It Might Have Been a Quiet Week for Markets, But Always a Bull Market for Meme Creators…

Source: Dave Whamond

Earlier in the month, FT columnist Robert Armstrong coined what had been a little-known term called ‘TACO’, which stands for ‘Trump Always Chickens Out’, a rather cheeky dig at the President’s seeming propensity to back out of tough trade negotiations after an aggressive opening salvo. Effectively, Mr. Armstong suggested that it was in the counterparty’s interest to ‘wait out’ the President’s threats as he would eventually stand down.

The TACO acronym took on mainstream relevance when the President was asked about this term specifically during a WH press meeting, and it was naturally not well received by the leadership.

Perhaps in response to the insolence, the administration turned noticeably more hawkish towards the end of the week, headlined by a slew of negative US-China escalation headlines:

- Trump accused China of “total violating” their Geneva trade agreement

- Secretary Bessent accuses China that it is holding back products that are essential to the US industrial supply chain (rare earths)

- Trade Representative Greer accused China of ‘slow-rolling’ rare earth export approvals

- Beijing has countered by accusing the US of ‘absuing’ export controls in semiconductors

- The Administration broadened restrictions on licensing agreements on China’s tech sector

- The Commerce Department restricted the sale of chip design software and some jet engine parts to China

- Secretary of State Marco Rubio announced that the US would start revoking Chinese student visas, on top of the earlier ban on Harvard’s foreign students

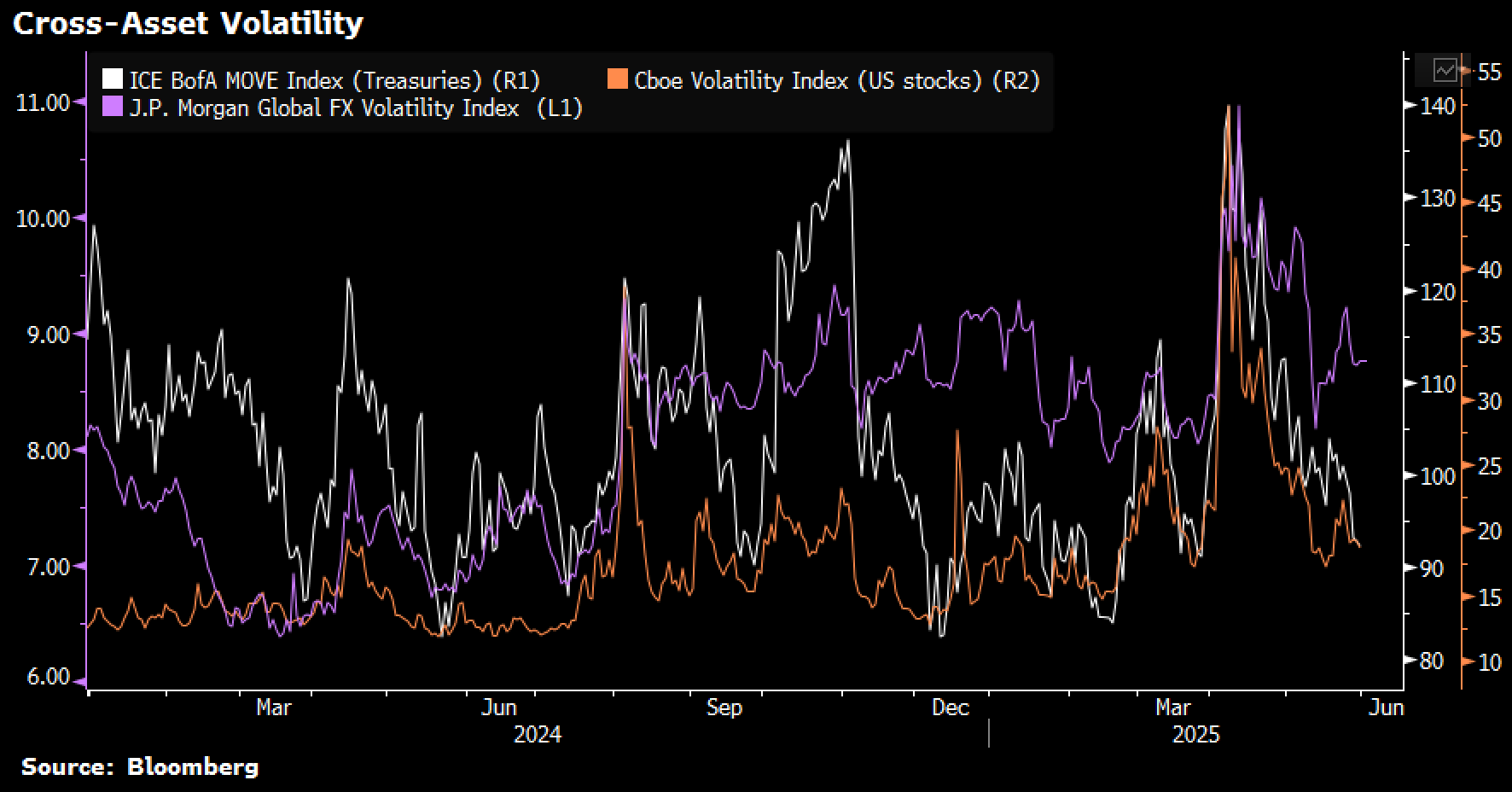

Overall, the market went into a more decidedly risk-off time late in the week, with equities struggling to make new highs despite equities and fixed income volatility receding back to cycle lows.

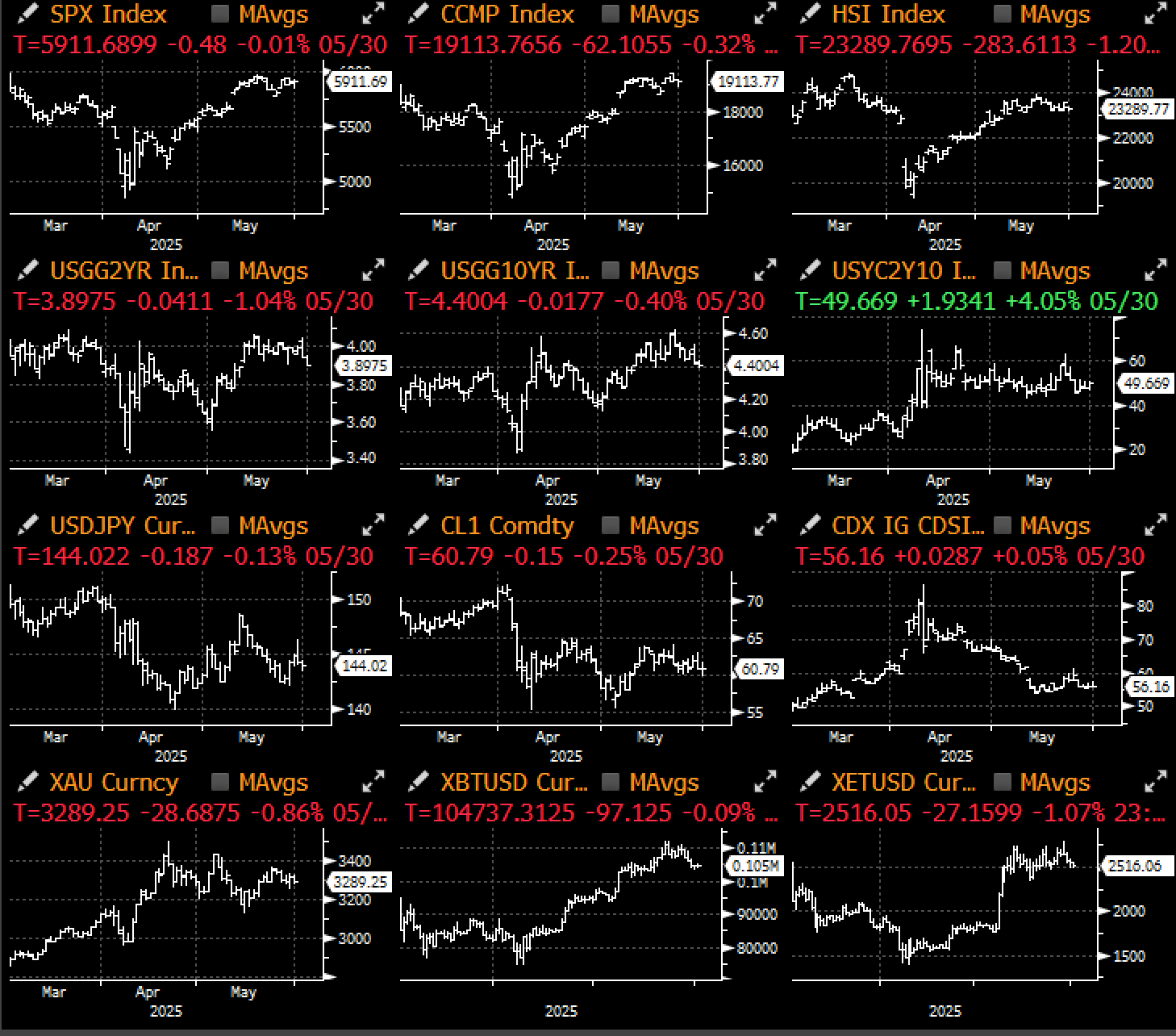

SPX Failing to Break to New Highs Despite Easing Tariff Tensions from Court Decisions

Source: Cam Hui

Equities & Fixed Income Volatility Have Receded Back to Interim Lows

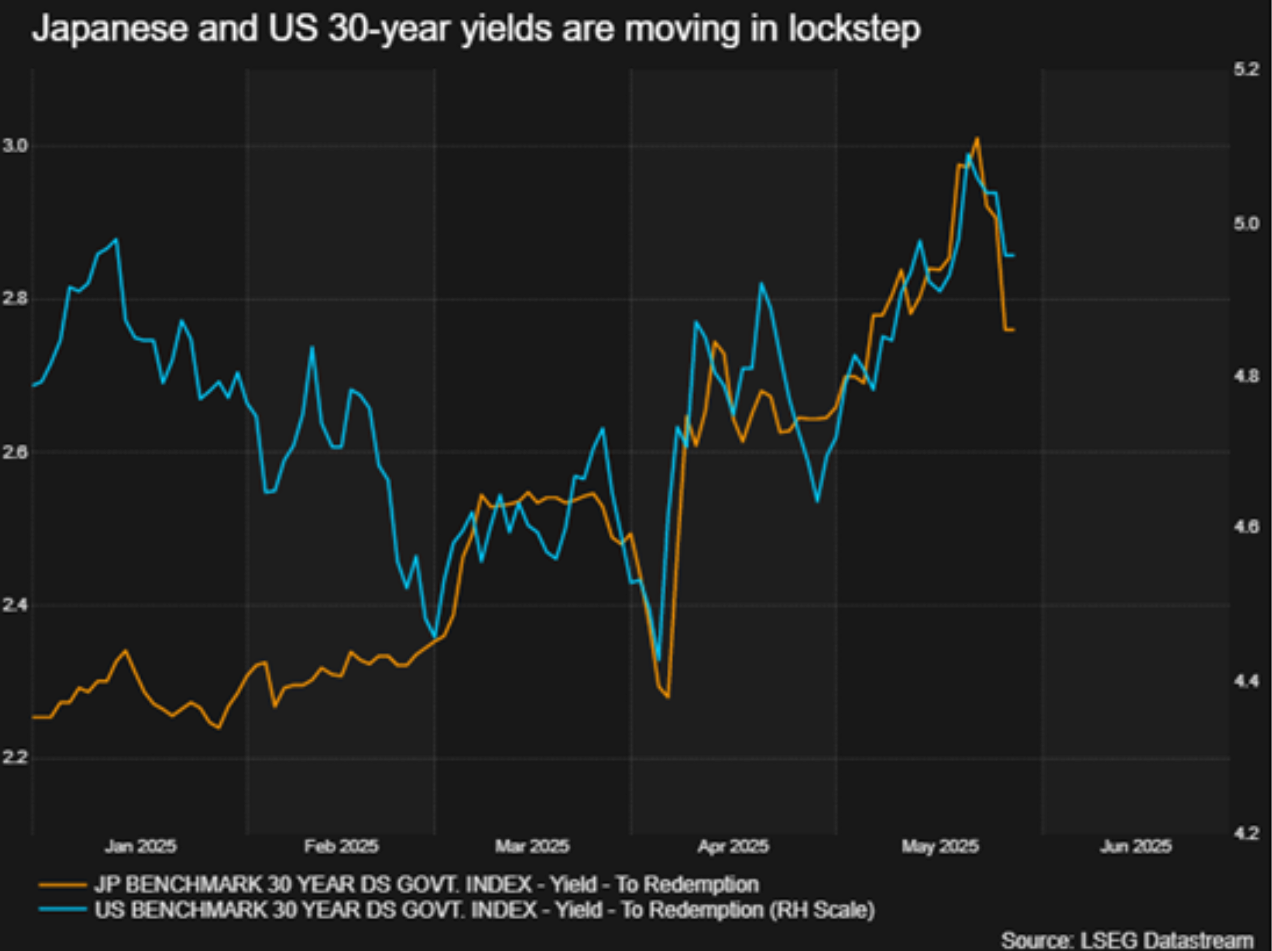

Earlier concerns over runaway bond yields have also calmed, with 30yr JGBs moving lower in lock-step with US treasuries, making it difficult to say which market is leading who. This actually suggests that the overall rise in yields is from general fixed income de-risking and overall macro concerns, rather than valid and idiosyncratic issues, adding comfort to our view that yields should be steadily grinding lower into the summer months.

UST and JGB Yields have Been Moving in Lock-Step from General De-Risking, But Showing Signs That the Worst Might be Behind Us

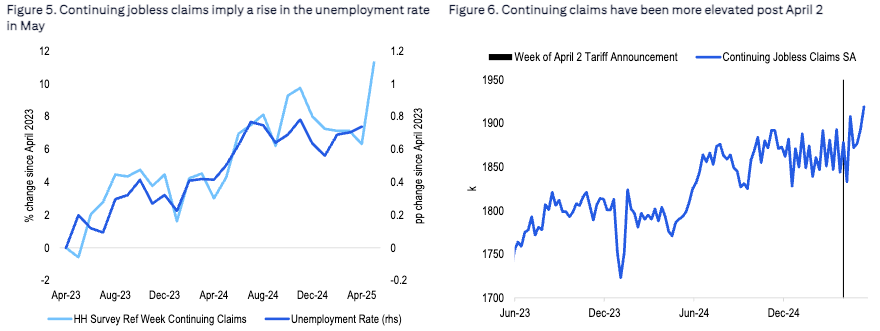

Outside of the daily trade-related headlines, which the market has started to normalize to, markets are feeling tired with convictions low across the board, with focus likely to be towards the end of the week to see whether the NFP can continue to buck the trend against softening survey data and lower growth expectations. Given the persistent softening in job surveys and jobless claims, the risk is probably skewed to the downside, in particular given where overall equity levels are. Famous last words!

NFP has Been Hanging in Strong Despite a Rapid Slowing in Survey Data & Growth Expectations

Source: Citi

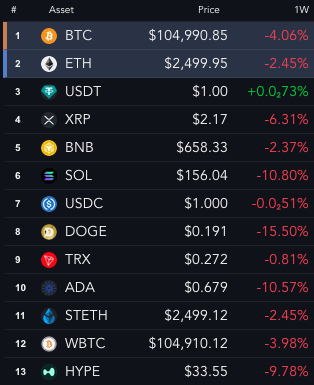

Over in crypto, while recent headlines have been positive, the price action has struggled as both BTC and MSTR have failed to break decisively to the upside, with major tokens falling around 5-10% on a weekly basis.

Crypto Prices Struggled Over the Past Week Despite Encouraging Headline Developments

Source: Messari, Mike Cautillo on X

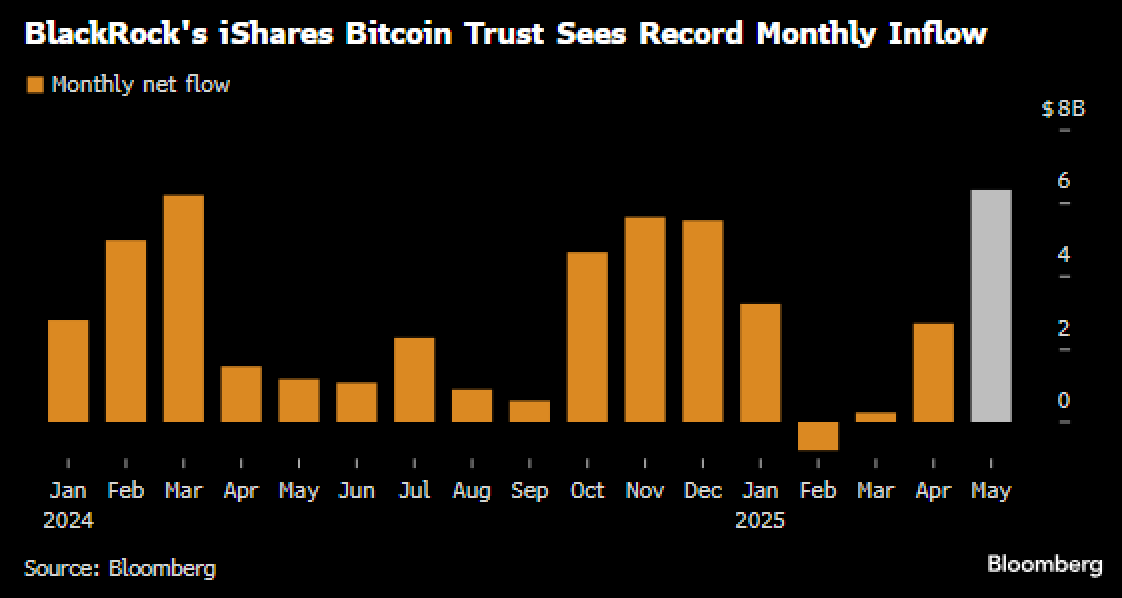

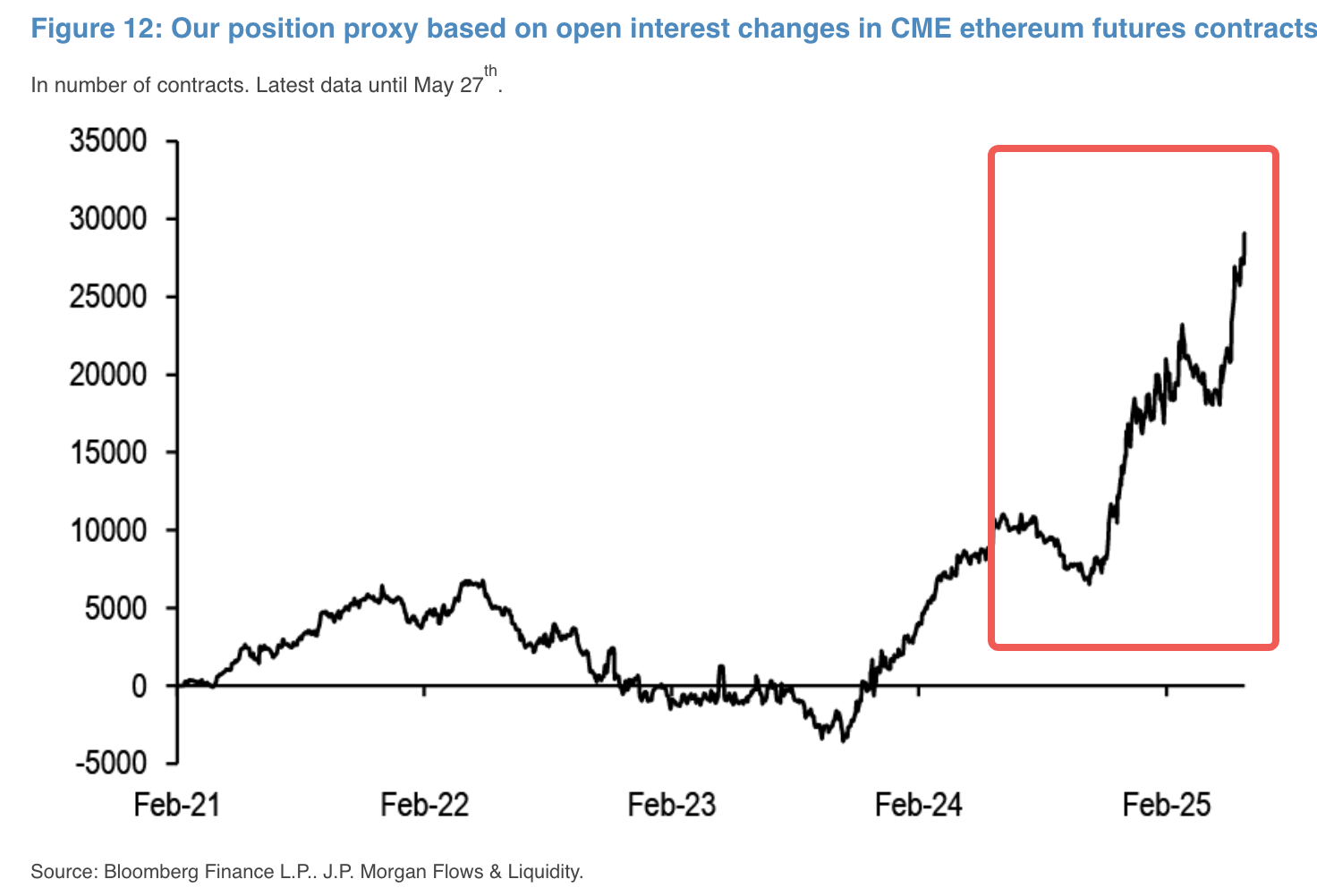

On the positive side, Blackrock’s IBIT ETF saw the largest monthly inflow on record at over $6bln, while ETH futures open-interest has been moving higher with the Q1 rally, suggesting that new longs are being added.

IBIT Saw the Largest Monthly ETF Inflow on Record While ETH Futures Open Interest has Been Climbing Along with the Price Rally

Source: Bloomberg, JPM

On the news side, Stripe is reported to be in ‘serious discussions’ with TradFi banks on adopting and using stablecoins for transactions, while Trump Media has raised a total of ~$2.3B in equity and convertibles to fund more BTC treasury purposes. Lastly, the SEC has dropped their outstanding lawsuit against Binance, with prejudice (ie. cannot reopen the case again), marking the end of the previous crypto era as well as the beginning of a brave new world, albeit with significant TradFi and political influence.

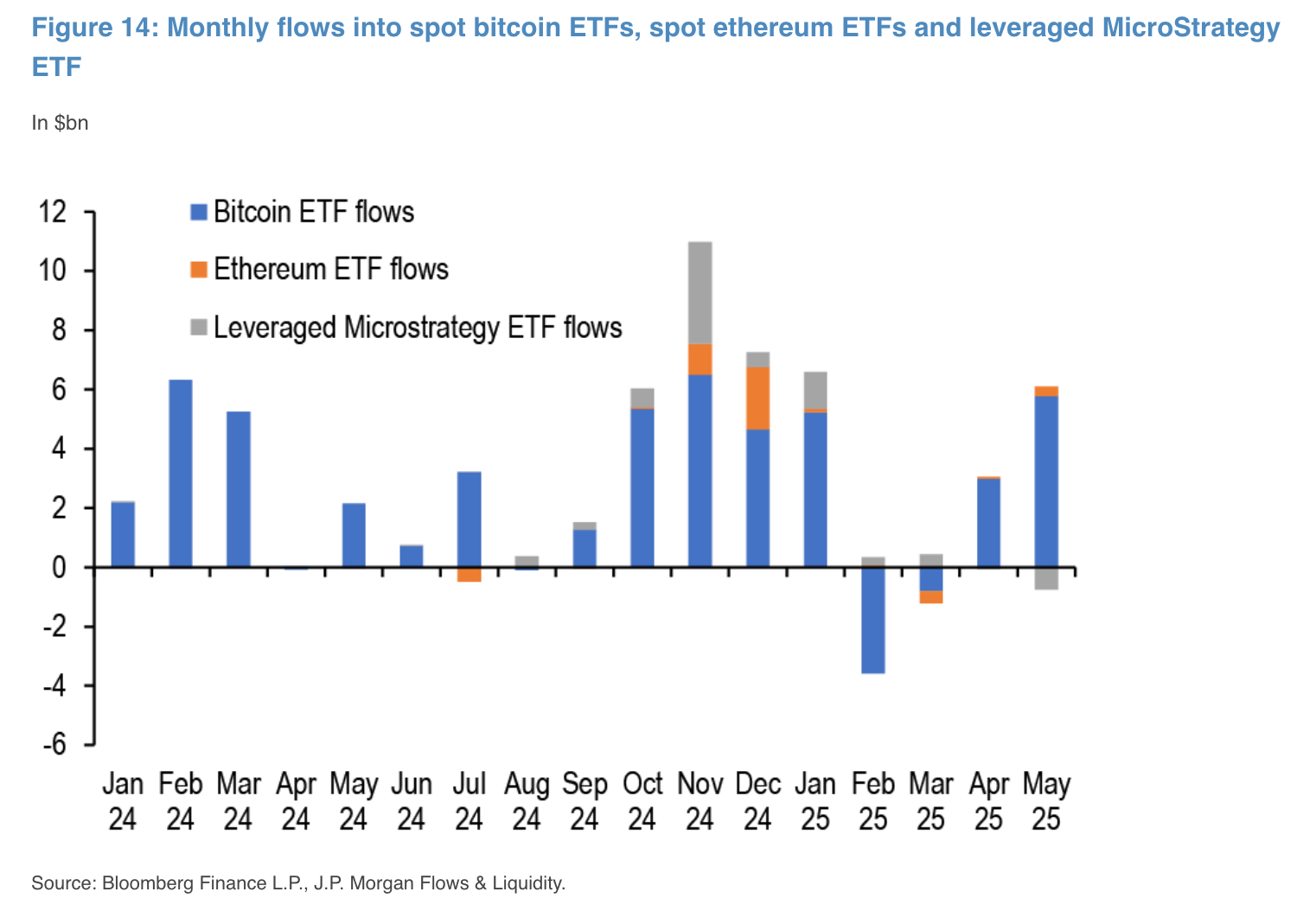

Unfortunately, despite the positive backdrop, BTC failed to hold its ground last week and prices have broken down from its upward channel, and it’s always an internal flag for us when markets can’t rally on positive news. Furthermore, the recent strength in BTC has not been matched by similar gains in crypto proxies such as MSTR, where we actually saw outflows from the leveraged MSTR ETFs, marking a negative divergence vs what we are seeing with BTC and ETH.

BTC has Broken Down From Its Ascending Channel

Source: Bloomberg

MSTR has Struggled to Keep Pace, as Their Leveraged Vehicle Saw an Outflow Divergence Vs The Rest of the Crypto ETF Complex

On a YTD basis, BTC remains a strong outformer on a macro basis and vs equity, though there are short-term signs that we might be up for more challenging times ahead, with OGs and natives continuing to be better sellers and profit takers against mainstream buying.

Will we see a catch down in performance, should macro risks take a new leg down into the summer? Our bias is that markets will be quiet and not too exciting after a volatile 1H.

Good luck & good trading friends – and try to refrain from running 40x levered position in on-chain BTC if one can help it!

BTC vs Levered Nasdaq Performance… Will We See a Catch Down Into the Summer?

Source: Bloomberg

The Infamous On-Chain Portfolio, Courtesy of X

Source: X