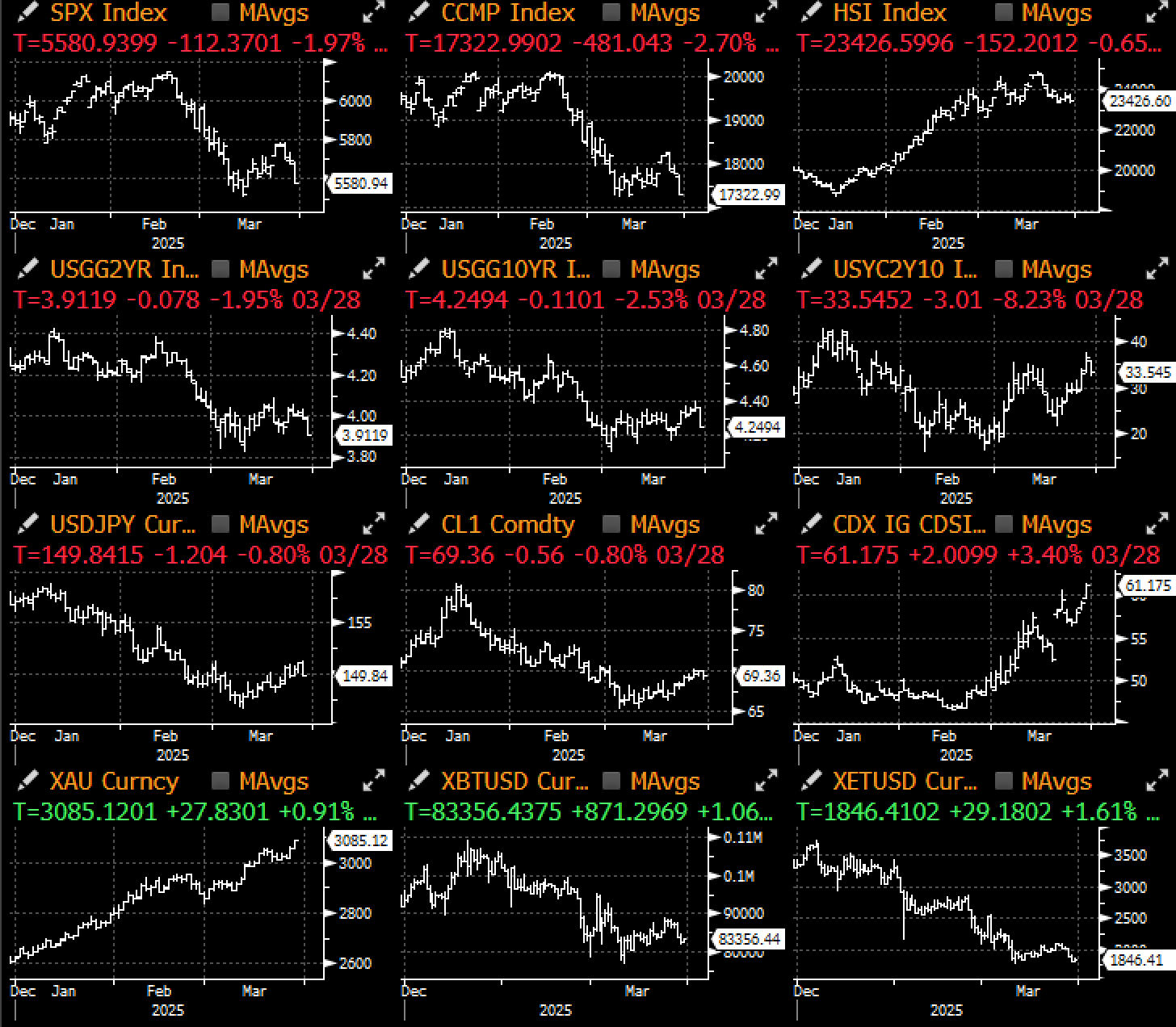

Risk assets endured a terrible end to a rough week with US equities trading down -2 to -3% on terrible breadth, CDS spreads hitting recent wides (+20bp on high yield), crypto prices breaking back to YTD lows (BTC <$82k), treasuries bull steepened, and spot gold hitting record highs as the primary risk-off hedge. Tech stocks were hammered (Mag-7 down -3.5% on Friday) while defensive names outperformed, as risk-takers took shelter ahead of Trump’s imminent ‘liberation day’ announcements this Wednesday.

On top of tariff concerns, US economic data disappointed across the board with sticky inflation prints against weak consumer confidence surveys.

Consumer spending slowed materially to start the year, rising just 0.1% MoM in real terms following a rough -0.6% drop in January. Services spending fell for the 1st time since 2021, while core PCE came on the high side at 0.37% MoM and 2.8% YoY, giving the Fed room very little room to maneuver. Final UMich long-term inflation median came in at the highest level in a decade (4.1%), with the 5yr expectation also rising from 3.3% to 3.7% at the latest print.

Bad Data Day Friday – Weak Spending, Low Consumer Confidence, and Sticky Inflation Cast a Gloomy Mood to End the Week

Source: Bloomberg, Citi

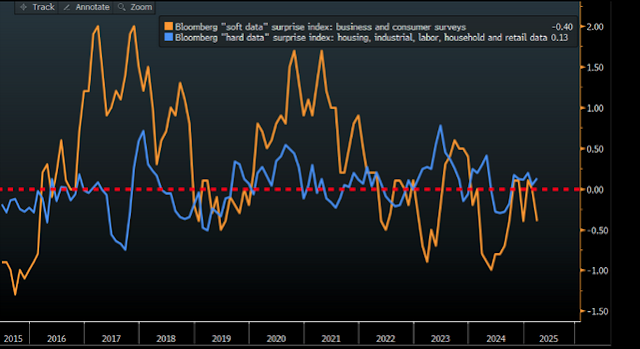

While economic hard data has held in for the most part, participants are rightfully worried about the weakening survey data spilling over into an activity slowdown. This is especially true at a time when Elon’s DOGE department is making such drastic cuts to government faculties, with a Washington Post article suggesting that the latest DOGE initiatives will be cutting up to 50% of federal agency employees based on an internal White House document.

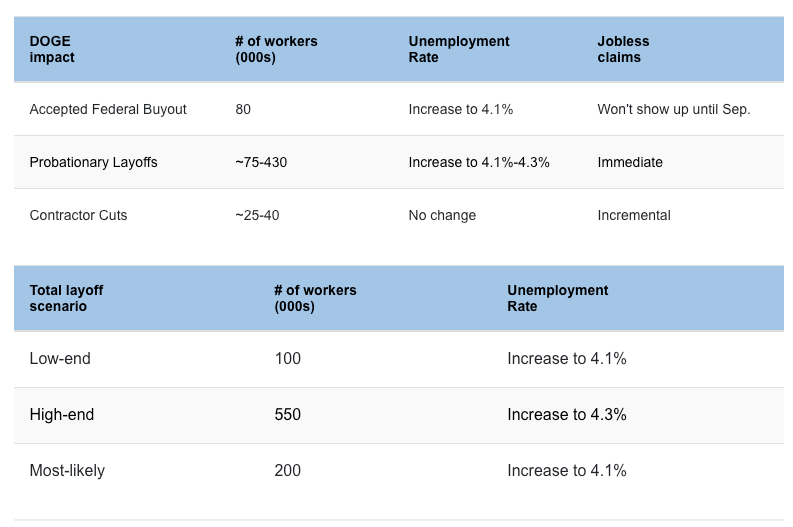

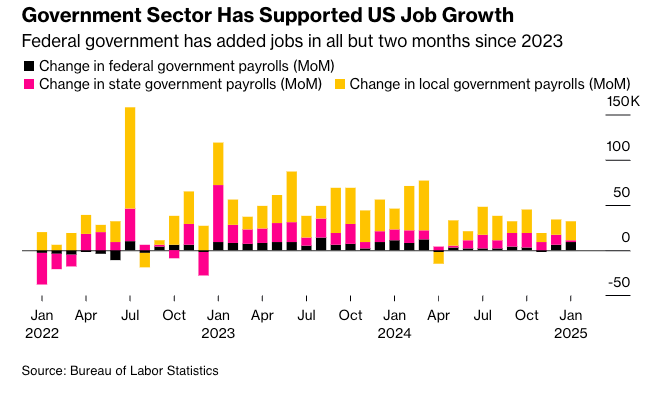

Such a cut would basically offset much of the US job gains post covid, which was mostly government sector driven, and puts significant upside risks on the unemployment rate vs current sell-side estimates.

Economic Soft Data Remains a Clear Downward Trend… Will Hard Data Follow Soon?

Source: Bloomberg

The DOGE Cuts are Getting Serious and Adding to Upside Risks on Unemployment

Federal officials are preparing for agencies to cut between 8 and 50 percent of their employees in the first phase of a Trump administration push to shrink the federal government, according to an internal White House document.

Source: Washington Post

Source: RBC, Bloomberg

As if that wasn’t enough, the latest update to Atlanta Fed’s GDPNow suggested a negative growth in Q1 even after adjusting for the outsized gold import figures. The latest adjusted print showed 1Q25 GDP growth at -0.5% vs +0.2% previously, well below the 1.2% consensus GDP estimate from Wall Street, which stood as high as 2.2% a short while ago.

Stagflation, anyone? Atlanta Fed’s GDPNow Suggests a Negative Print for Q1 GDP

Source: Atlanta Fed

In terms of market response, treasury yields aggressively bull-steepened into the risk-off move, providing a bit of a PNL buffer for equities, as stock-bond correlation fell to the most negative levels in a year. A negative correlation at this time suggests that markets are genuinely worried about an economic slowdown that the Fed might not be able to buffer with rate cuts in time.

Bonds-Stock Correlation is at the Most Negative Levels in a Year as Markets Worry About an Incoming Slowdown

US Treasury Yield Curves Bull Steepened Aggressively Post the Disappointing Economic Releases

SPX broke down through a bearish flag pattern, and the Mag-7 threatened to make a bearish breakdown against the YTD lows. Technical indicators look ominous and the path of least resistance appears to be downwards from here.

Both SPX and Mag-7 Stocks Appear to Be Breaking Down from Technical Support Levels

Source: Cam Hui, Bloomberg

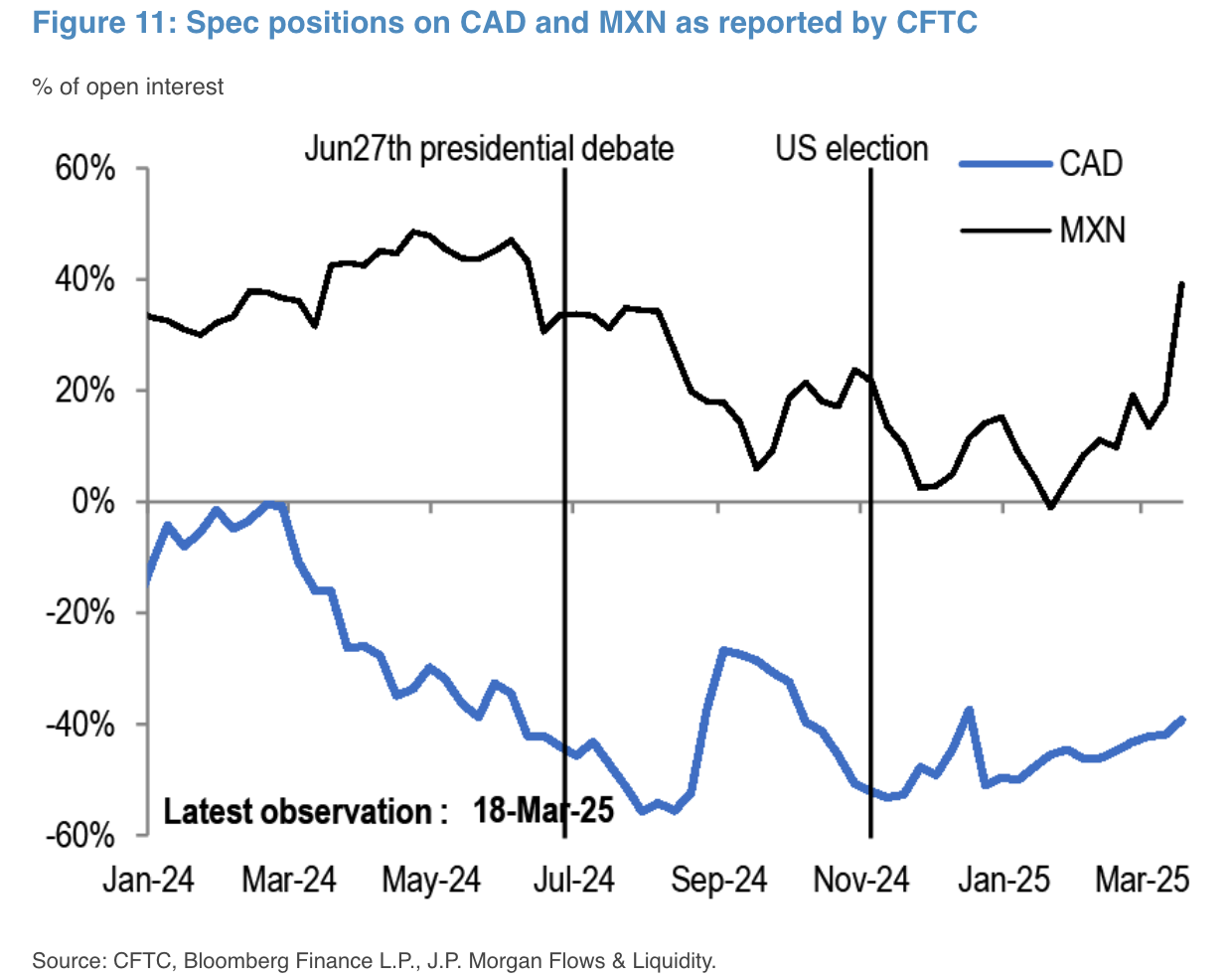

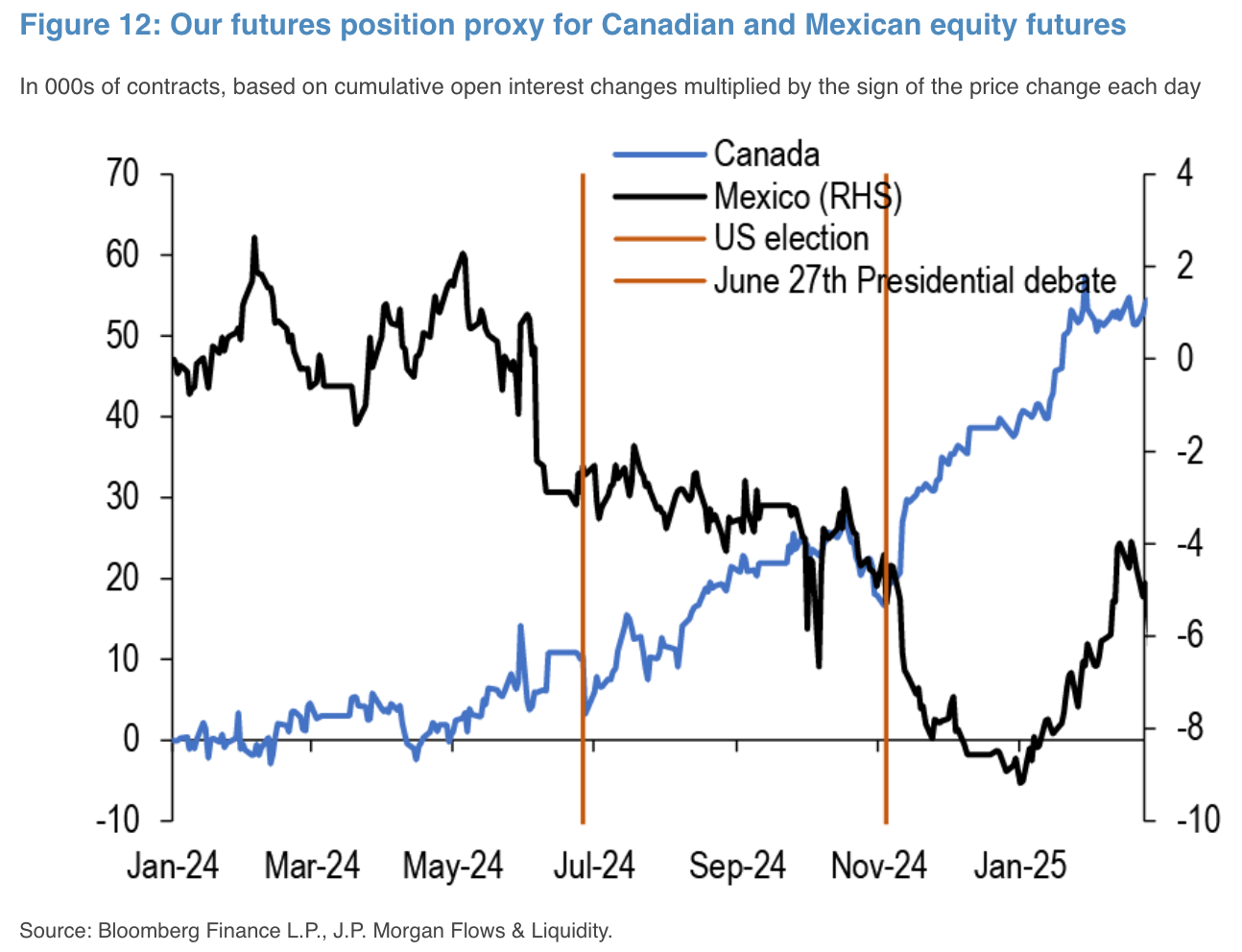

Naturally, risk takers are reeling from the PNL damage and have been taking a highly defensive stance with low exposure this week. FX option demand suggests low activity and positioning ahead of April 2nd, while outright exposures on tariff-sensitive assets in Canada and Mexico remain muted.

TradFi Speculators are Taking a Cautious and Non-Commital Stance Ahead of the April 2nd Announcement

Source: Bloomberg, Citi

Just as in months past, crypto’s close correlation with equities continued, with BTC trading down -6% on the week and ETH and SOL losing -13% and -10%, respectively, on a lack of new catalysts and inflows. ETF activity has been muted and more of a function of hedge fund basis-arb trades, rather than new directional flows.

Crypto Saw Another Tough Week, Mirroring the Move in TradFi Assets

Source: Messari

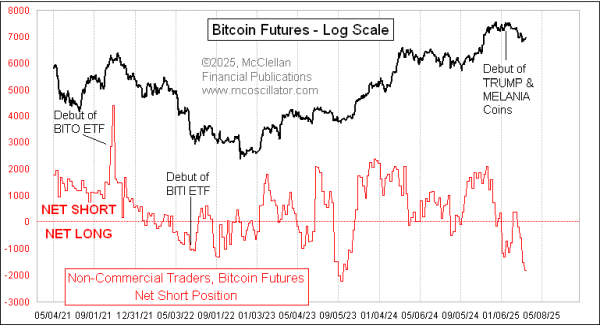

From a positioning perspective, speculative positions on BTC futures (CME) are at some of the most negative (short) levels over the past few years, a rapid turn around in fortune from the widespread bullishness in January. Keep in mind that positioning data is merely a statement on the market condition, and not necessarily a signal to a tradeable setup. The catalysts for a sustained rally remain fleeting at the moment, though we would expect any bullish turn to be sharp given the extended short positioning at the moment.

Speculative Shorts on BTC Futures (CME) is at the Highest Level in Years

Source: Tom McClellan

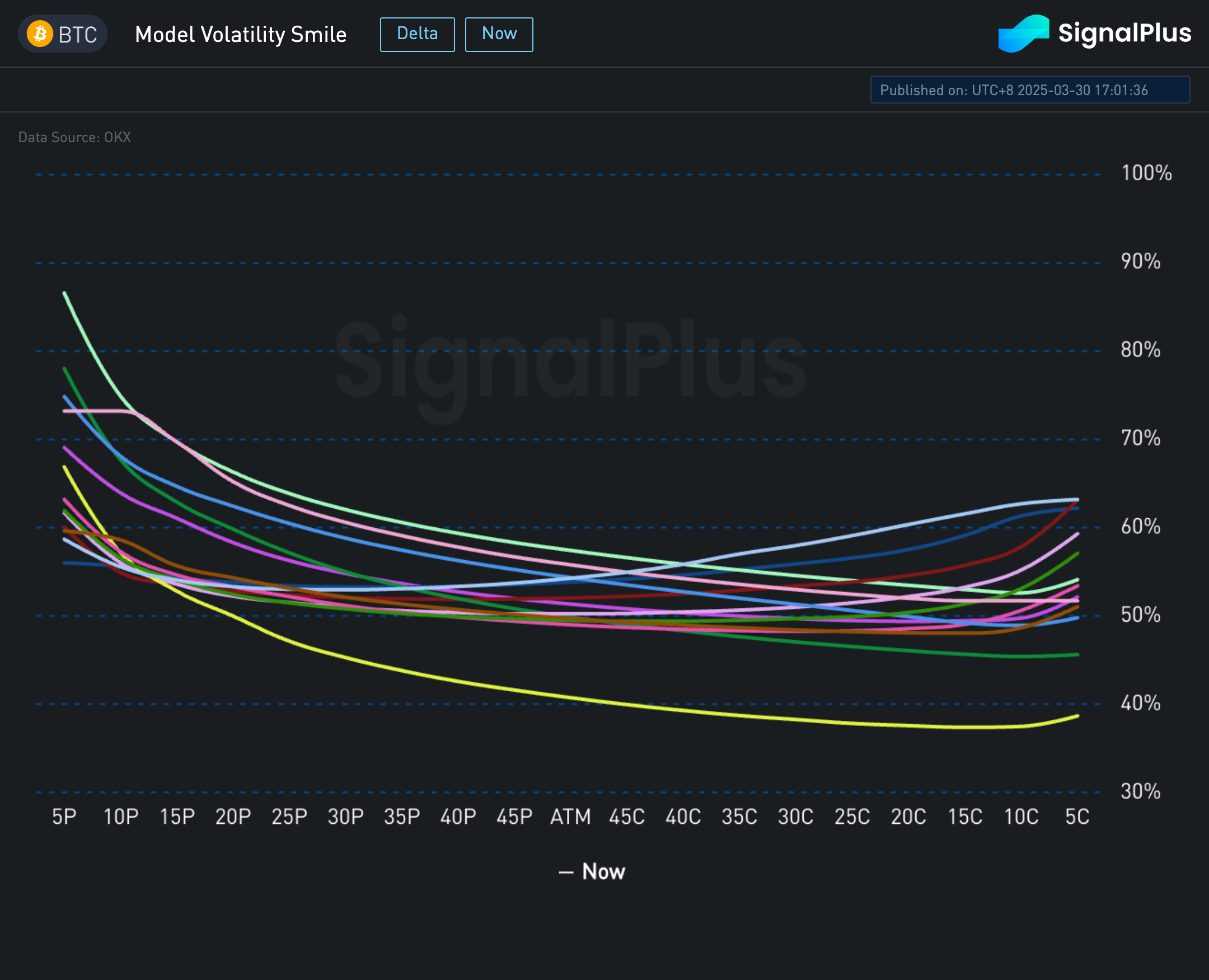

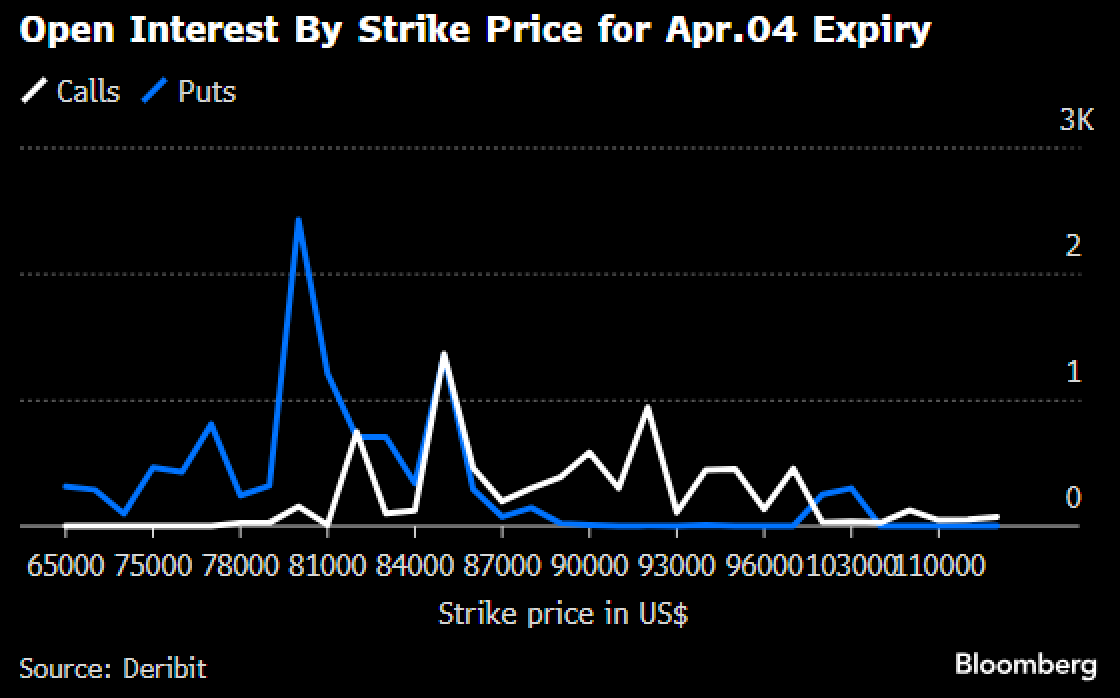

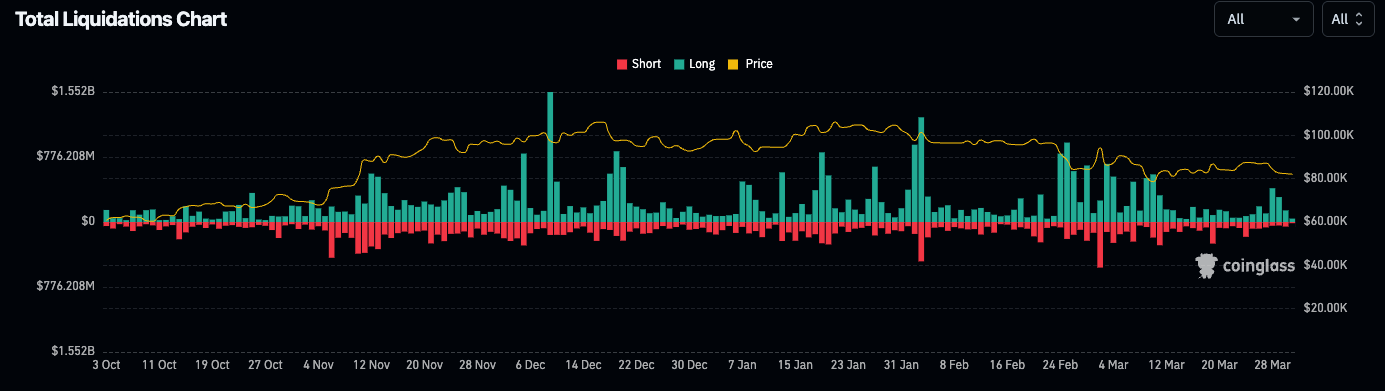

In options space, put skews are trading extremely rich to calls across all maturity tenors, with the market hedging aggressively against the downside, particularly around the 80k area. Futures liquidation has picked up recently, though nothing like the pace earlier in the quarter, signaling the current low conviction in the space to close a challenging quarter.

BTC Put Smiles are Very Rich Compared to Calls, with Particular Strike Interest at Around the 80k Area

Source: SignalPlus, Bloomberg

Long Futures Liquidation has Picked Up on the Latest Sell-off, Though a Far Cry from Earlier in the Quarter

Source: Coinglass