Risk assets have recovered sharply to levels that are now challenging even the most ardent bears on whether this is still a dead cat bounce or the beginning of a new bull market. While we think labels are often unhelpful and misleading, the pain trade remains for higher prices and that remains the path of least resistance in the near term.

Beginning with macro, we are certainly nearing the latter half of the drama with trade deals starting to be signed with US trading partners. The inaugural deal goes to the UK, where the big win was a cut of all US steel import tariffs from 25% down to 0%, along with smaller wins with a reduction in auto tariffs to 10% and a new $10bln Boeing procurement deal. Interestingly, the minimum 10% reciprocal tariff rate remains, though that is less of an issue here with the UK being a net trade importer.

More importantly, the much anticipated trade talks with China appear to be bearing fruit, with positive rhetoric coming out of the weekend meeting with Vice Premier Lifeng stating that trade discussions were ‘constructive’, and Treasury Secretary Bessen affirming ‘substantial progress’ being made by both sides. Markets are rallying strongly in the early Asian hours (HSI +2%) on the back of the thawing trade tensions. Expectations are running high for more trade details to arrive in the US hours later today.

Are We Finally Nearing the End of the Trade Tariff Kabuki?

Source: Reuters

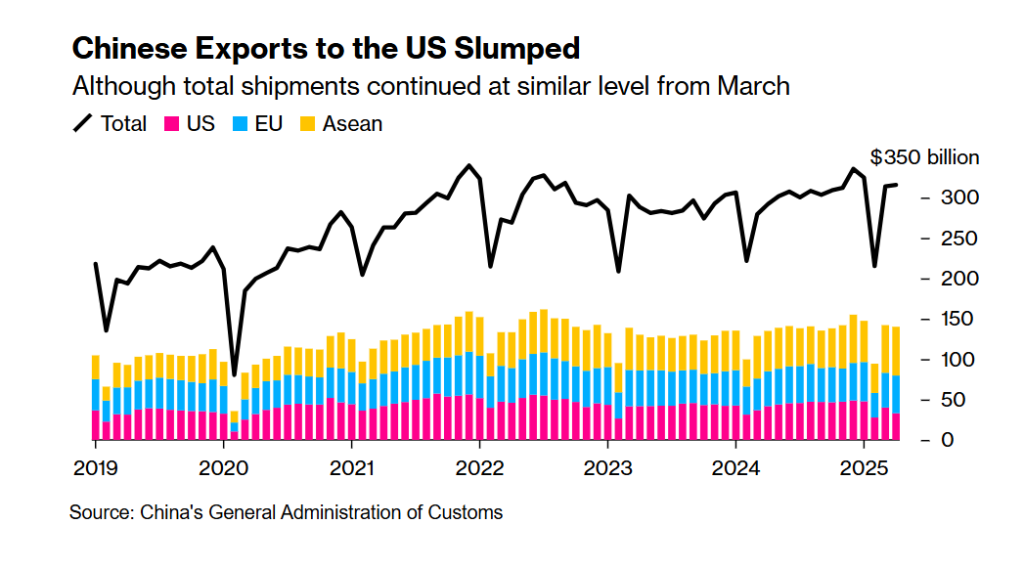

Interestingly, shipping volumes from the China to US had already started to recover since Early May – were exporters ‘front-running’ any deal expectations or did people find a way to pass on the tariffs downstream?

Judging from the resilience in China’s recent export figures, it is probably fair to say that the US will not able to cut its import dependences in the near-term, and any direct cuts in US-China trade will likely be made up by a re-routing of goods to SEA as a ‘tri-party’ solution.

Shipping Volumes from China to US Had Already Started to Recover in May

China Exports Remained Resilient in April with Goods Likely Being Re-Routed to SEA to Avoid Punitive Tariffs

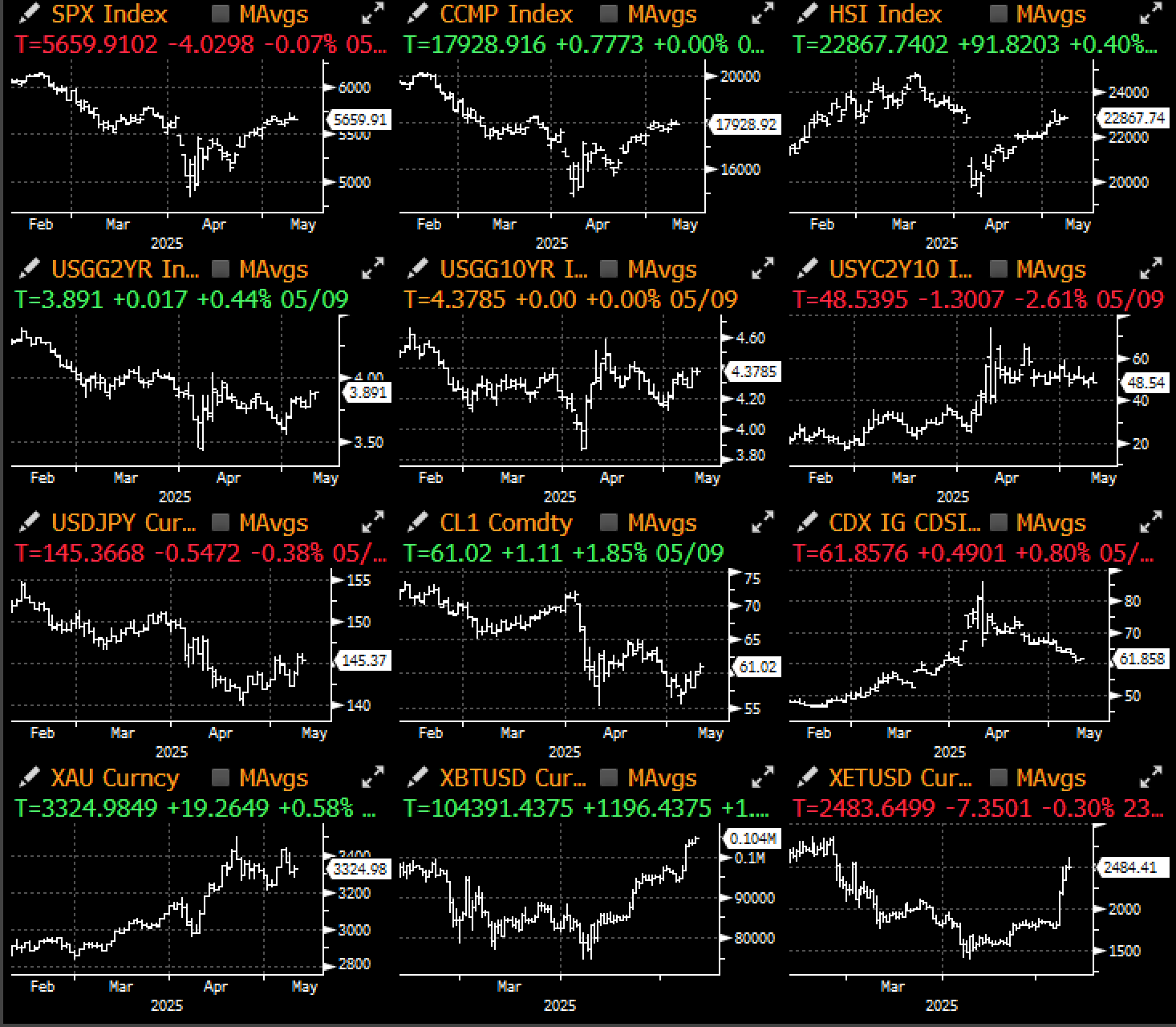

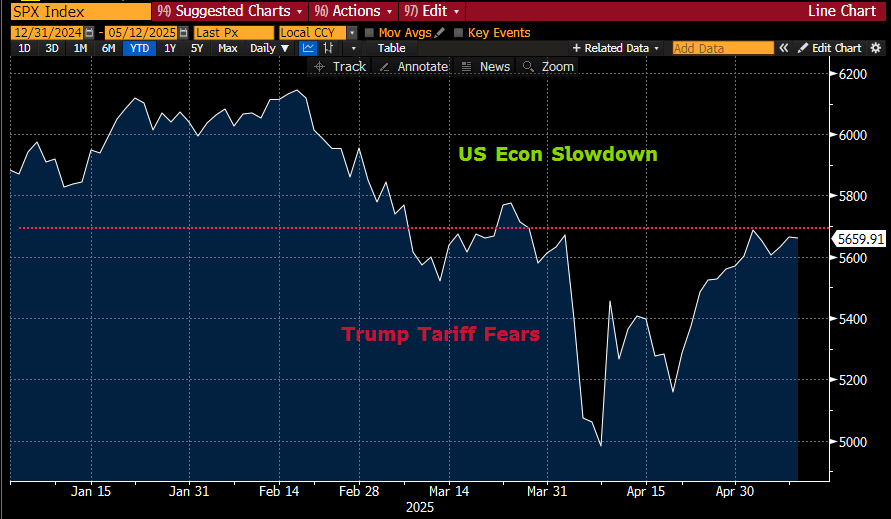

In any case, even before the weekend events, risk assets had already rallied aggressively with the equity VIX sounding the ‘all-clear’ by falling back to below pre-Liberation day levels, and the SPX recovering effectively most of its April losses.

Equity Volatility Has Retraced Back to Pre-Liberation Day Levels

Source: Bloomberg

From a YTD basis, the partial recovery makes sense with markets having effectively moved on from Trump’s tariff-charade, but remains cognizant of the worsening US economic outlook. Any progress to recovering against previous highs will be dependent on the economic path from here.

Who says markets aren’t efficient after all?

SPX Has Recovered All of Its Tariff Related Concerns, But Any Further Progress Will Be Dependent on the Actual Economic Outlook

Source: Bloomberg

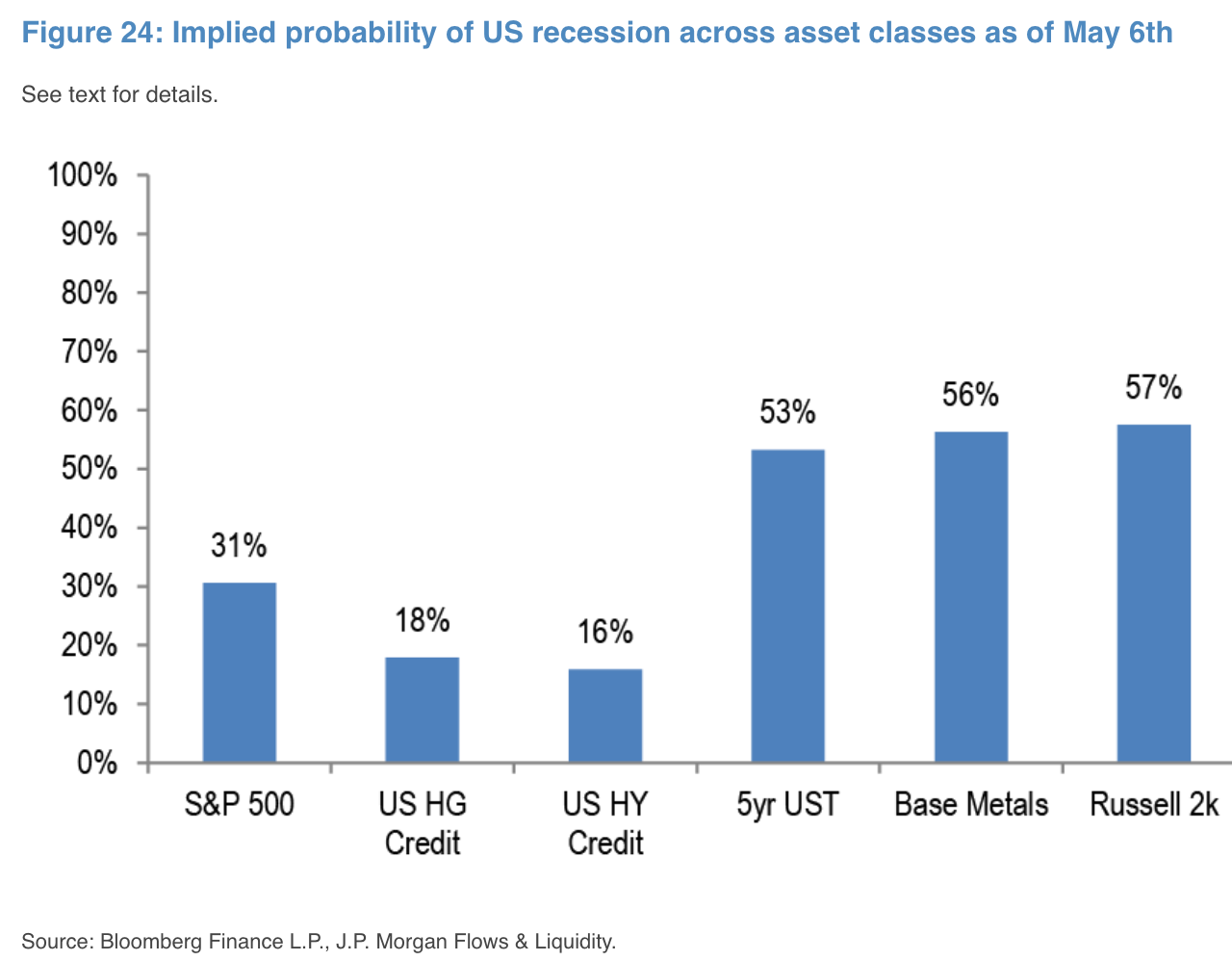

Back to the All-Clear? US Recession Odds are Dropping Rapidly Based on Asset Market Pricings

Source: JPM

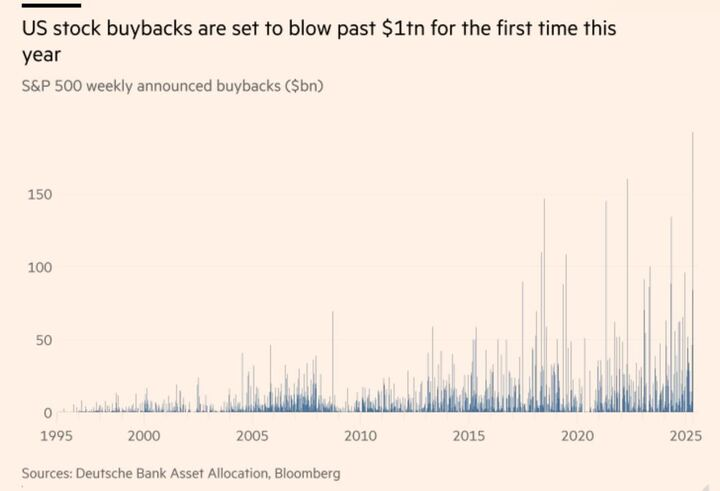

While it’s fair to say that tariff optimism is overpriced for now, it is difficult to fight the tape with US earnings growth still holding in, as well as US companies engaging in stock buybacks at the highest pace ever. Annual US stock buybacks are expected to surpass $1T for the first time in history this year.

Strong US Buybacks

Source: X, FT

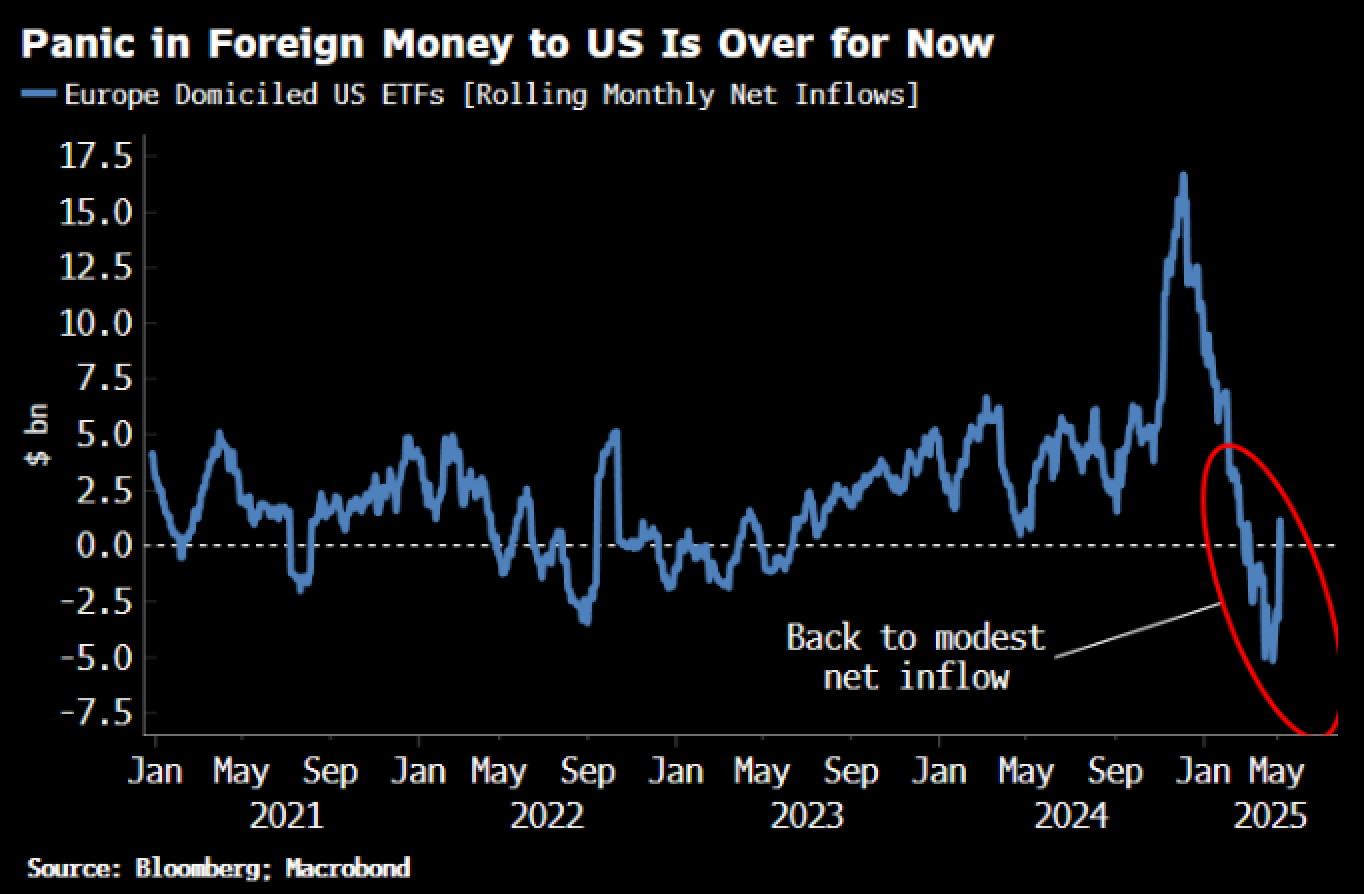

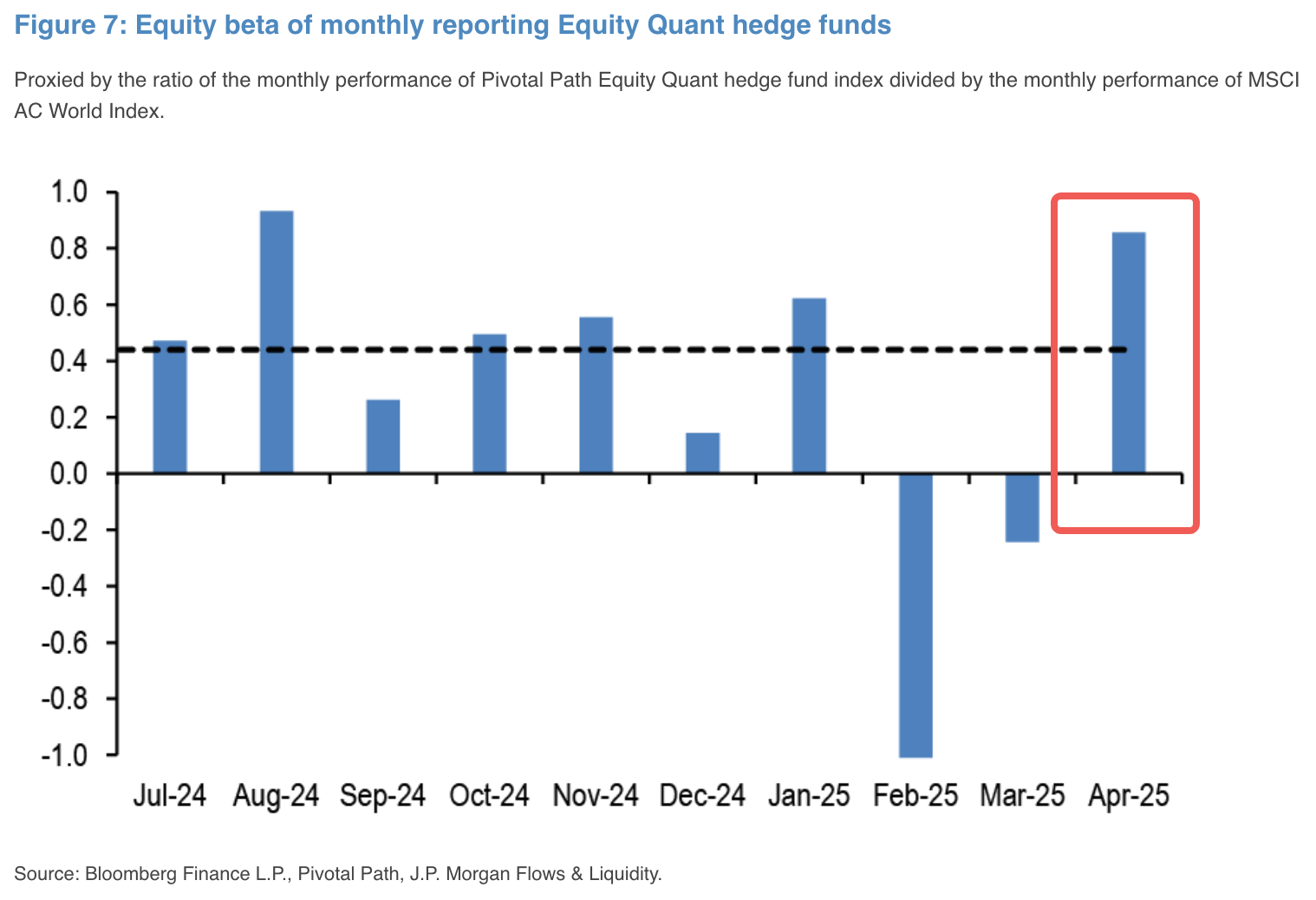

From a positioning perspective, foreign capital has started to return to US markets, along with quantitative funds that have been quick to reverse their Feb-Mar selling into equity longs in April.

Foreign Capital has Started to Return to US Capital Markets

Quant Strategies have Been Quick to Reverse Their Feb/Mar Selling to Participate in the April Rally

Source: JPM

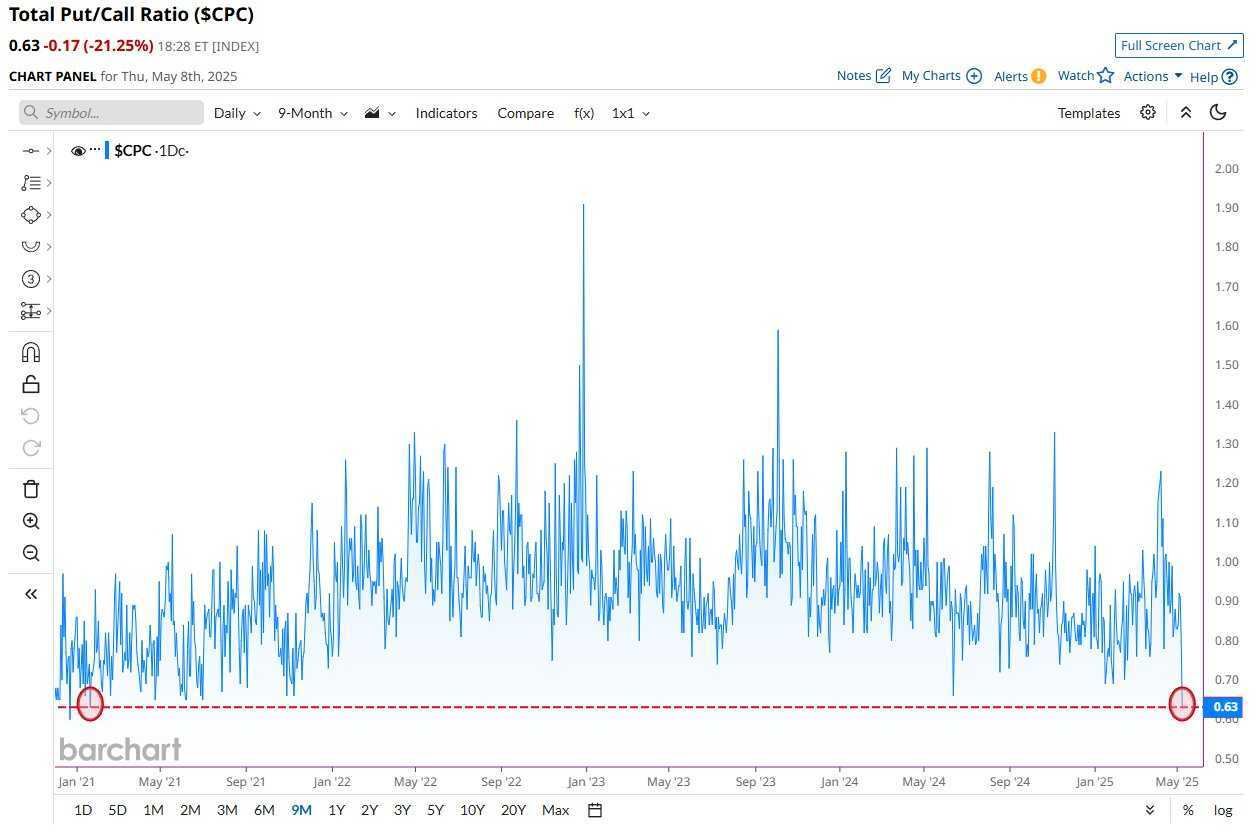

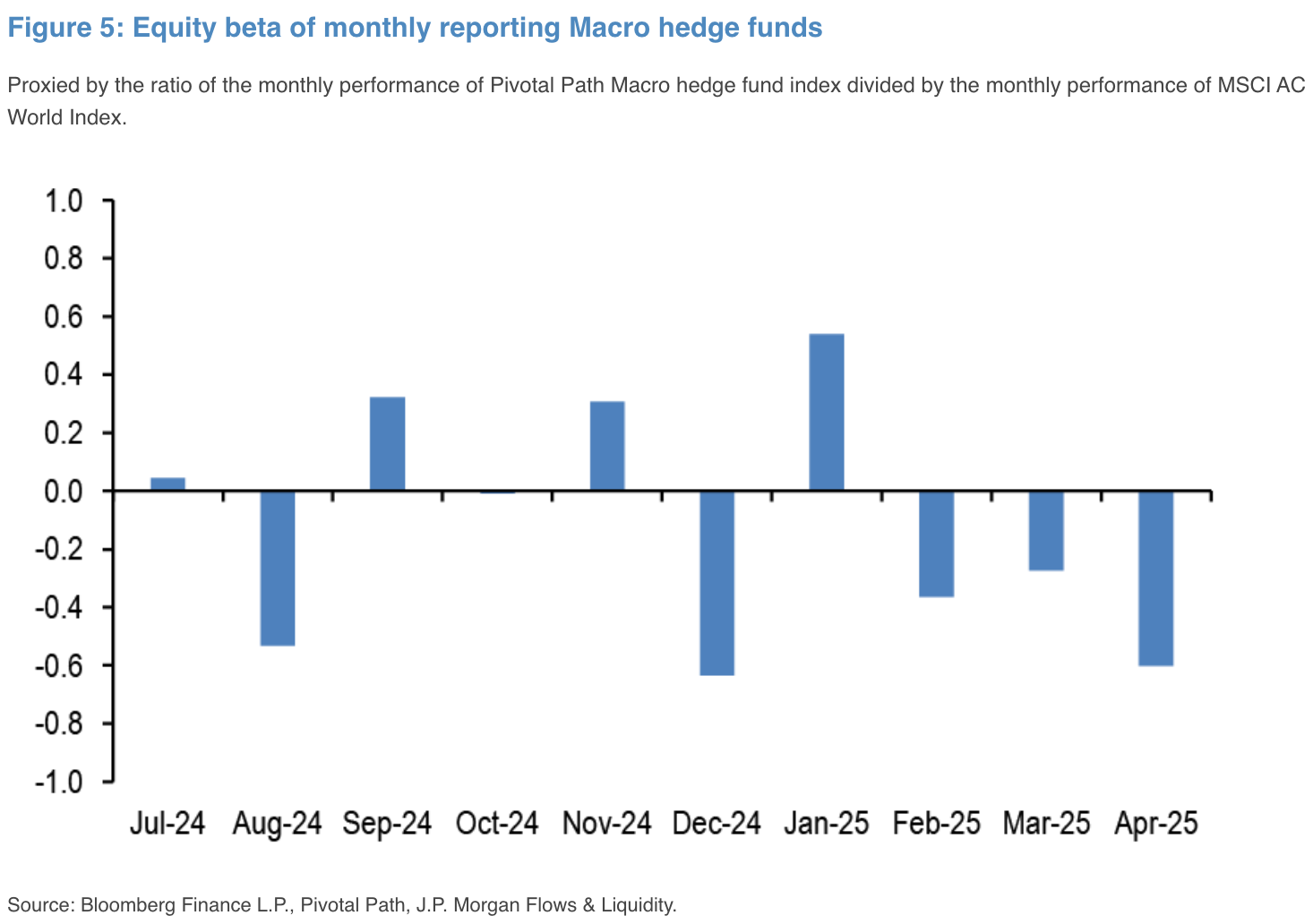

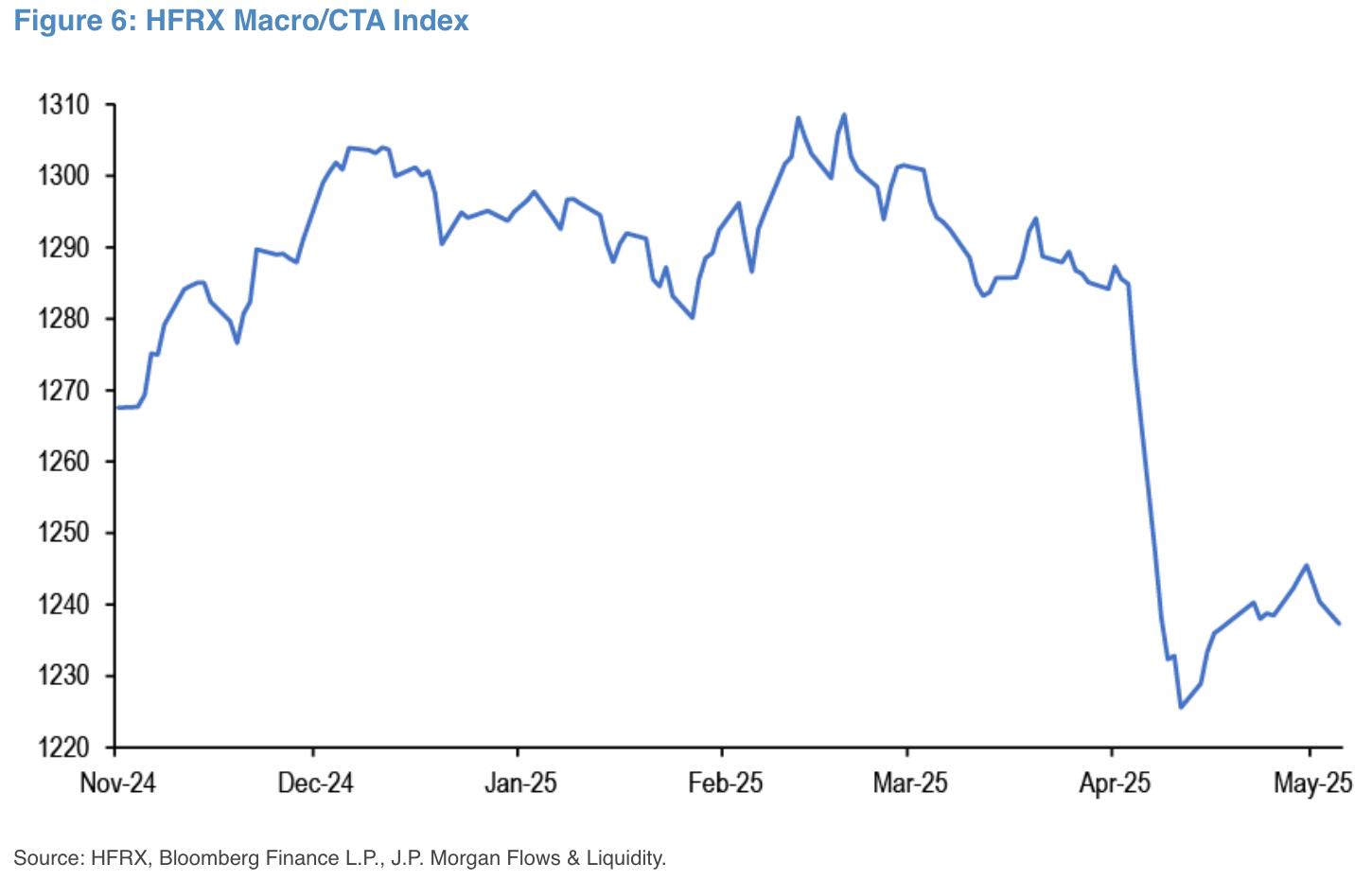

With retail investors remaining as bullish as ever, equity put-call ratios have also fallen to the lowest level in years, leaving only the traditional macro hedge funds being under-invested outliers as they are still recovering the tough PNL drawdown in Q1. We believe that the pain trade remains to be higher prices until more macro bears throw in the towel.

Equity Put-Call Ratio at the Lowest in Years

Source: Stray Reflections

Classic Macro Funds Remain the Bearish Outliers in the Market

Source: JPM

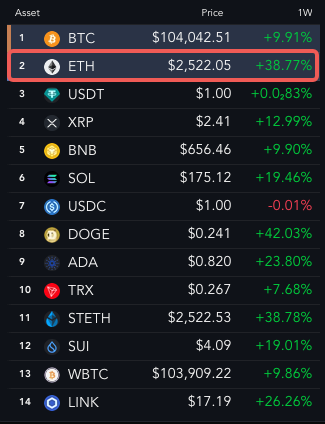

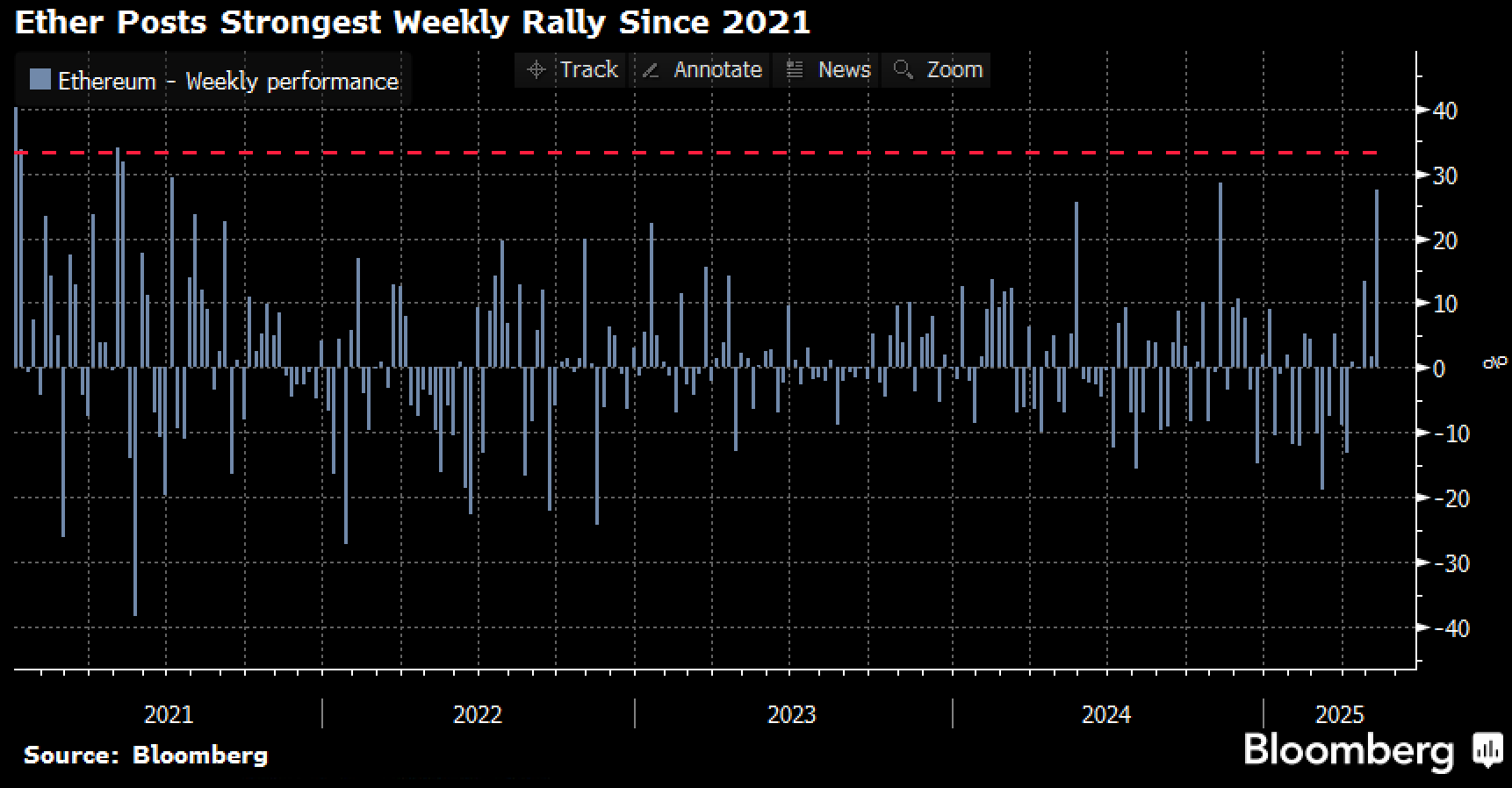

Speaking of squeezes, Ethereum witnessed the largest weekly squeeze since 2021 as the beleaguered token jumped ~40% on the week, far outpacing BTC at +10% WoW as Bitcoin quietly crawls quietly back to ATHs.

Back from the Dead? Ethereum Saw Its Biggest Bounce in Years, Gaining +40% Week on Week

Source: Messari, Bloomberg

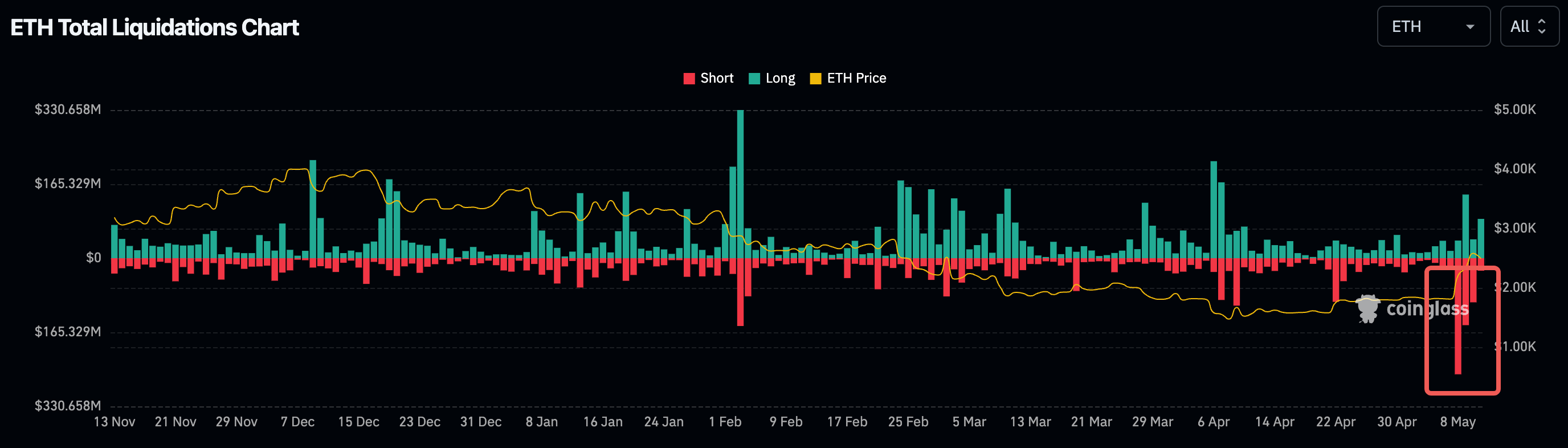

Naturally, markets are looking to fabricate reasons to justify the rally. Whether it be the upcoming Pectra upgrade or something else, we subscribe to the view that this was a classic market short-squeeze against an exceptionally one-sided market, with Coinglass reporting over $1B in shorts liquidation in the latter half of last week, by far the largest wipe-out in recent record.

Ethereum Saw Over $1B in Short Liquidations in the Latter Half of Last Week

Source: Coinglass

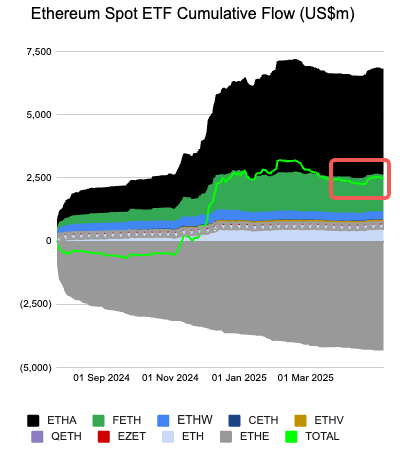

We didn’t see any follow through in ETH ETF buying, suggesting to us that this remains a native short-squeeze event rather than any detectable change in longer-term narrative.

ETH ETFs Didn’t See Any Follow Through in Mainstream Buying

Source: Farside Investors

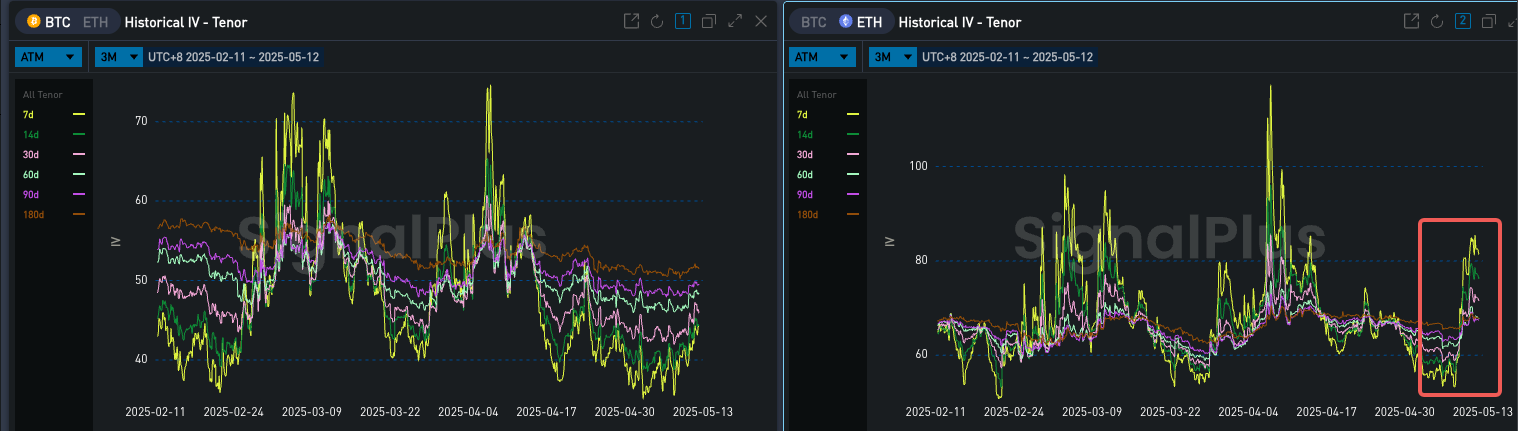

In vol space, implied volatility spiked up following the gap move up in spot, but the vol smile remains negatively skewed in Ethereum vs a positive bias in BTC. In other words, we are not really seeing any new levered longs being placed on ETH despite the move, so we are pretty much in no-man’s land right now as to where prices will go from here.

Implied Vol on ETH Spiked Up Following the Jump in Spot

Source: SignalPlus

But That Has Not Translated to Any Material Buying in Upside Structures as the ETH Vol Smile Remains Negatively Skewed

Source: SignalPlus

Net net, assuming no drastic U-turn in the equity market, we would expect prices to grind up slowly with BTC likely to struggle against interim resistance at $105K, with Ethereum benefitting from the overall rise in the crypto complex. In terms of the safe haven argument, we think that the ‘anti-dollar’ ledge is more structural this time around and investors will be looking to invest into EM, precious metals, and crypto as a portfolio allocation decision away from the USD, and dips will be seen as a buying opportunity from here given overriding geopolitics.

Be patient and don’t fight the tape! Good luck and good trading this week.