaviour from TradFi Investors

Looking ahead, GDP figures are due from the US and Europe, with additional inflation readings out of Europe and NFP jobs data out on Friday. The BoJ is expected to keep rates steady at 0.5% on Thursday with the Fed already in communication blackout ahead of the May 7th decision.

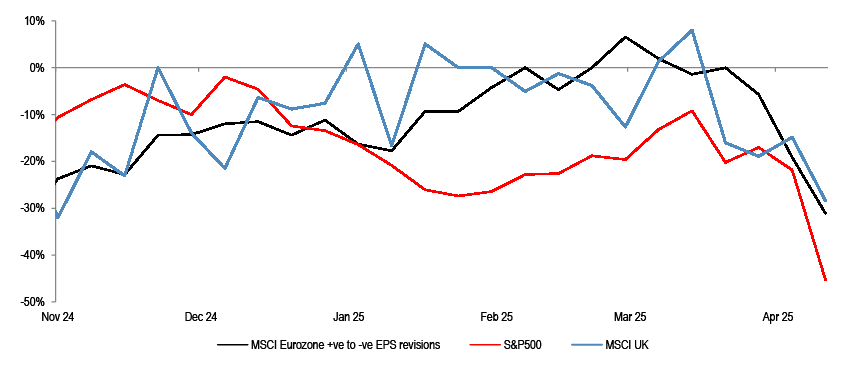

Over in equities, over half of the Mag-7 members (Microsoft, Meta, Amazon, Apple) will report this week against drastically lower EPS revisions.

As such, we expect markets to shift their focus to economic releases and earnings reports, and tune out some the cacophony of trade-related noises for this week. Good luck and good trading ahead!

Earnings Season will Pick Up Against Drastically Lowered EPS Revisions

Source: JPM