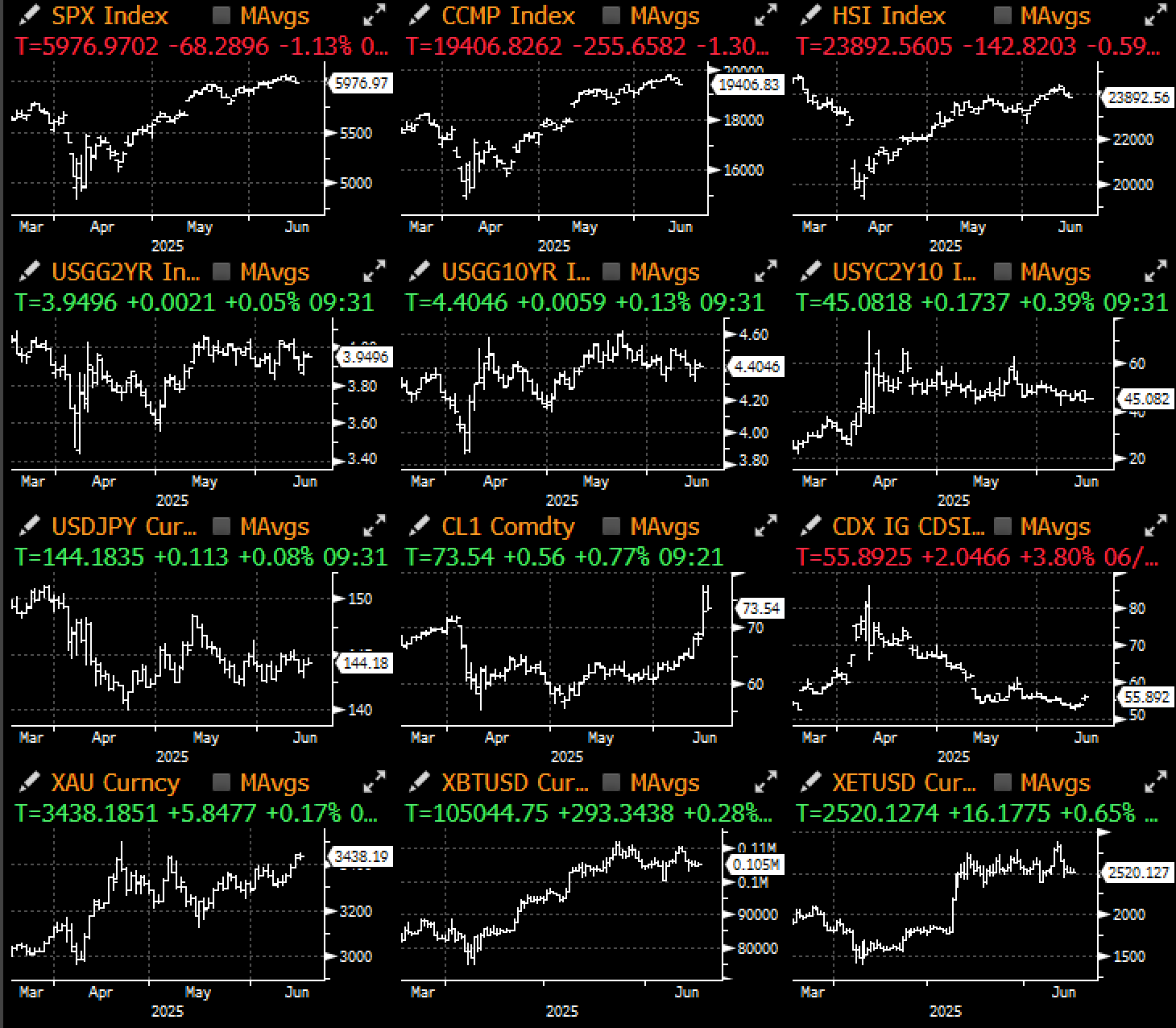

Geopolitics stormed back to the forefront, with Israel’s attack on Iran’s facilities, and the latter’s subsequent response spiked oil prices and weakened risk sentiment on Friday. With markets rightly concerned about further escalation risks, Iran’s possible closure of the Hormuz canal, and as well as the US’s potential response to the conflict, would influence where oil prices go into the peak US driving months.

Oil Prices are Back in Play as a ‘Risk’ Asset With the Worsening Israel-Iran Conflicts

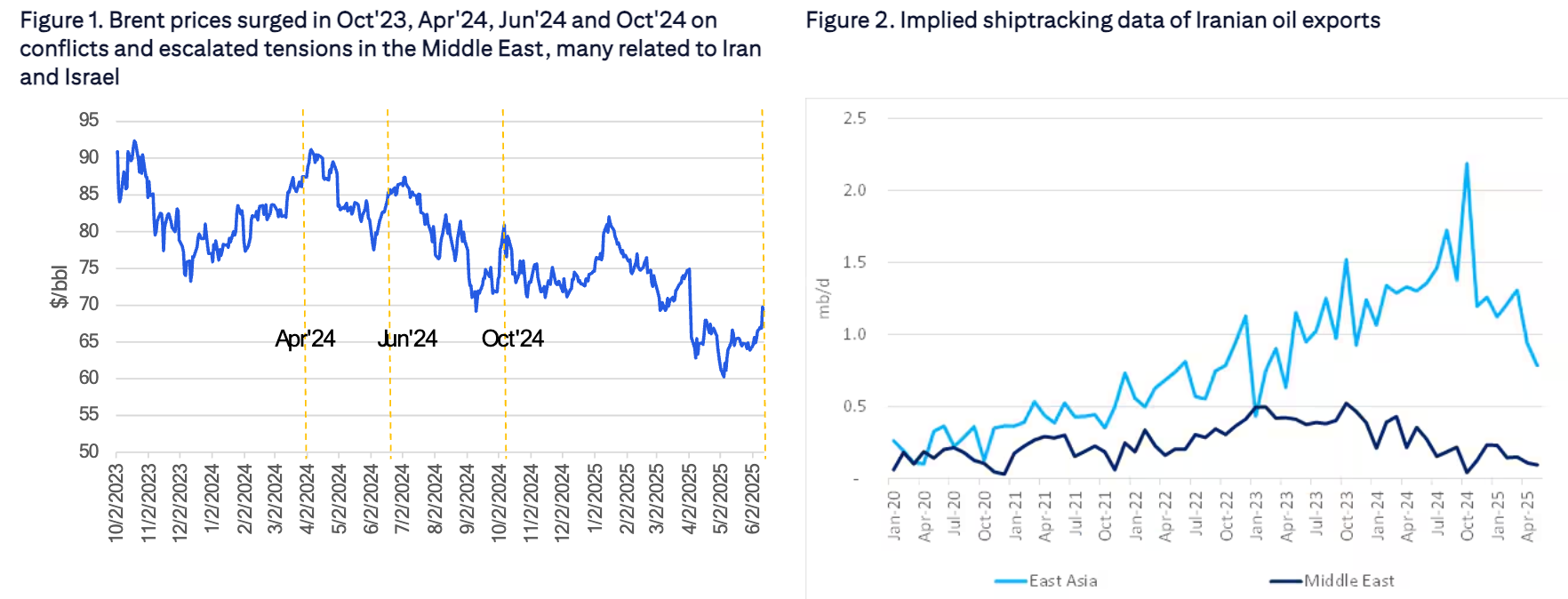

In the meantime, the price rally has stalled against the falling 2yr trend line, and more convincing break upwards will likely spell issues for risk sentiment in the near term. However, Street consensus suggests that energy disruptions should be limited, such as with rising production out of the Saudis, though the most sustainable forward would still have to be through diplomacy.

Oil Prices Stalling Against Multi-Year Trend Line

Source: Bloomberg

Wall Street Expects Oil Disruptions to be Minimal and Short-Lived, Similar to Prior Episodes

Source: Citi

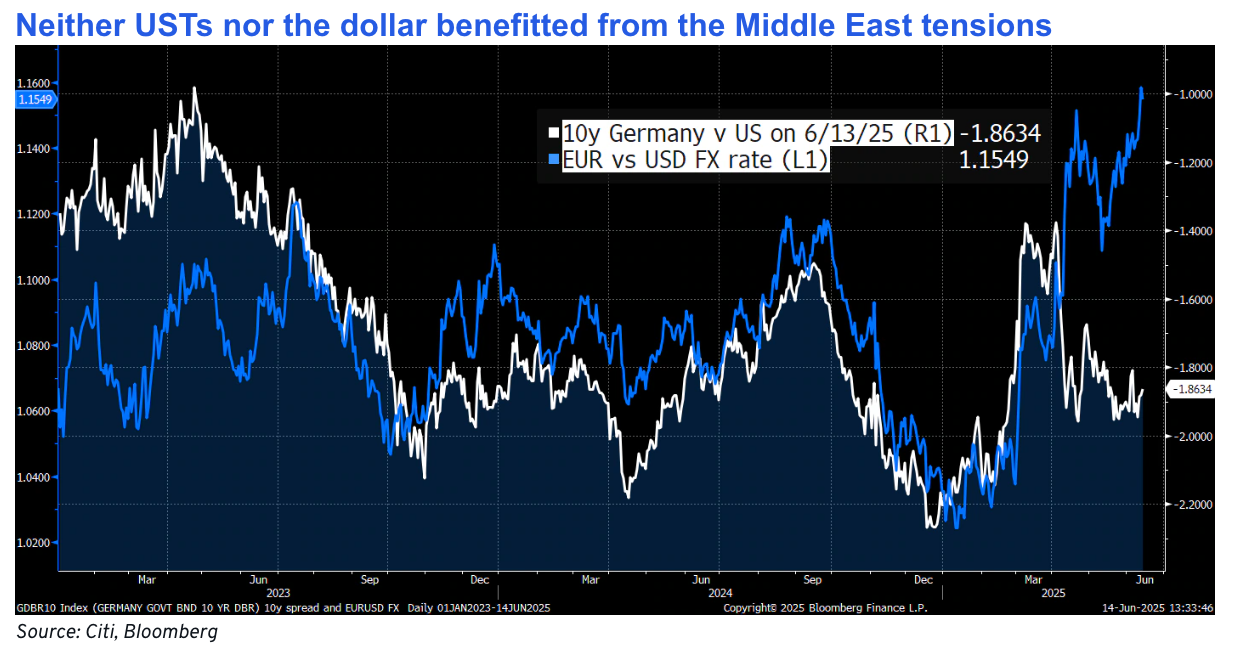

A more interesting take away is how the US$ and US Treasuries have failed to see any real ‘flight-to-quality’ bids throughout this move, indicating that the world remains more worried about US capital flow concerns than the situation in the Middle East. This is certainly not something that hasn’t gone unnoticed.

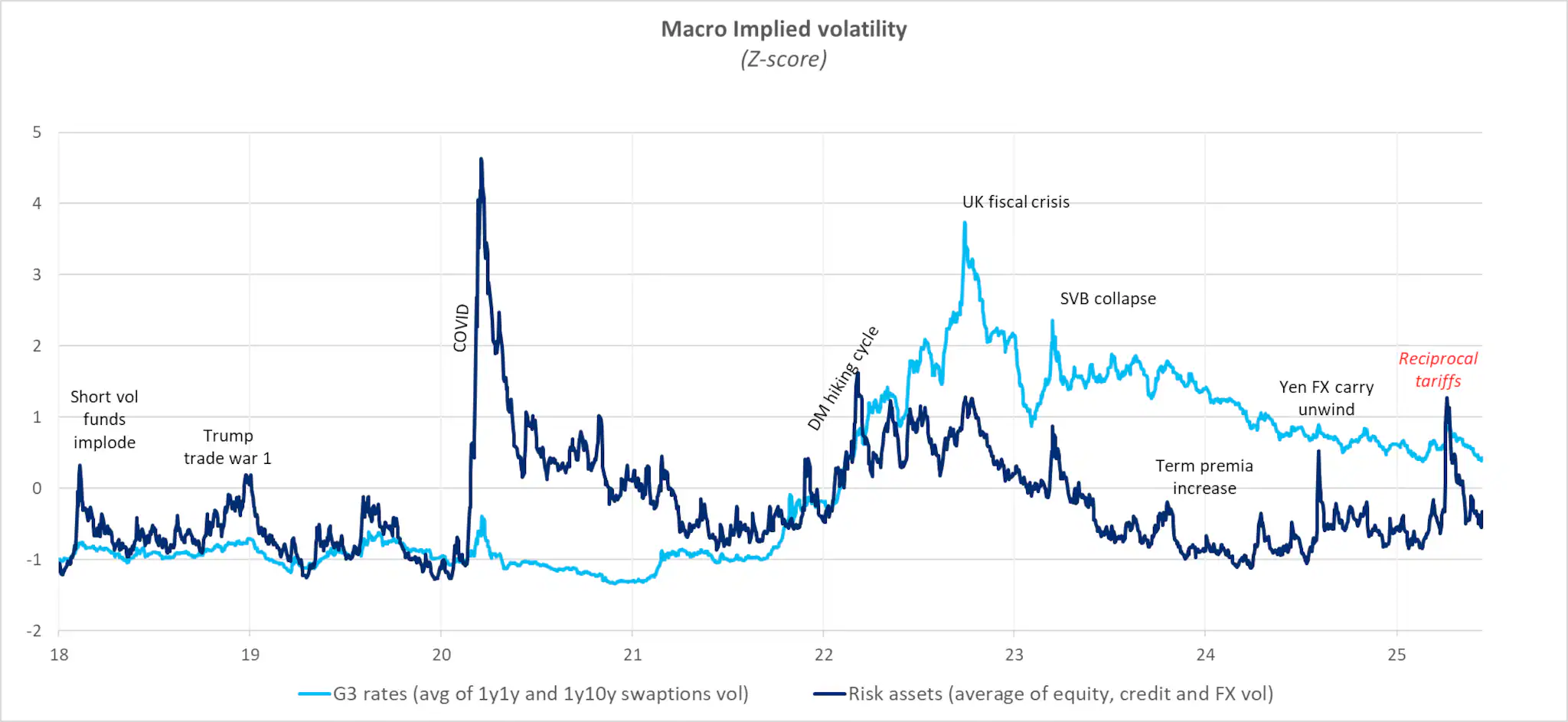

Rates volatility have also regressed back near to multi-year lows, suggesting that macro markets are eager to move on and focus back on tariffs and the economy.

What Volatility? Rate Vol has Retraced All the Way Back to Near Record Lows

Source: Citi

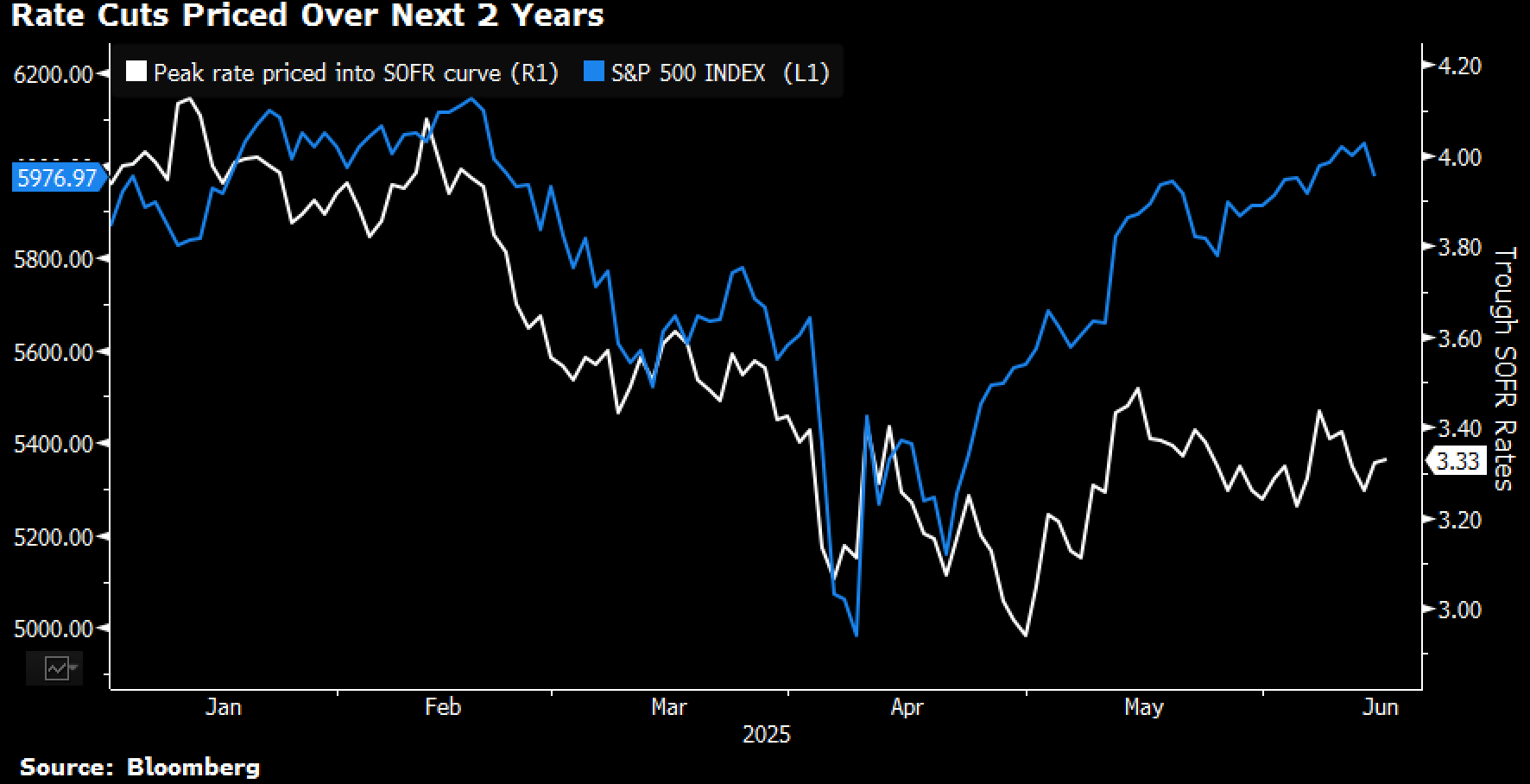

In fact, the conflict has barely made a budge in the rate cutting odds for 2025, where markets are still only expecting just 2 rate cuts before year-end, despite the string of softer than expected inflation prints.

Rate Cutting Odds Barely Budged Despite All the Risk Noise

Source: Bloomberg

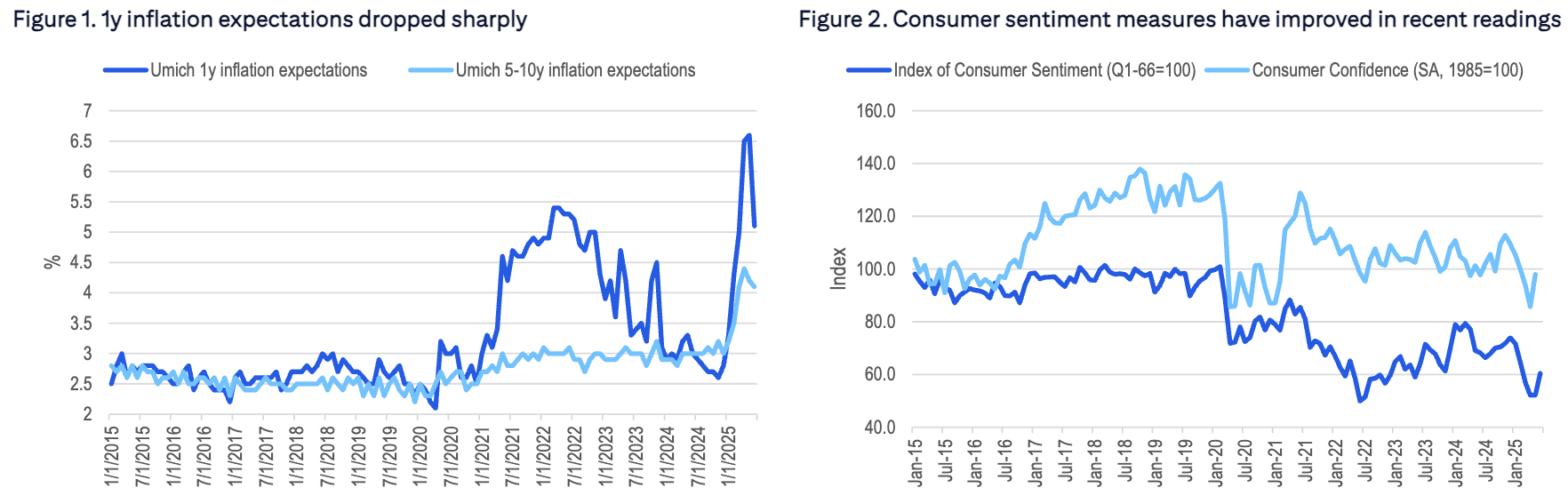

Before Friday’s moves, markets had enjoyed a string of lower inflation prints across developed markets (except Japan), with the US showing downsides misses in CPI, PPI, NY Fed inflation & U-Mich inflation expectations.

US Disinflation Story Appears Well and Alive as Per the Fed’s Expectations

Source: Citi

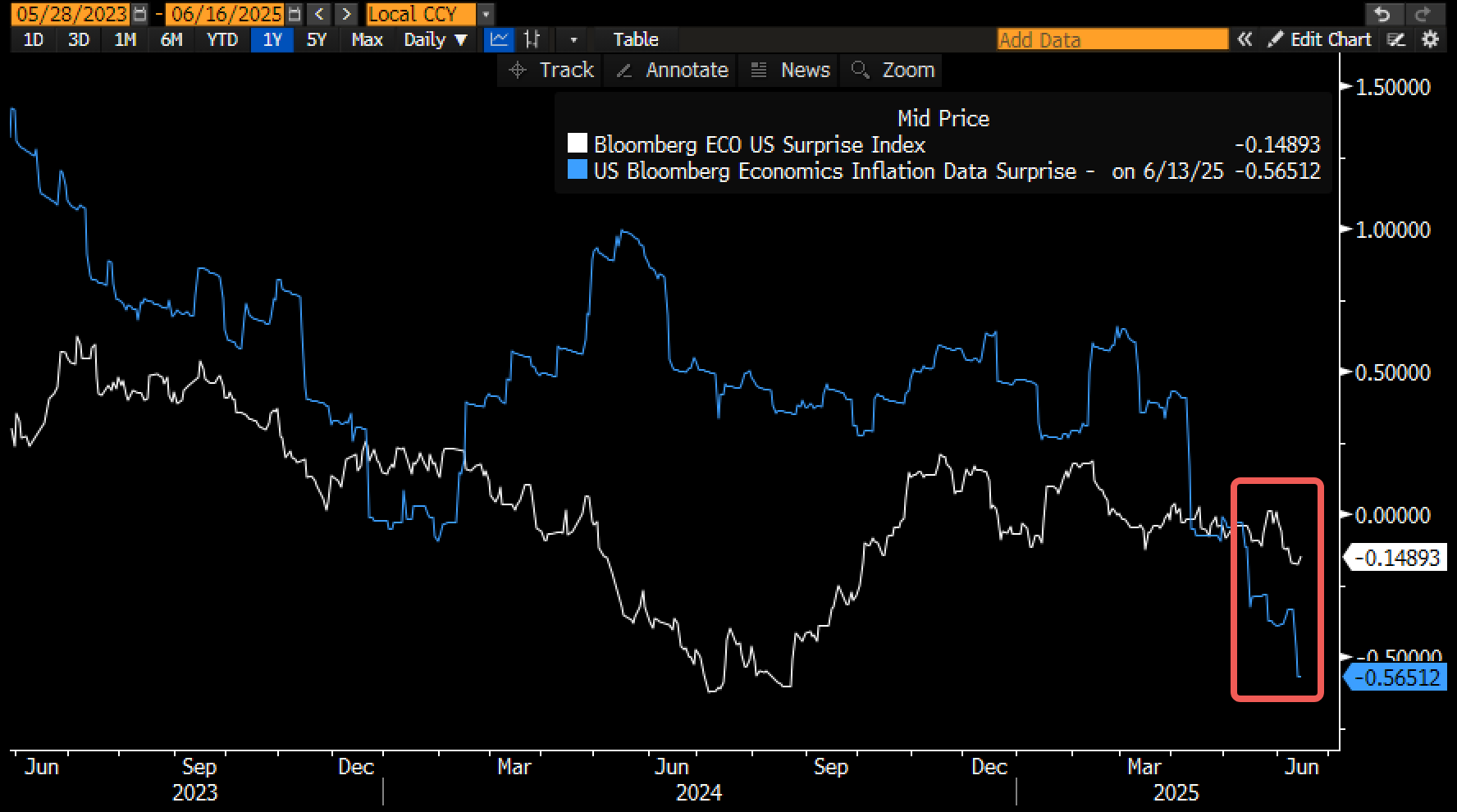

In fact, the recent drop in core CPI was one of the bigger downsides surprises in recent memories, helping to buoy risk sentiment and giving the Fed ample room to keep financial conditions easy.

Recent CPI Miss was One of the Larger Positive Surprises Over the Past Year

Source: Bloomberg

Financial Conditions have Eased Back Significantly Since Liberation Day

Source: Bloomberg

Long/short equity hedge funds have re-added back to their equity longs, taking their net exposures back to some of the highest levels in a year, with the path of least resistance still upwards.

Equity Long/Short Hedge Funds have Rebuilt Their Longs in April and May

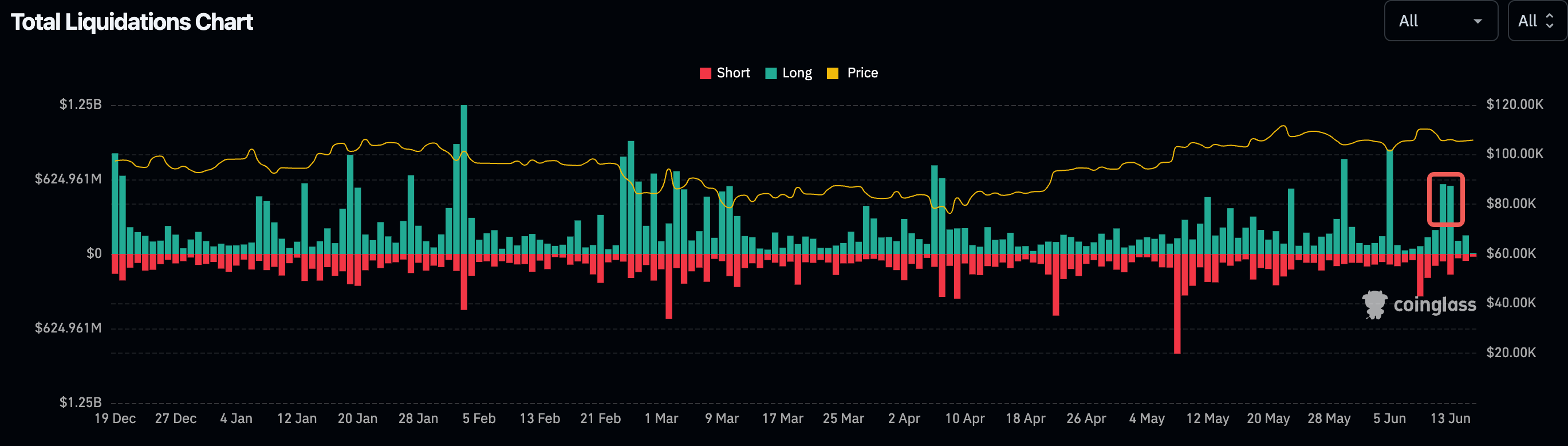

Crypto reaffirmed its status as a ‘risky’ asset class as token prices fell across the board on the week, with over $1.2bln in futures liquidated on Friday as prices retreated along with the equity swoon. Altcoins led the decline on Friday with BTC settling back into the 105k area helped by steady ETF inflows and public treasury vehicles.

Crypto Prices Sold Off Along with Significant Long Liquidations Observed Last Friday

Source: Messari, Coinglass

BTC Continues to Track the (Leveraged) Nasdaq Quite Closely

Source: Bloomberg

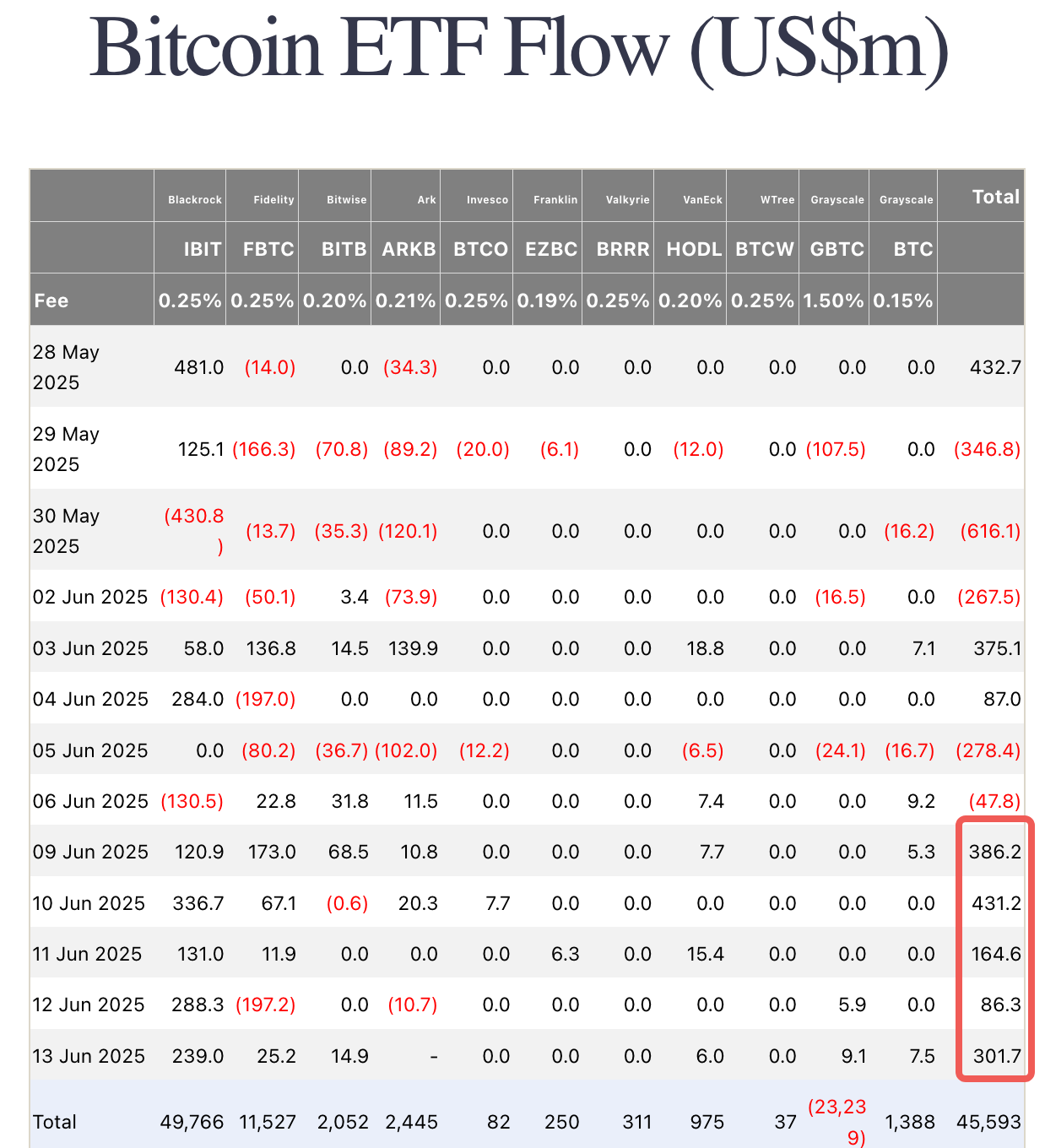

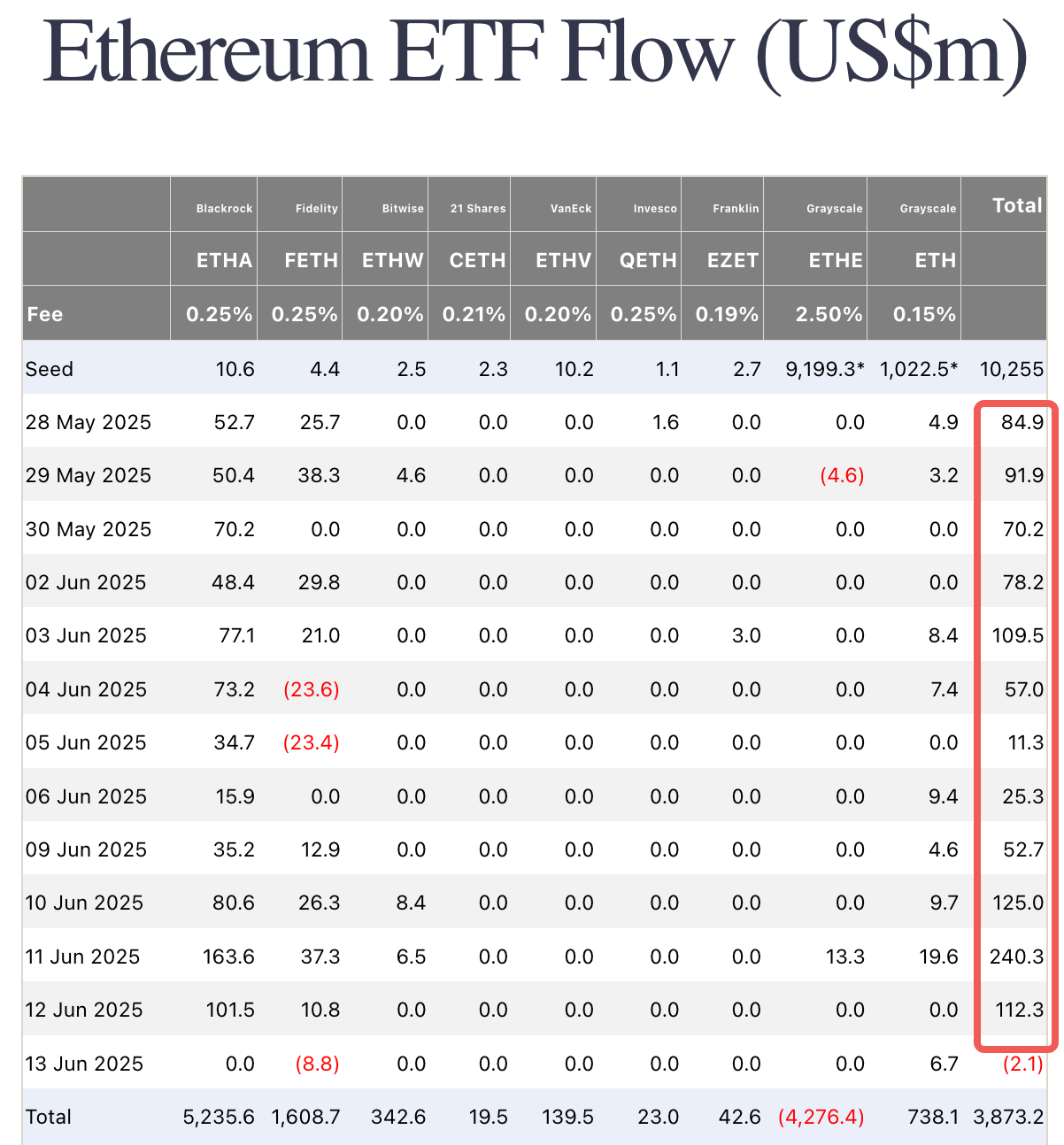

BTC ETFs saw 1.4bln of net inflows, while ETH ETFs just broke a streak of 2+ weeks of consecutive net buying as TradFi participation remains healthy. We expect prices to continue to follow the equity sentiment into the summer, with a slow grind higher in prices.

ETF Inflows has Remained Consistently Positive Through The Move

Source: Farside Investors

This will be a week of Central Bank meetings (Fed, BOJ, BOE, Norges, SNB, though we don’t expect a lot of surprises for the market. The Fed will likely see some dovish risk on the margin, and the market will see whether the committee will use the recent string in downside inflation misses and weaker jobless claims to justify a more pronounced dovish pivot. We don’t expect a whole lot out of the meeting and the near-term focus will remain on the Iran-Israel situation, in particular to any kinetic escalation or dangerous political moves, with the US still bogged down in various tariff and budget negotiations. Good luck & good trading.