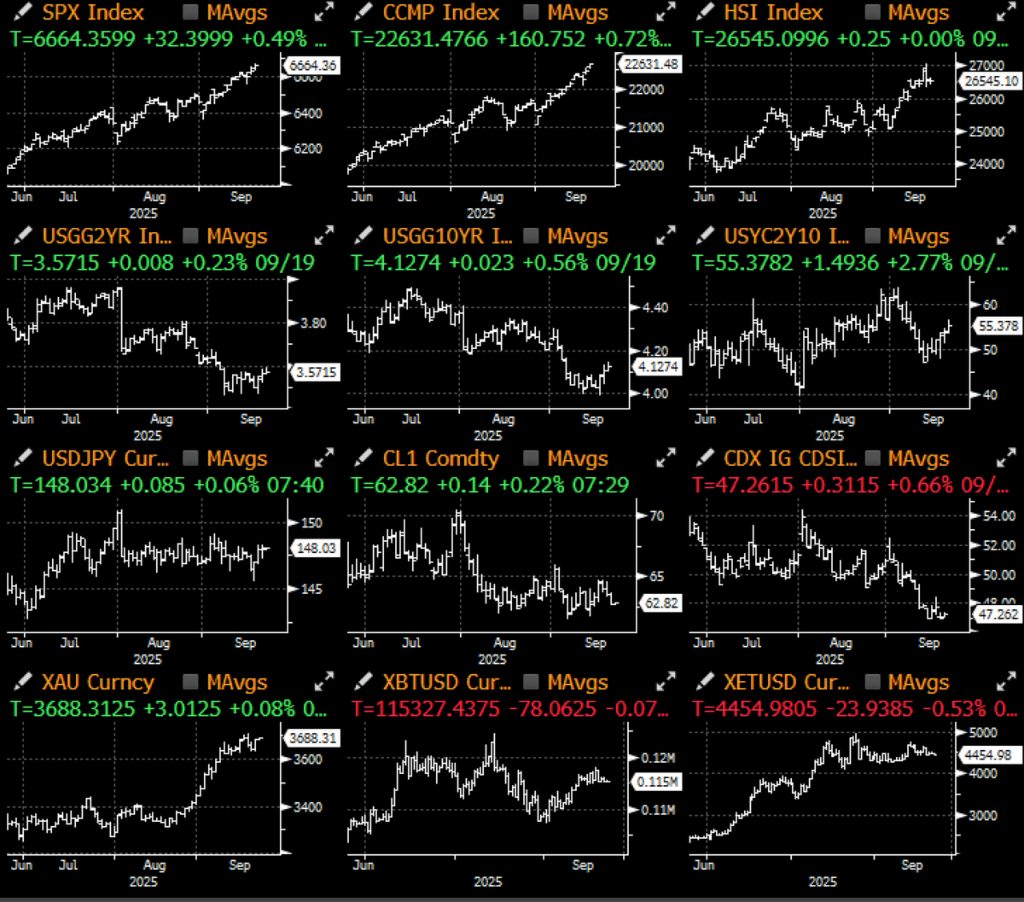

According to Bloomberg, for just the 26th time over the past 100 years, the S&P 500, Nasdaq, the Dow Jones Average, and the Russell 2000 all set new record highs over the same week as the melt-up sentiment continued unabated. At the same time, investment-grade credit spreads hit record tights since 1998, with the index coming in at a mere 0.72% over equivalent treasuries, offering next to zero protection buffer if the economy were to really worsen.

What Recession Fears? US Equities Hit Record Highs Over the Past Week as Credit Spreads Strengthened to the Tighest Levels Since 1998

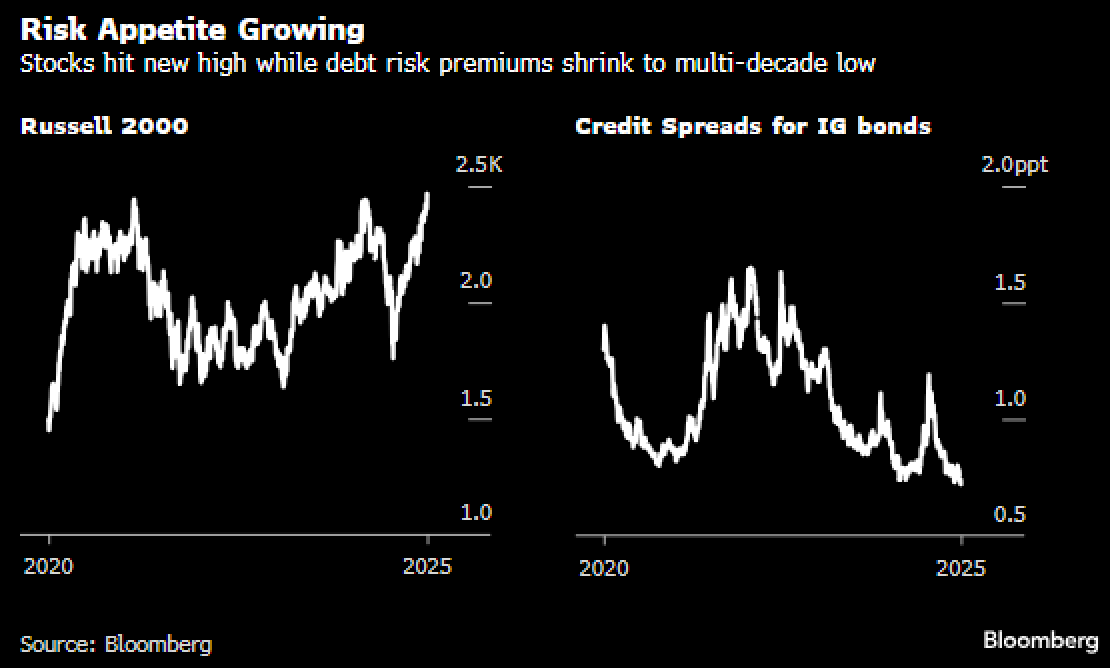

On the geopolitical side, there has been a notable improvement in the US-China narrative with a tetative TikTok deal, with the Trump-Xi phone call affirming continued progress being made on trade talks. The leaders have also promised an in-person meeting during the APEC Summit in South Korea next month, which would be their first face-to-face meeting since the G20 back in 2019. All of this has buoyed risk sentiment, particularly in EM stocks, with the BoJ even signalling plans to (slowly) divest out of their ETF holdings with the TOPIX hitting record highs.

China-US Relationships Appear to be On the Upswing in Recent Weeks

Source: Politico

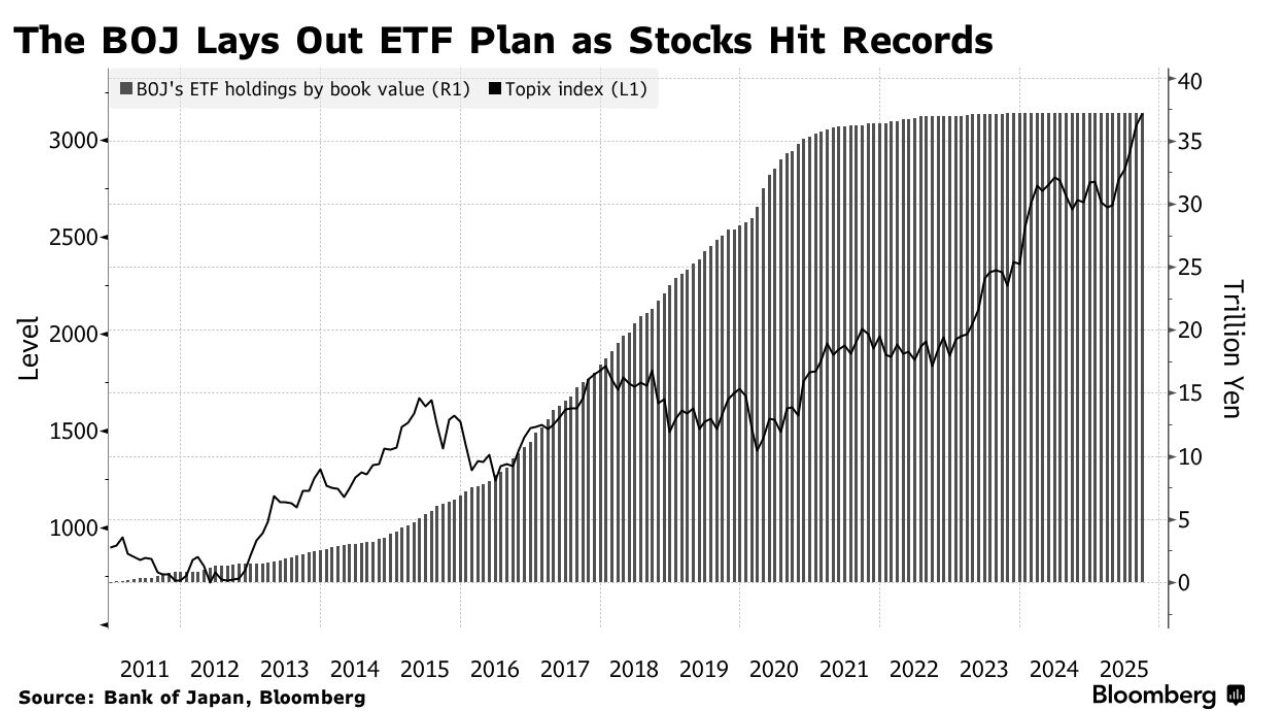

Equity Sentiment has Been So Strong that Even the BoJ is Looking to Divest Out of Their Considerable ETF Holdings

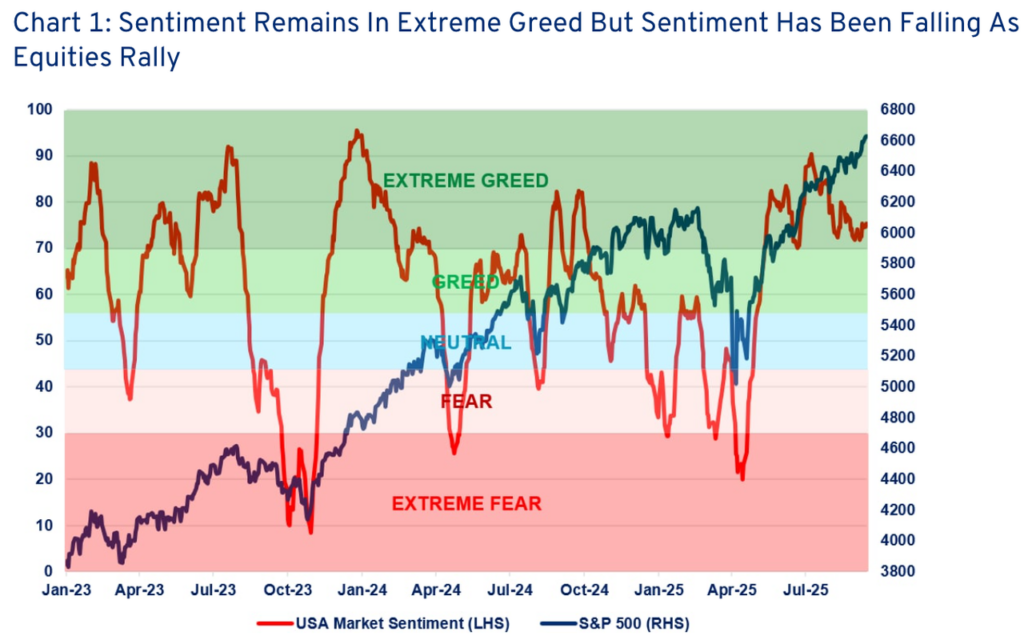

Risk sentiment barometers remain in extreme territory, but have eased off a bit since late summer, albeit without impacting equity prices much. Risk appetite remains driven by loose-money conditions, which remain at some of the easiest levels in history, thanks in large to the Fed’s recent dovish policy pivot.

Equity Sentiment Measures Remain Extreme but Have Come Off in Recent Weeks

Source: Citi

Financial Conditions are at Some of the Easiest Levels in Modern History

Source: Bloomberg

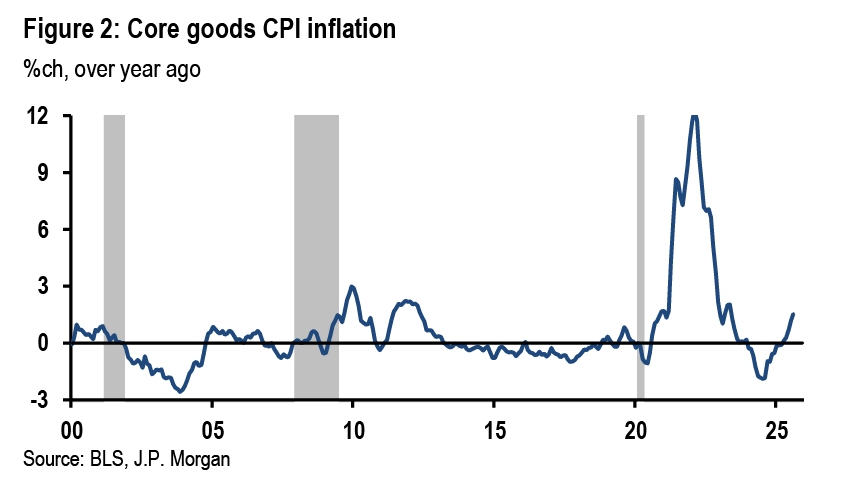

This week will be quieter on the data side, with focus shifting to the Fed speakers, with 17 speaking events planned for the week, headlined by Powell on Tuesday. Recently appointed Fed Governor Miran came out swinging, doubling down on his dovish dissent by claiming that he doesn’t “see any material inflation from tariffs… with no discernible core good inflation in US vs elsewhere… and that the Fed Rate is quite far from neutral”…

The Fed Continues to Turn a Blind Eye to Inflation… And Driving Asset Prices Higher as a Result

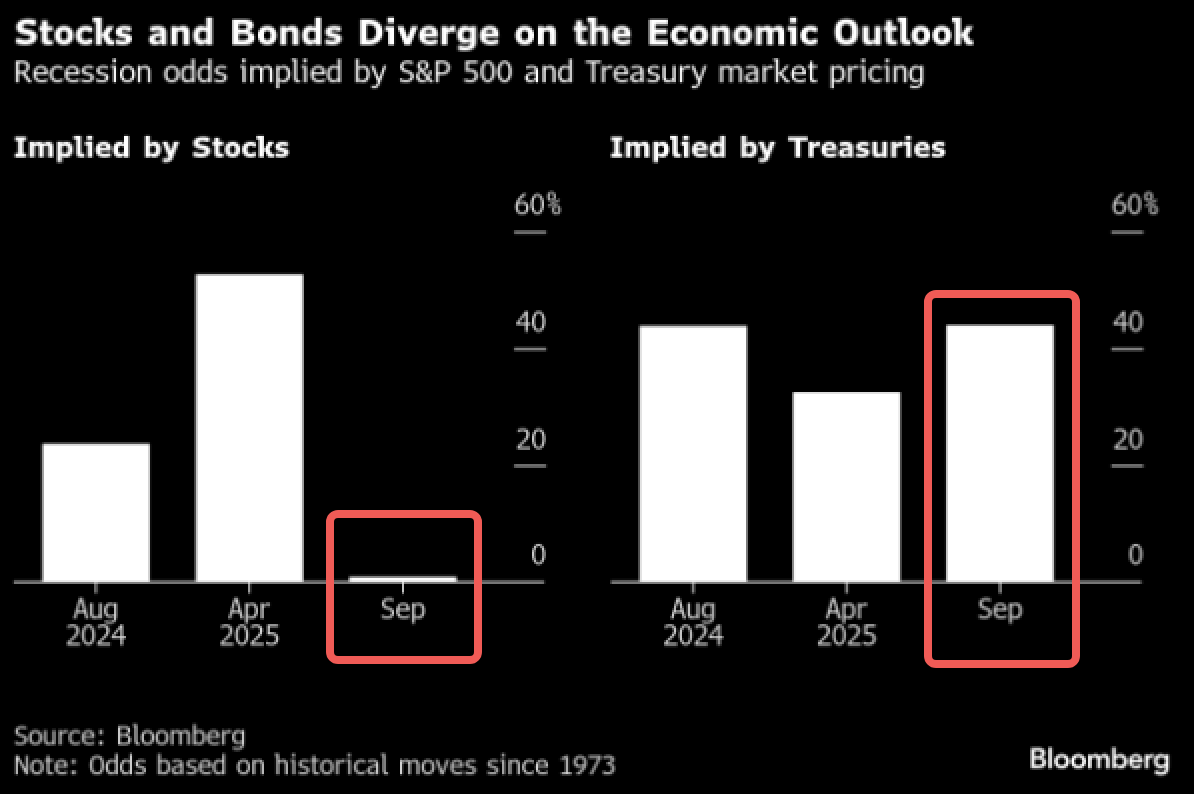

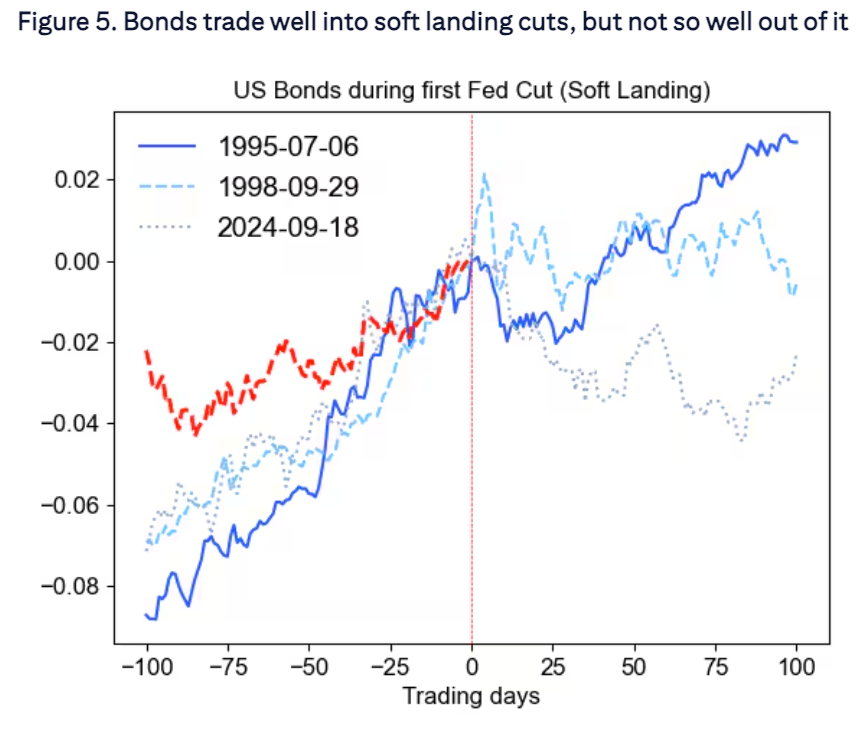

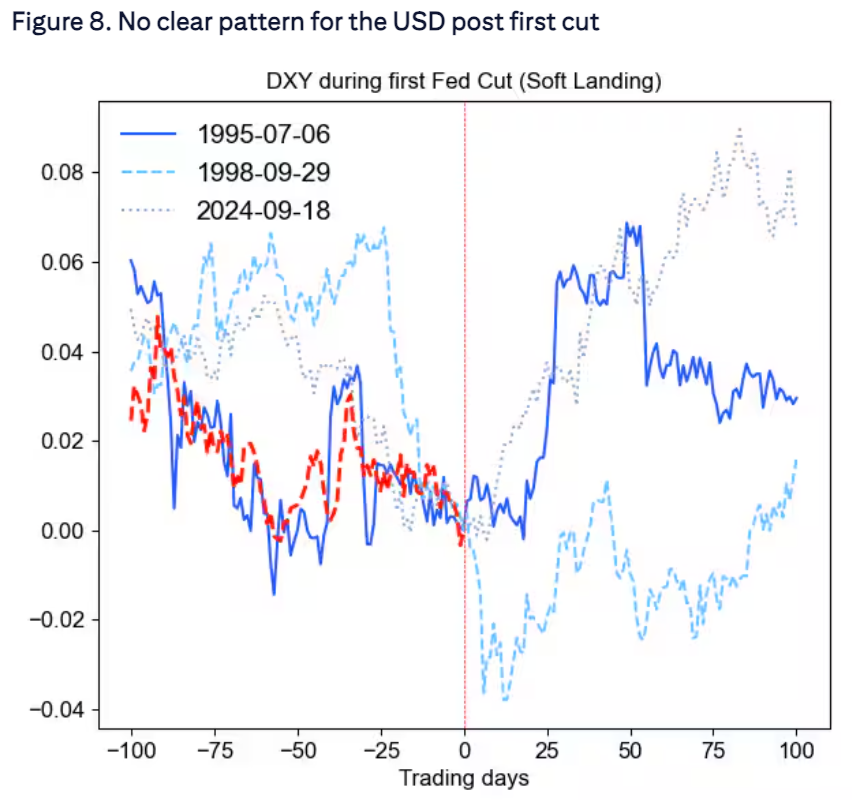

While it’s not the first time that stocks & bonds have told a different story – with equity pricing implying next to zero chance of a recession, while fixed income is pricing close to 50% – it’s helpful to revisit how they have respectively traded into and out of a Fed easing cycle.

A Tale of Two Markets… Again

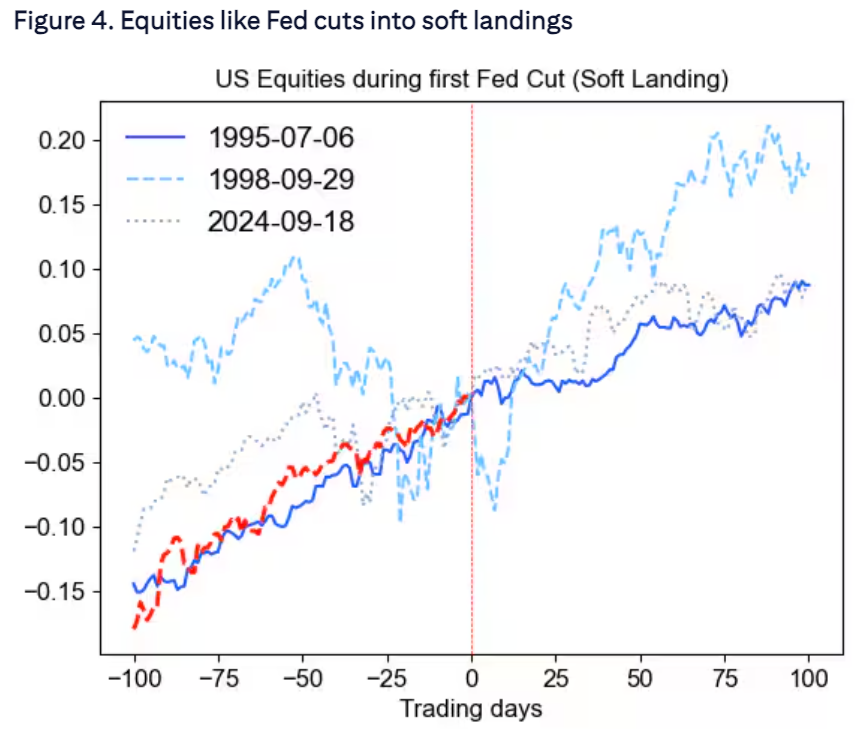

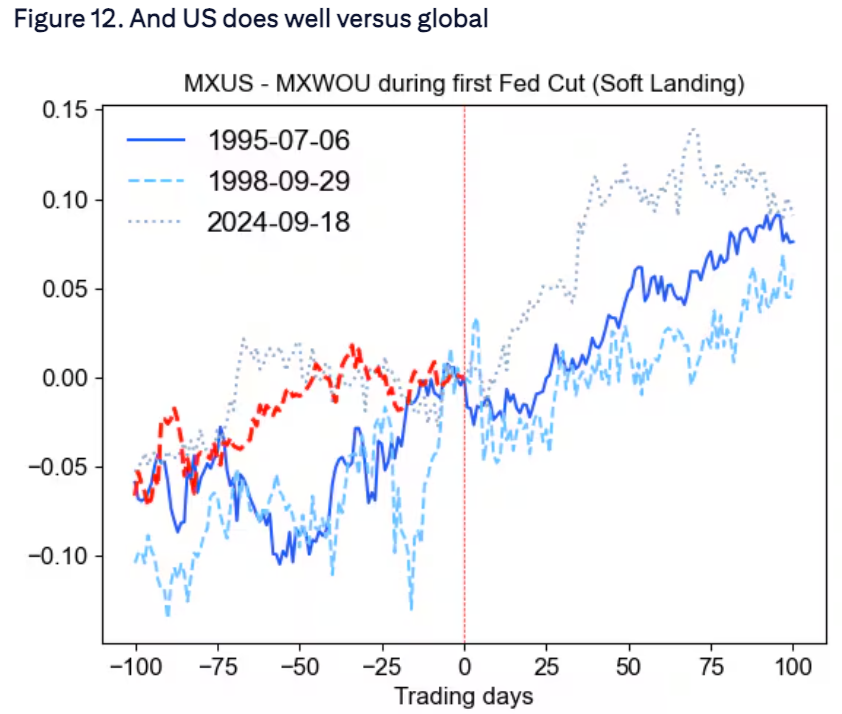

Assuming the Fed is successful in generating a soft-landing, US stocks have generally done well into AND out of the first rate cut, while outperforming global stocks at the same time. On the other hand, bonds have experienced quite the opposite, with performance being front-loaded and yields tending to re-drift higher as the economy stabilizes. For the US dollar, there doesn’t appear to be a clear pattern, as FX movements are more susceptible to the confounding influence of both capital and current account flows, though it’s probably fair to say that the Trump administration is more explicit about wanting a weaker dollar this time around.

Equities Tend to Do Well Into AND Out of Fed Cuts Assuming We Get a Soft Landing…

But the Same Can’t Always be Said About Bonds and FX Based on History

Source: Citi

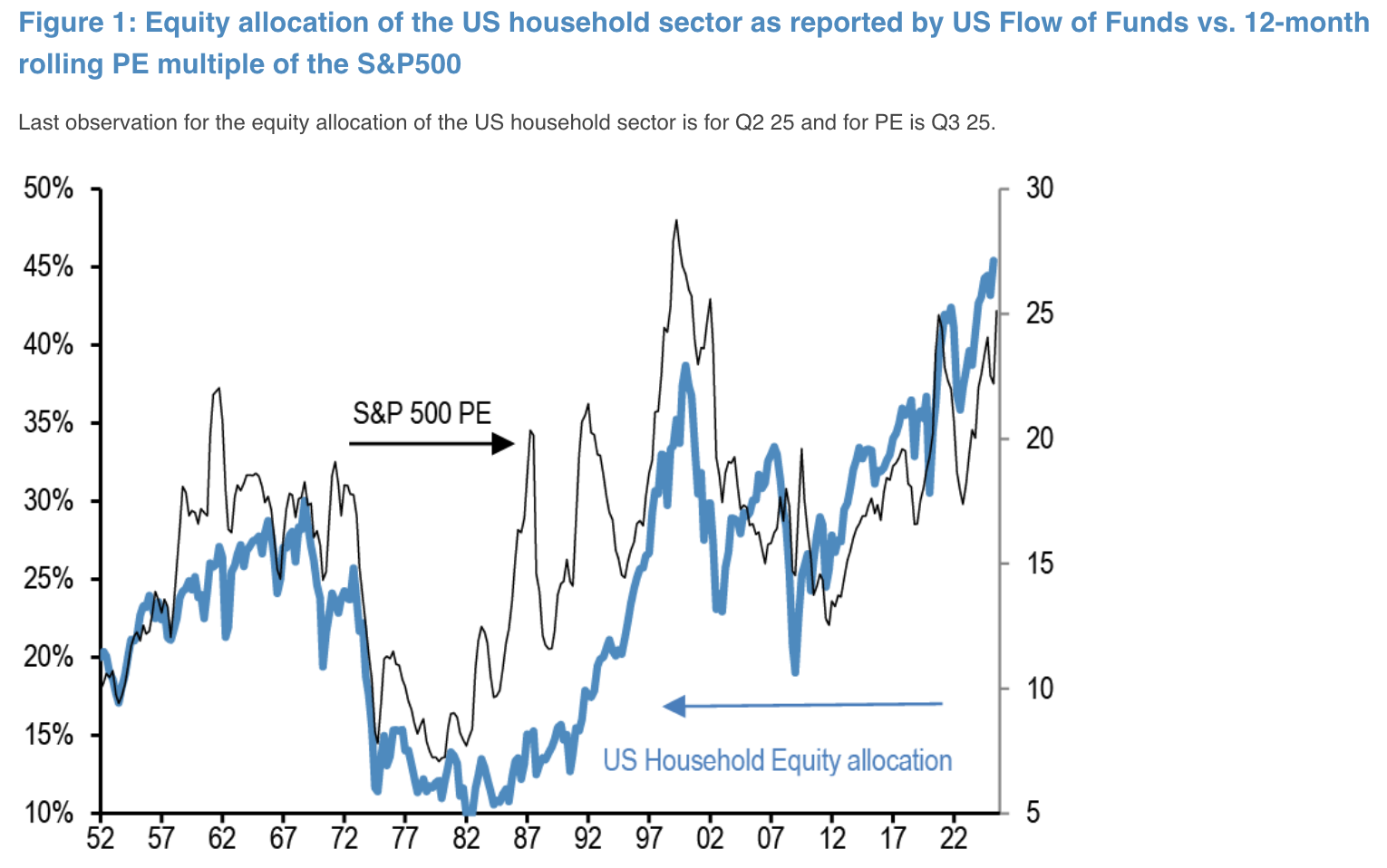

Not a lot to look forward to this week, with macro assets successfully bucking the negative Sep/Oct seasonals thus far, and US household allocation to equity closing in on an incredible 50% as the financialization of the US economy continues. Volatility remains low and hedges remain cheap, with no obvious catalysts suggesting otherwise in the meantime.

Risk Assets have Outperformed Negative Seasonals in Sep/Oct Thus Far, With US Household Allocation to Equity Approaching 50%

Source: Citi / JPM

Crypto prices had a flattish week, with nearly all major tokens in the red last week, with the notable exception of Binance’s BNB, which hit a new record high with a handful of successful token launches (eg. $ASTER). On the other hand, the Dogecoin ETF (DOJE) was successfully launched last Thursday, opening the door to a likely flood of memecoin-themed ETFs to be listed in the months’ head.

BNB was the Only Token to Rally Last Week, and Dogecoin’s ETF Launch Came and Went Without Much Fanfare

Source: Messari, FT

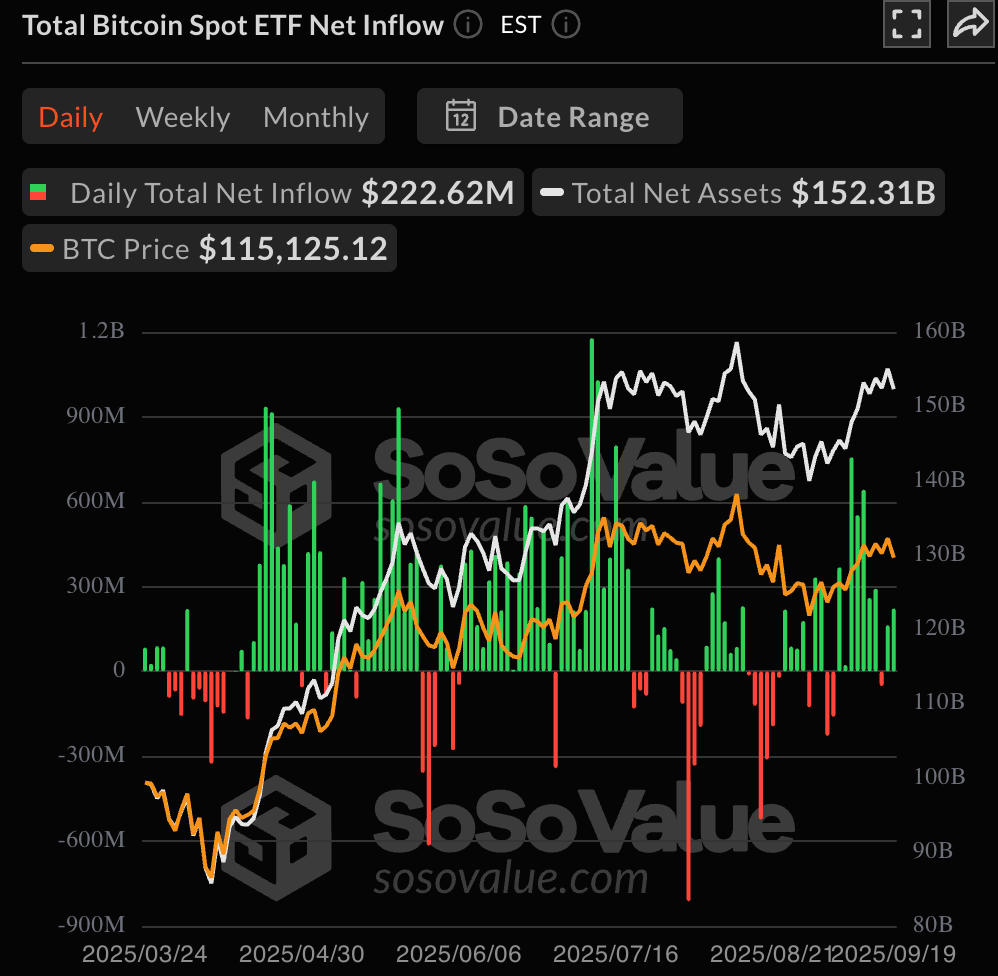

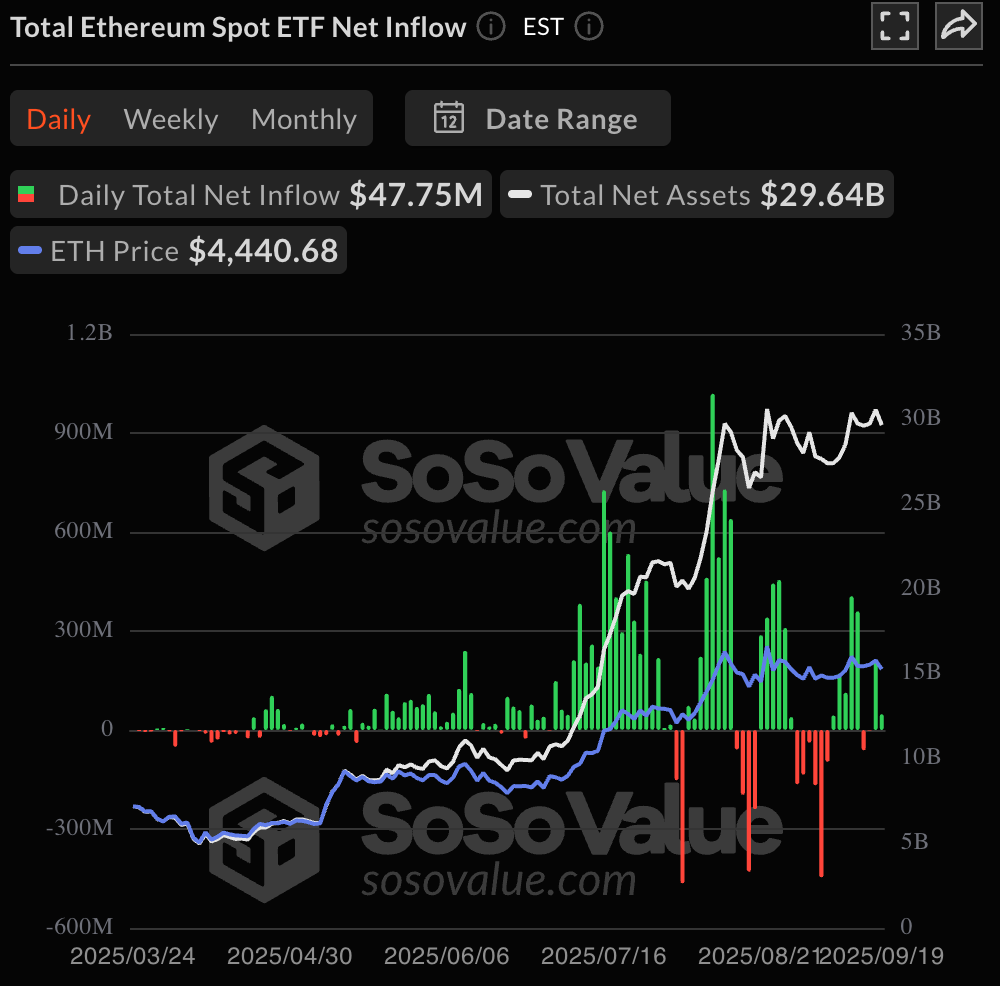

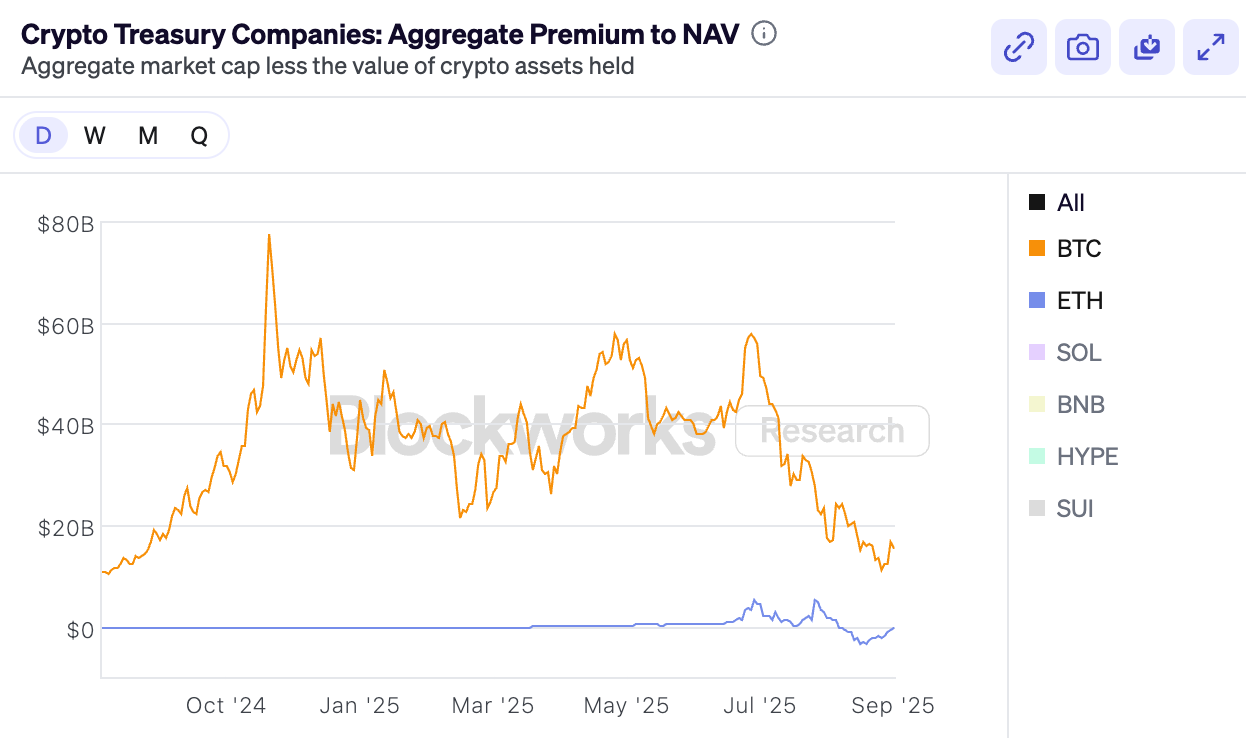

BTC/ETH ETFs saw modest inflows, but it was otherwise another uneventful week with both outright volatility and momentum trading extremely heavy. DAT premium rebounded slightly but lingers at near the lowest levels in a year. We expect markets to stay range bound in the foreseeable future, but would expect crypto to lag any further rallies in gold and equities in the meantime. Good luck & good trading.

BTC/ETH ETF Saw Modest Inflows Last Week

Source: SoSoValue

Implied Volatility & Momentum Remain in the Doldrums

Source: SignalPlus

Crypto DAT Premium Remain Noticeably Soft as Well and Suggest Further Weakness Ahead…

Source: Blockworks