Not a whole lot of to report this week, as the S&P 500 brushed off the post NFP shock to recover back close to their ATHs. On the other hand, Nasdaq managed a new record thanks to strong earnings reports, brushing off the ongoing political drama with the Trump administration & new import taxes.

US Growth Stocks have Roared Back with a Vengenence

Risk assets did well globally as well, with European and Japanese stocks rallying on continued trade resolutions, with the US making concessions on tariff stacking and reduction on car taxes.

European & Japanese Stocks Outperformed on Positive Trade Resolutions

On the other hand, the US-China trade truce will expire this week, with some participants expecting the deadline to be extended again, though there are concerns that new tariffs will be levied for Chinese buying of Russian oil, which was recently assigned to India for the same offense.

US Mulls Additional Tariff Threats on Trading Partners’ Buying of Russian Oil

Source: BBC

On the positive side, US & Russia are slated to draft a new Ukraine peace deal ahead of the Alaskan Summit this week, giving yet another tailwind to risk assets, and depressing oil prices with the war premium continuing to come down.

Oil Prices have Softened as Geopolitical Conflicts Continue to Fade

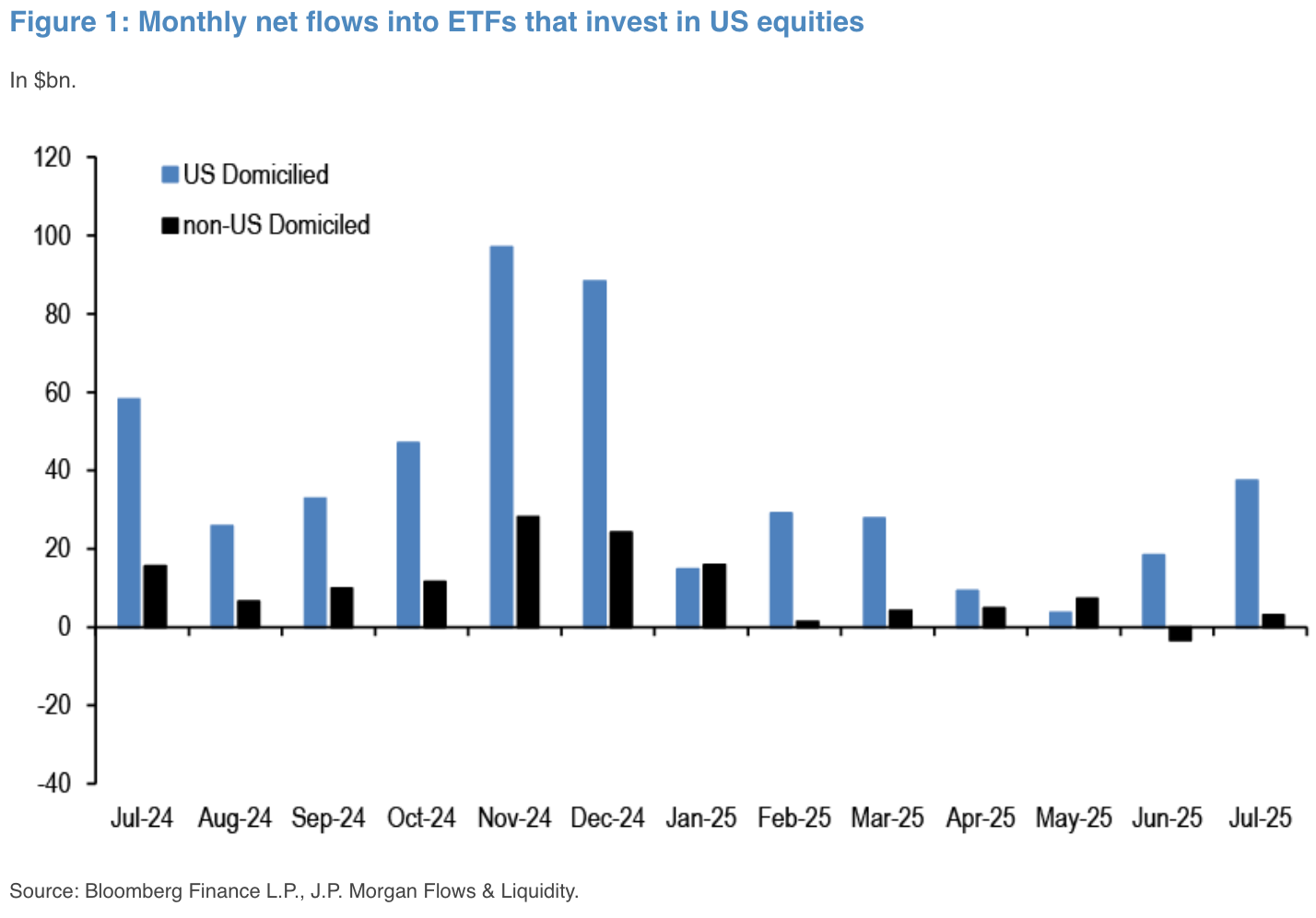

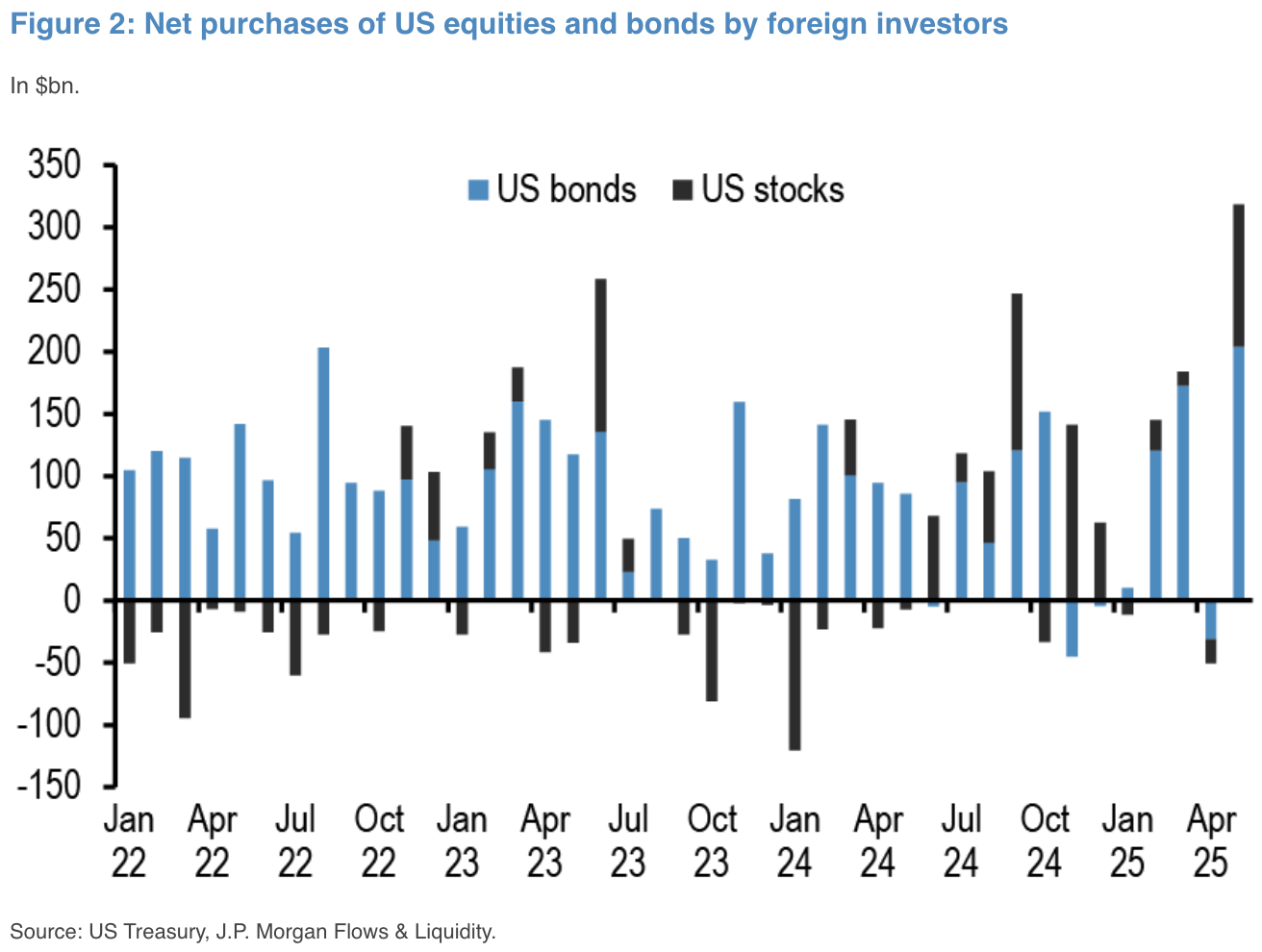

US capital flows remain strong as both domestic and overseas investors returned en masse, with net purchases showing record monthly inflow in the most recent data, with trading volumes also breaking to new highs as a positive confirmation.

Both Domestic and International Buyers Returned to US Assets En Masse Over the Recent Months

Source: JPM

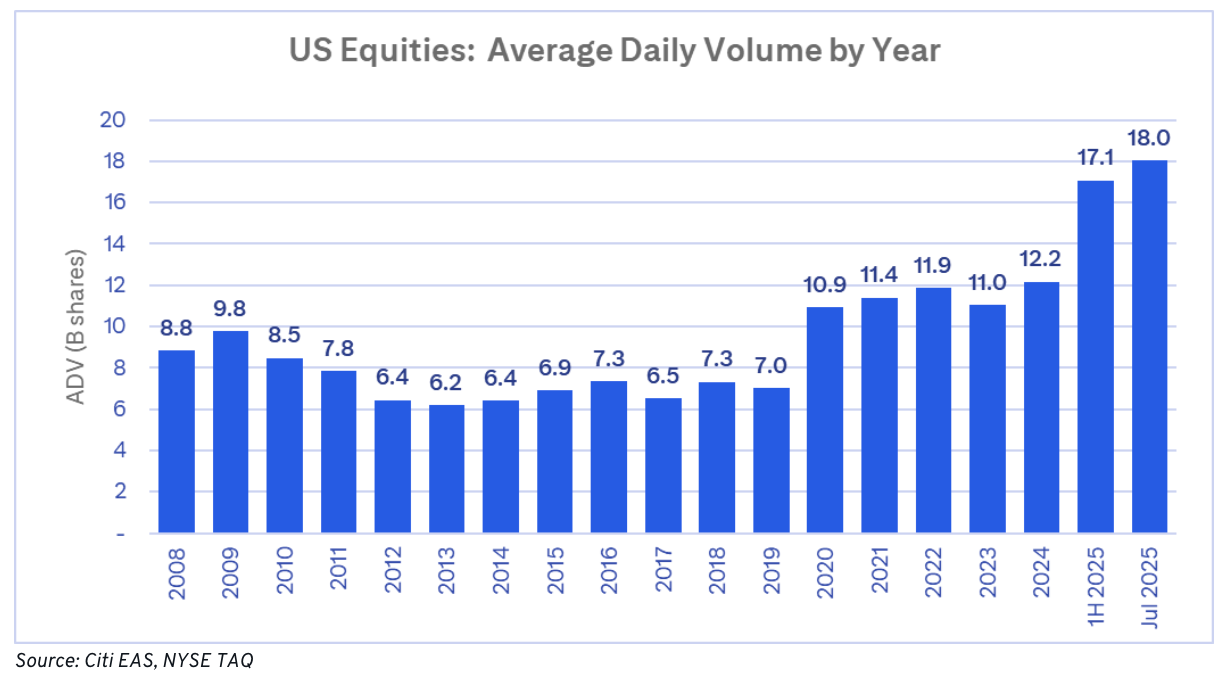

US equities have experienced record-breaking trading volumes in 2025, significantly outperforming prior years, thanks to the strong return of retail trading YTD. According to Citi, the average daily volume (ADV) in 1H25 was nearly 50% higher than the prior 5 year average, and a massive 40% jump from the previous record in 2024. The trend appears to be continued in July with and ADV of 18 billion shares per day.

US Equity Trading Volumes are Trending at a Massive 40% Jump vs the Previous Record in 2024

Source: Citi

In fact, 2025 has been such an incredible year that 17 of the 20 largest volume days in history have taken place in 2025, with 13 days in Q2 alone. Absolutely incredible.

17 of the 20 Largest Volume Days on Record Took Place in 2025, wth 13 in Q2 Alone

Source: Citi

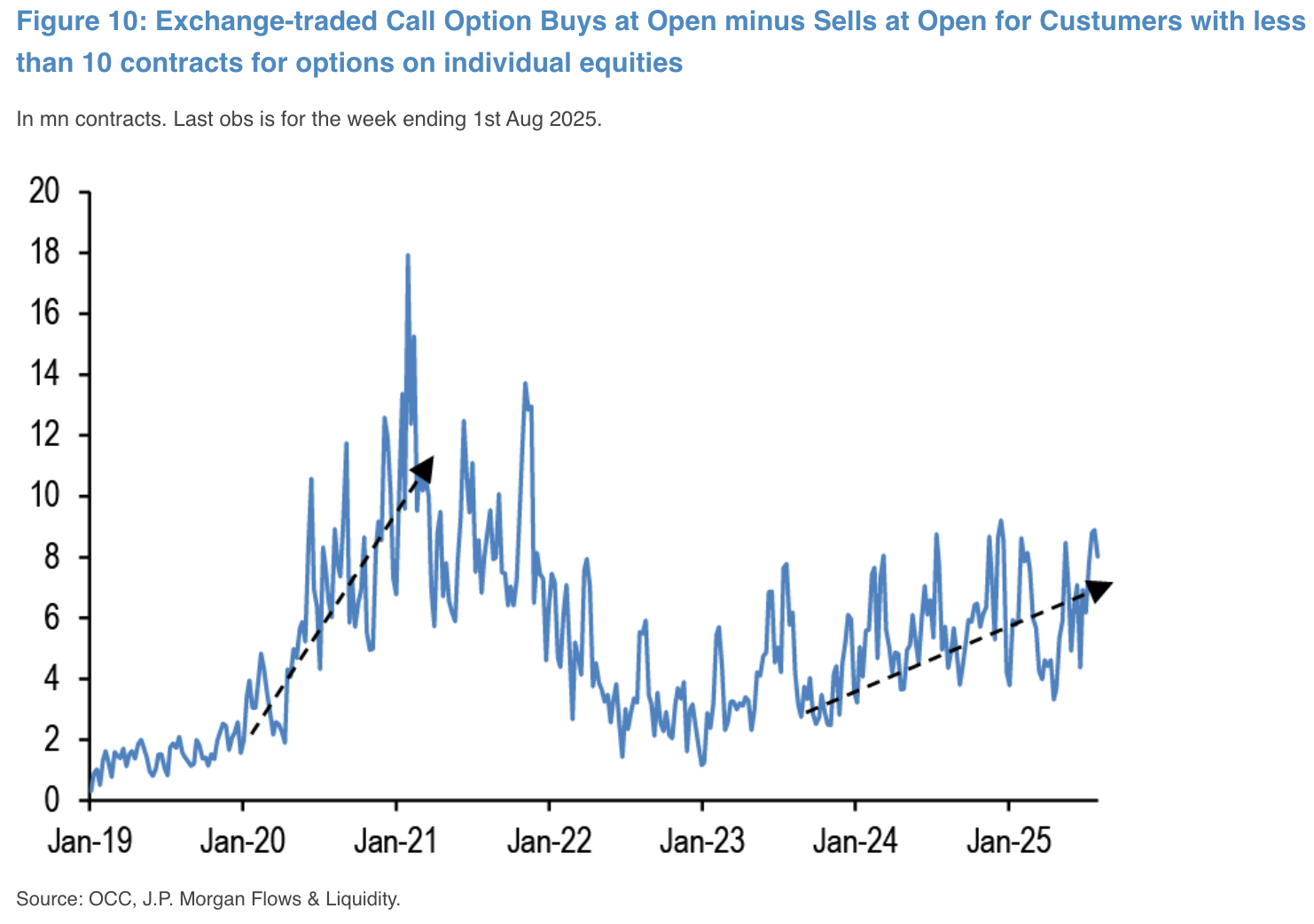

Retail participation has been driving extreme levels of single-stock concentration YTD, with days in 2025 where the top 5 stocks constituted over 20% of total market volume. Retail activity in call option plays have rebounded significantly as well to the highest levels since covid.

Retail Option Activity has Returned to the Highest Levels Since Covid

Source: JPM

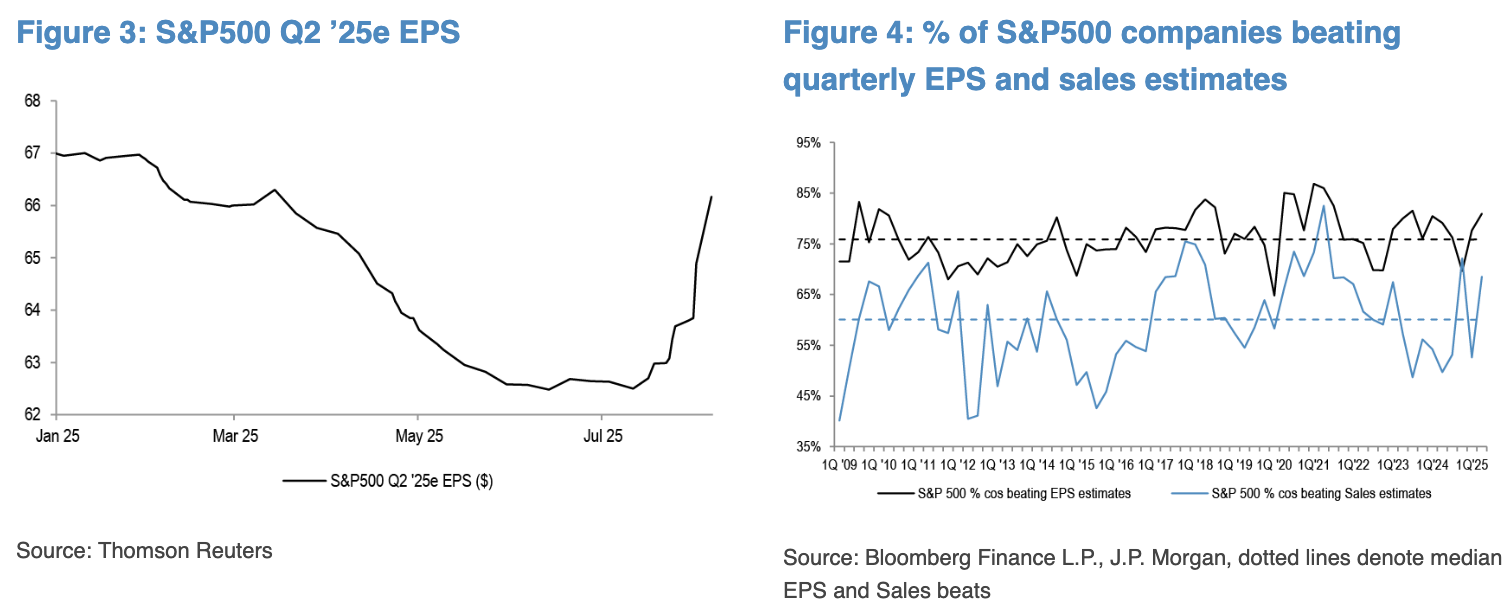

On the earnings front, ~80% of reported S&P 500 companies have beat estimates, with a +12% YoY pace for a +9% positive beat, led by tech and financials. 2Q25 EPS has come in significantly above the lowered expectations post tariff concerns.

S&P 500 Q2 EPS have Come in Significantly Above Expectations, Supporting the Equity Rally

Source: JPM

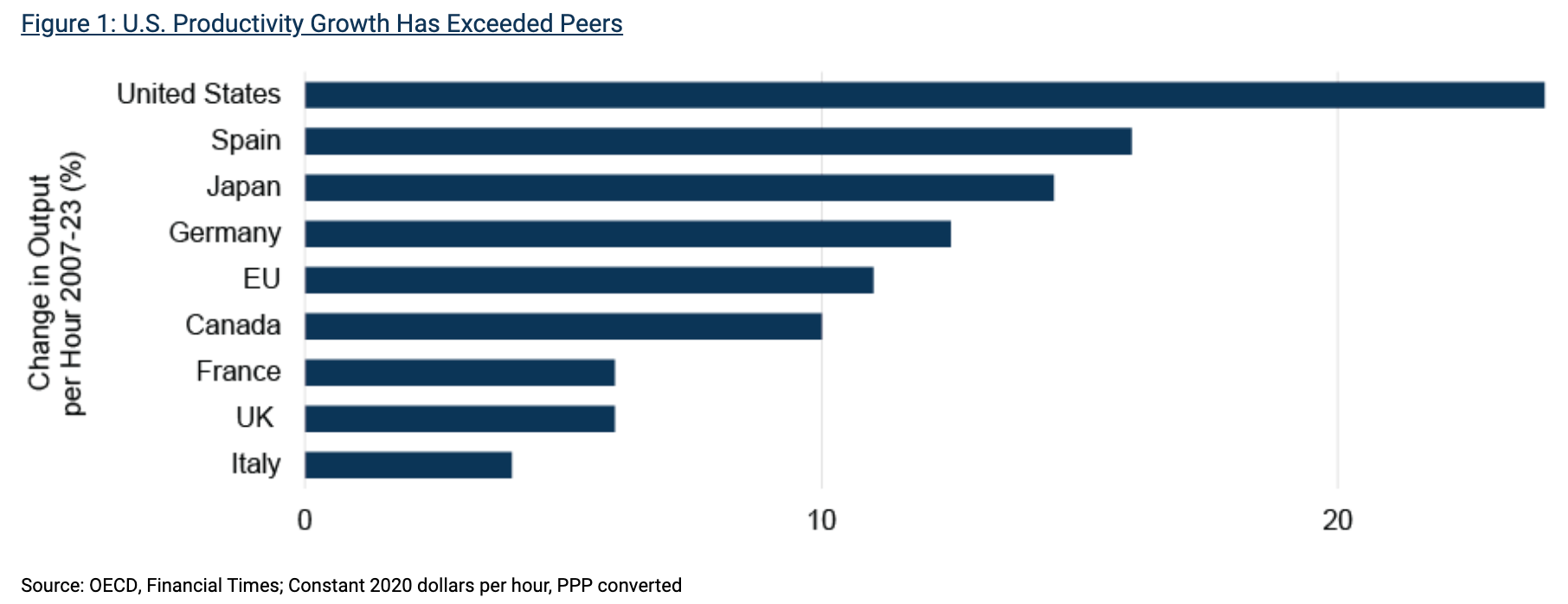

Strong Corporate Performance is Supported by Increases in US Productivity Well Above Global Peers

Source: JPM

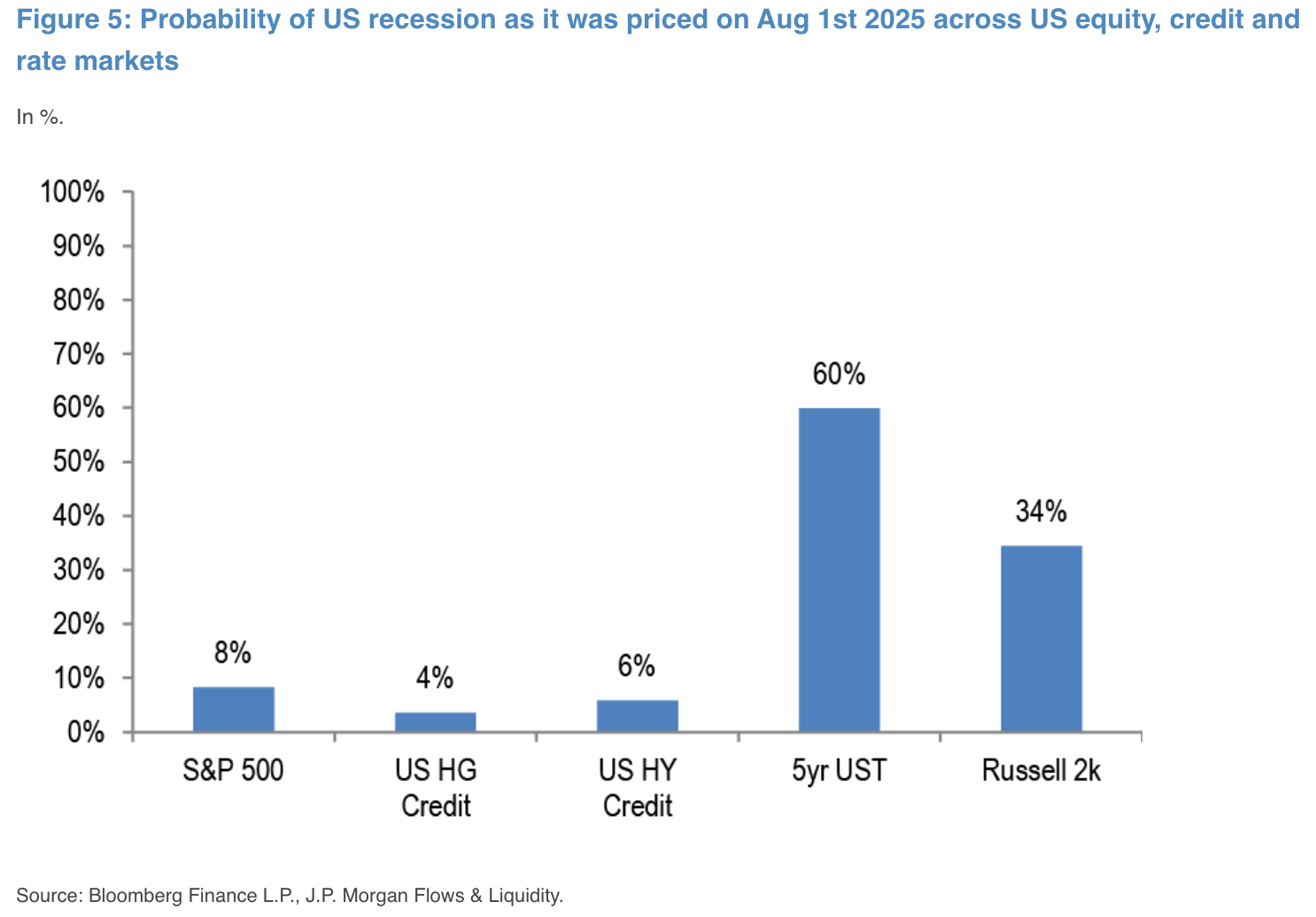

The current rally has taken recession odds back to low single digits across stocks & credit markets, with US fixed income being the (usual) outlier as they remain the most over-zealous in pricing in additional Fed easing.

Risk Assets Pricing in Next to No Chance of a US Recession on the Horizonrizon

Source: JPM

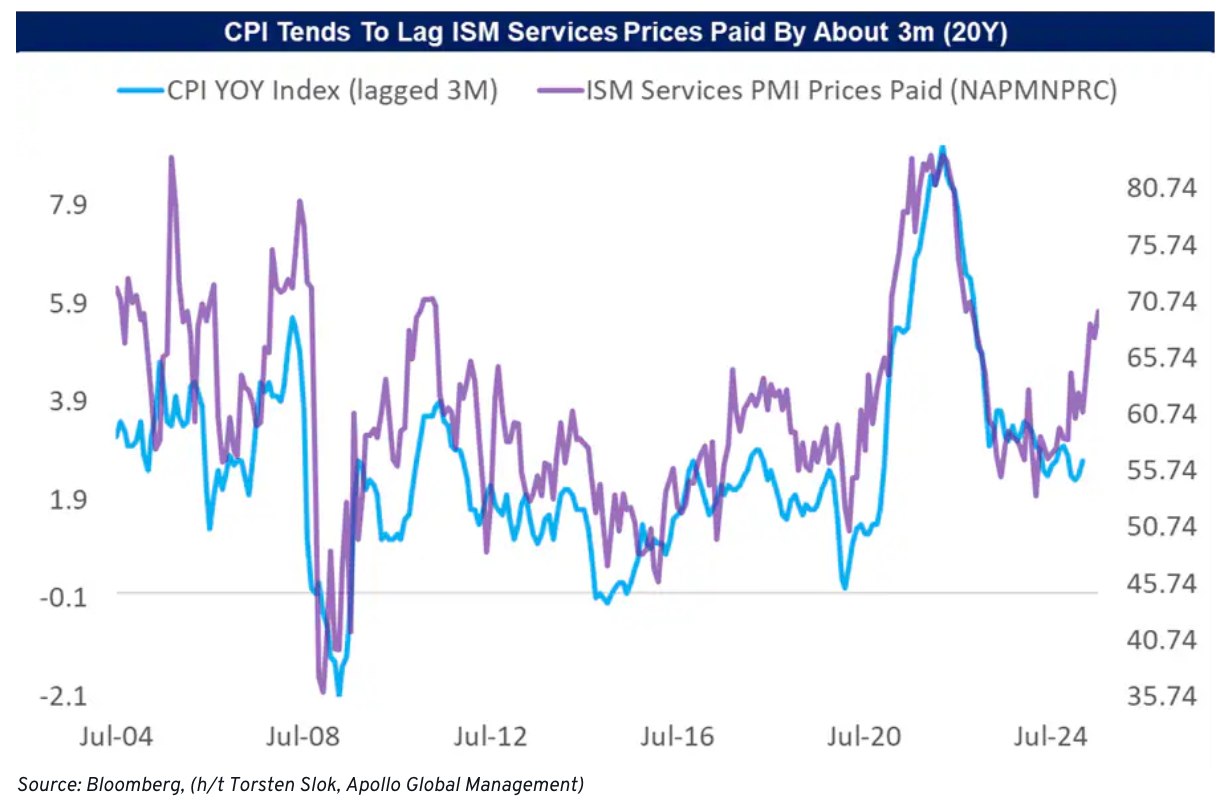

On the inflation side, while the Fed has stated that they are happy to overlook near term price pressures, ISM components are showing a concerning rebound in prices paid, which tends to lead CPI by about a quarter, potentially throwing a wrench into the Fed’s rate cutting plans later this year. But for now, markets are happy to levitate until hard data proves otherwise given the risk-on sentiment.

ISM Services Paid Shows a Concerning Rebound in Inflation Pressures in the 2H of the Year

Source: Citi

Crypto shared a similar rebound in prices this week, led by headline statements from Trump ordered regulators to “look into” the possibility of including crypto (and private equity) into 401k portfolios, which would obviously open up significant buying demand if that were to come to fruition. That’s still a long ways to go before that could possibly become law though.

Trump Ordered Regulators to “Look Into” Ways of Including Crypto & PE Into 401k Portfolios

Source: BBC

More exciting, Ethereum led the ramp higher this week with a +20% jump, with the latest mainstream experts / bandwagoners pumping ETH as the latest FOMO play in the public equity domain. Retail traders responded in kind, taking BNMR nearly 60% higher on the week, and showing native degens how to FOMO properly in the regulated world.

Ethereum Led the Crypto Rally This Week with a 20% Week-on-Week Jump

Source: Messari

Mainstream Cheerleading has Led the Rebound in ETH as the Latest Treasury Reserve Play

Source: Yahoo Finance, Trading View

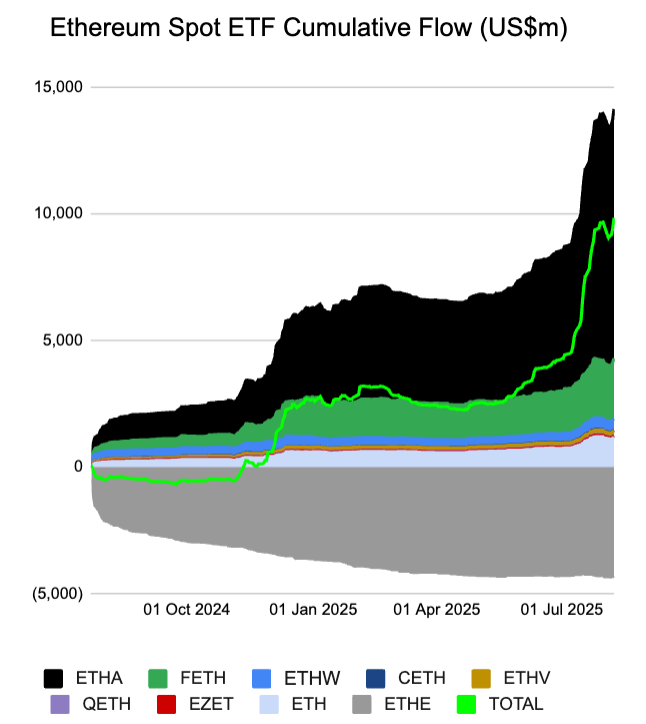

Unsurprisingly, Ethereum ETF inflows added ~$700M of fresh capital over the last 2 days of the week, taking cumulative inflows to new ATHs again, with cumulative AUM tripling 3x YTD to nearly $10Bln.

ETH ETFs have Tripled Their Cumulative Inflows YTD to $10B vs $3B to Start the Year

Source: Farside Investors

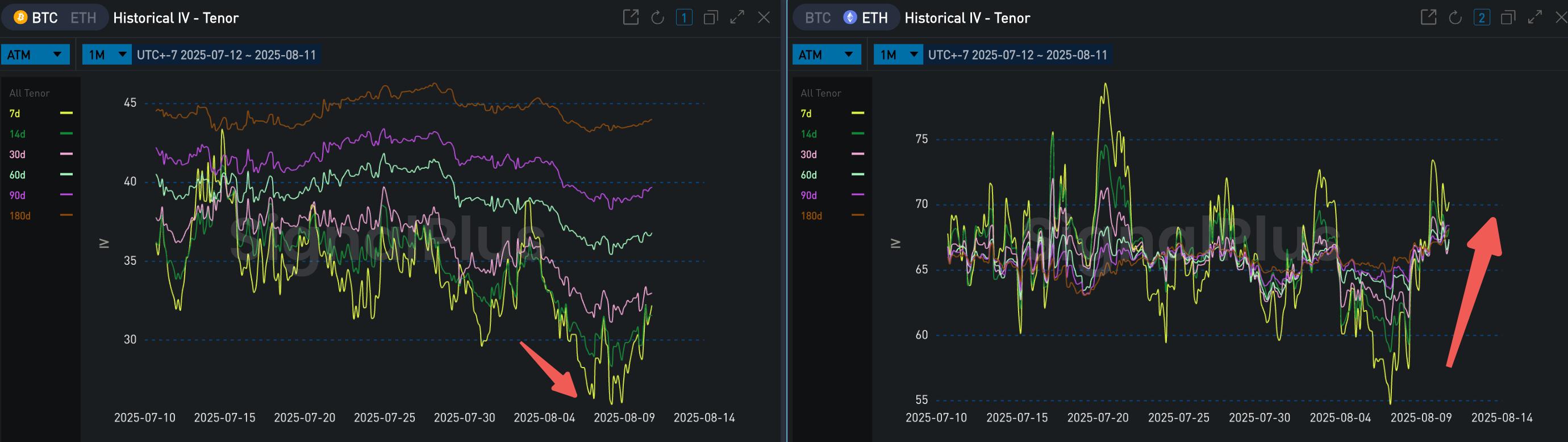

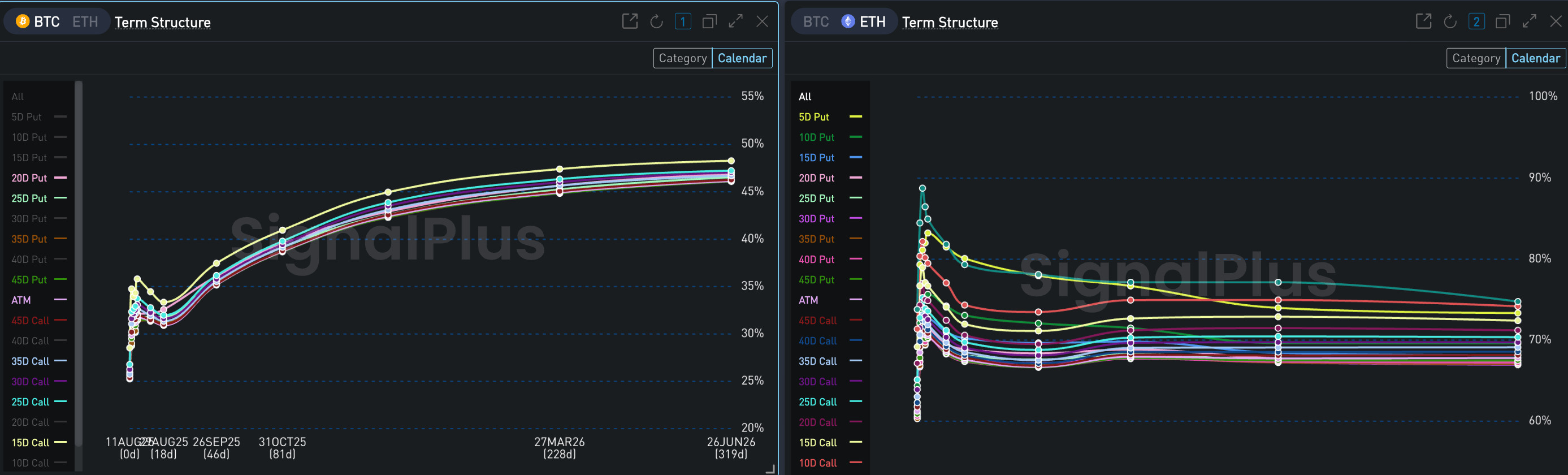

The recent rally in ETH has led to a dispersion in short-dated vol as well, with BTC IV still lingering around all time lows while ETH has jumped materially. Term structure on ETH is currently inverted as well with long-dated vol expected to settle back into the ~70% area, while the BTC IV curve is the opposite with short-dated vol heavily compressed with spot markets stuck at around the $120k area.

As a comparison, market pricing implied only a 5% chance of ETH hitting $4.5k in August just a month ago, with spot markets realizing way above the implied path and catching many participants off guard.

Short-Dated ETH Vol has Outperformed BTC Vol Subtantially on the Recent ETH Rally

Source: SignalPlus

The Vol Term Structure is Reversed as Well with the ETH IV Curve Inverted

Source: SignalPlus

Looking ahead, we don’t feel compelled to chase this market higher at the current juncture, given the expected 2-way volatility we expect across market assets over the next month or so. Keep an eye out for any large reversal in the DXY or an unwelcome return of inflation as potential downside catalysts. Stay safe and good luck trading everyone!

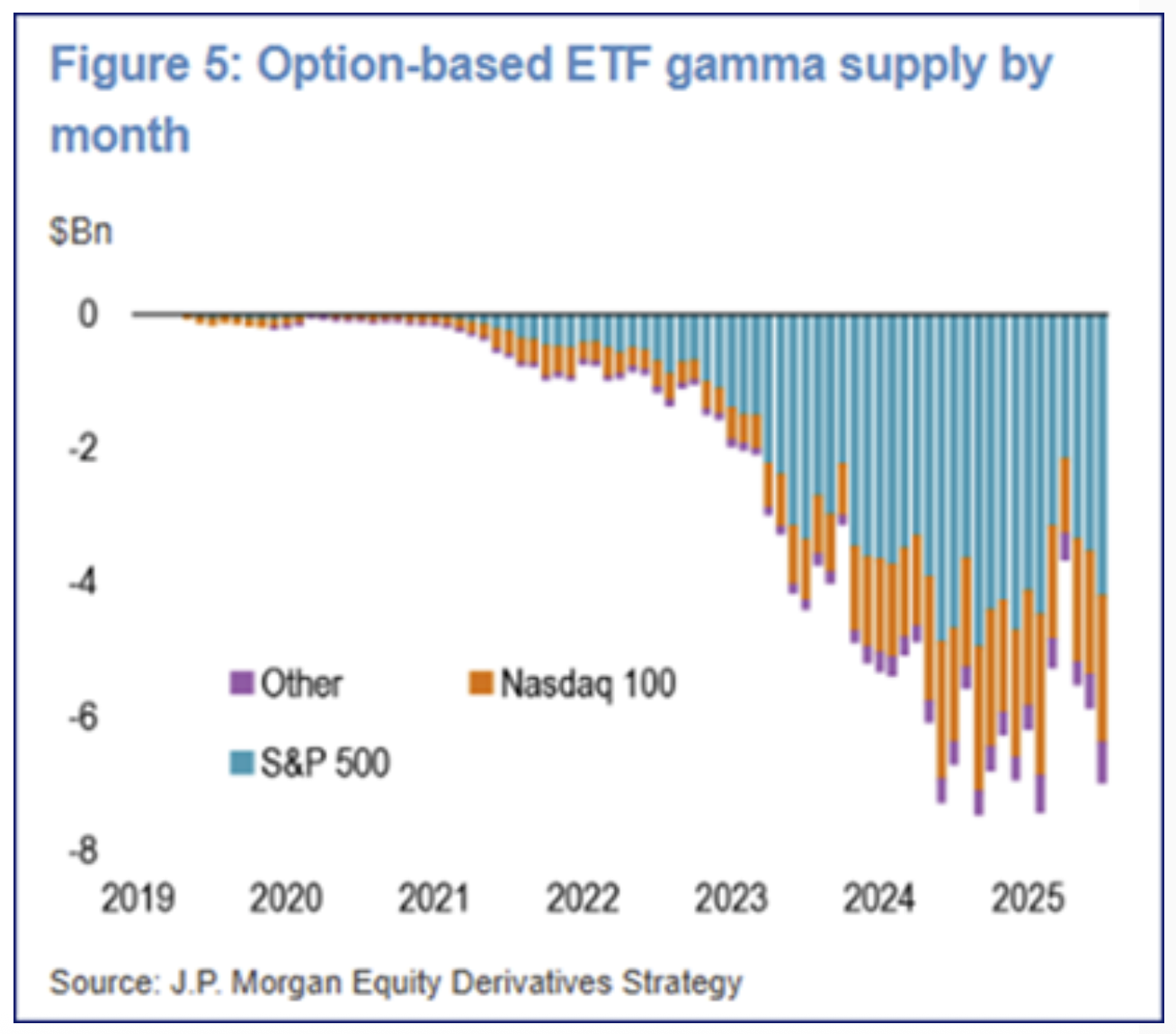

Should We Be Worried About a Volatility Spike in the Near Term Due to Overwriting of Option Premium

Source: Cam Hui