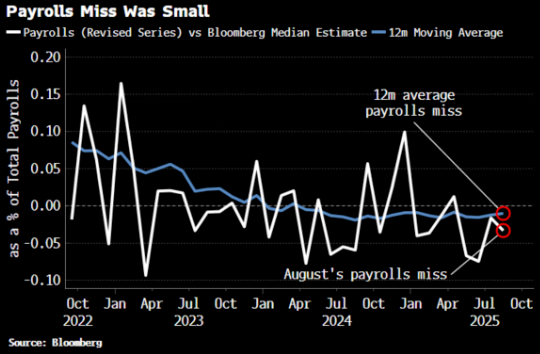

Right on queue, we entered into the seasonally tricky September period with a small headline miss on NFP, with the 3-month average trend slowing the weakest space since the pandemic.

While the NFP Headline Came in with a Small Miss, the 3-Month Average Trends Shows an Undeniable Slowing to the Weakest Pace Since Covid

Source: Bloomberg

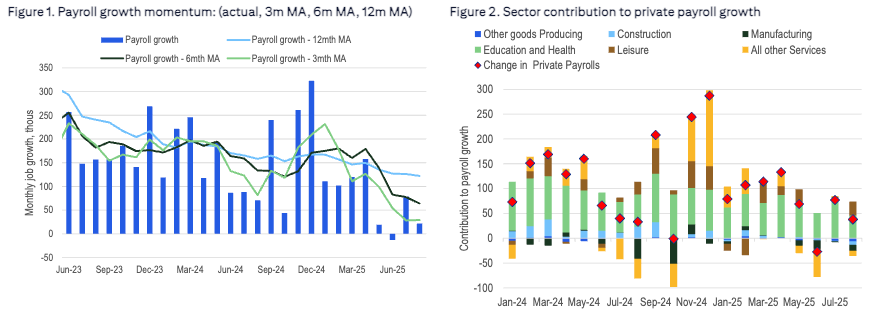

The guts of the report were also weak, with the majority of sectors reporting negative payroll growth for August, cementing the case for a rate cut this month and taking Fed terminal rates down to 2.9%, the lowest level in the current cycle. That’s a sharp 50bp repricing vs the 3.4% rate seen in the early summer.

Most Industries Reported Negative Growth Rates for the Month, with Markets Repricing Terminal Fed Rates Down to 2.9%.

Source: Citi, Bloomberg

Post NFP, rate traders are pricing a minuscule chance of a 50bp cut this month (~5%), and a 92% chance for 3 cumulative cuts by year-end. 1yr forward September Fed futures (Sep-2026) fell by 15bp on Friday, with markets pricing in nearly 3 full rate cuts by the end of 2026.

Treasury Curve Bull Steepened Aggressively Post NFP to the Steepest Levels in Almost 5 Years

Source: Bloomberg

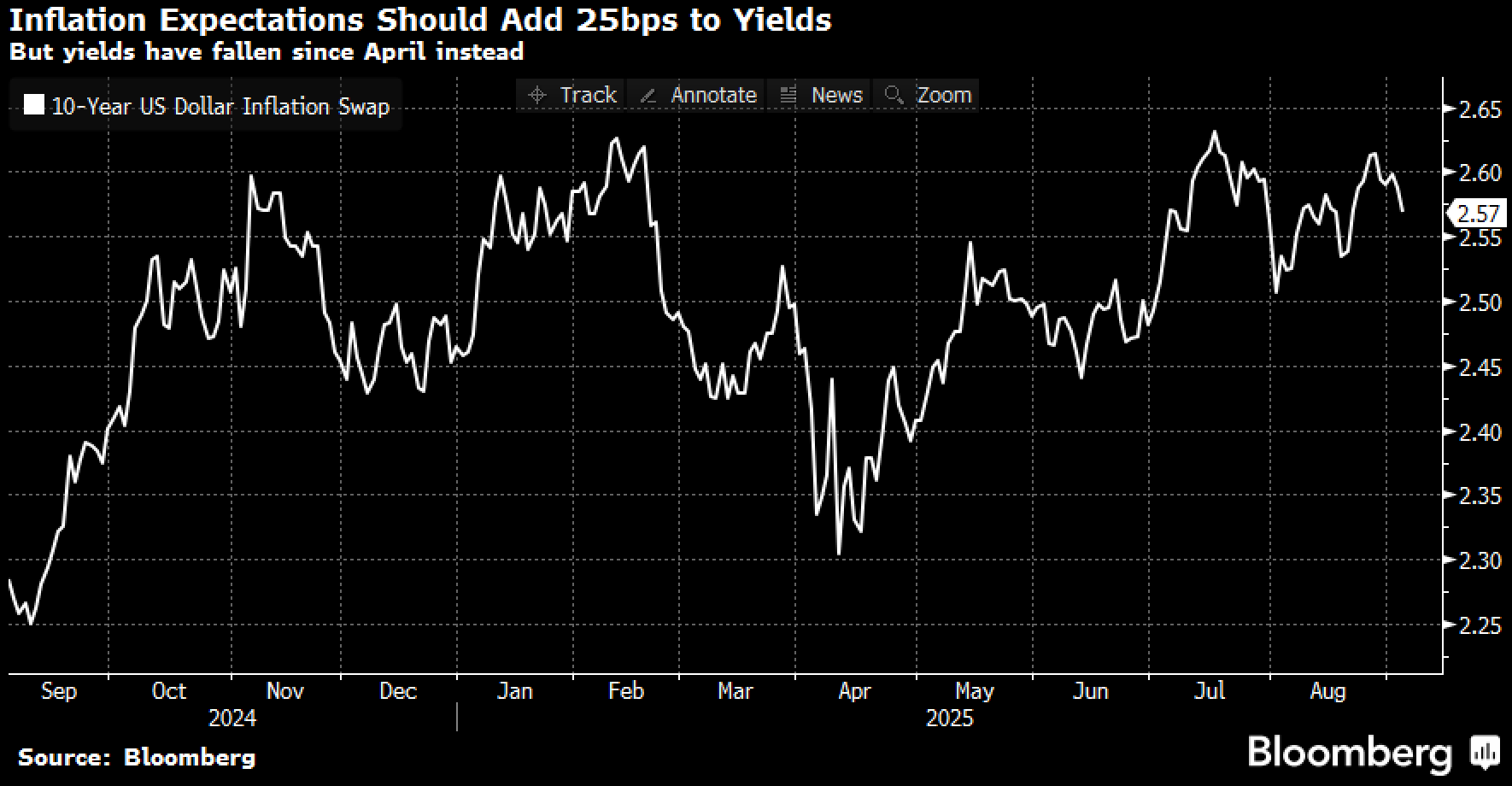

Inflation expectations were kept in check as both inflation swaps and long term bond breakevens feel as investors readjusted their expectations for a slowing economy, with CPI now pricing 2.92% for this week’s CPI. Traders will pay extra attention to confirmations of slowing underlying inflation to justify the Fed’s aggressive dovish pivot post-Jackson Hole, and these coming months of data will reveal whether any 1st signs of tariff-related pricing pressures will be coming through. Any hawkish inflation to the high side will not be welcomed by risk assets at the current juncture.

Inflation Expectations Came Off Slightly On Friday, But Remain Near Cycle Highs

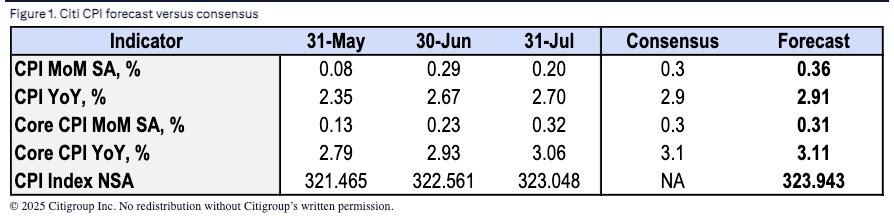

Market Expecting a 2.9% Headline Print on CPI This Week

Source: Citi

Breakeveni inflation fell slightly on Friday, a welcome relief for long-bonds which was threatening to break 5% in the US on continued fiscal concerns. 30y bonds tested and bounced off the 5% ceiling earlier this week, following the big drop in 10y yields which are within shooting distance of testing 4% on the other end.

Treasury Bonds Have Enjoyed a Strong Rally to Start the Month

Source: Bloomberg

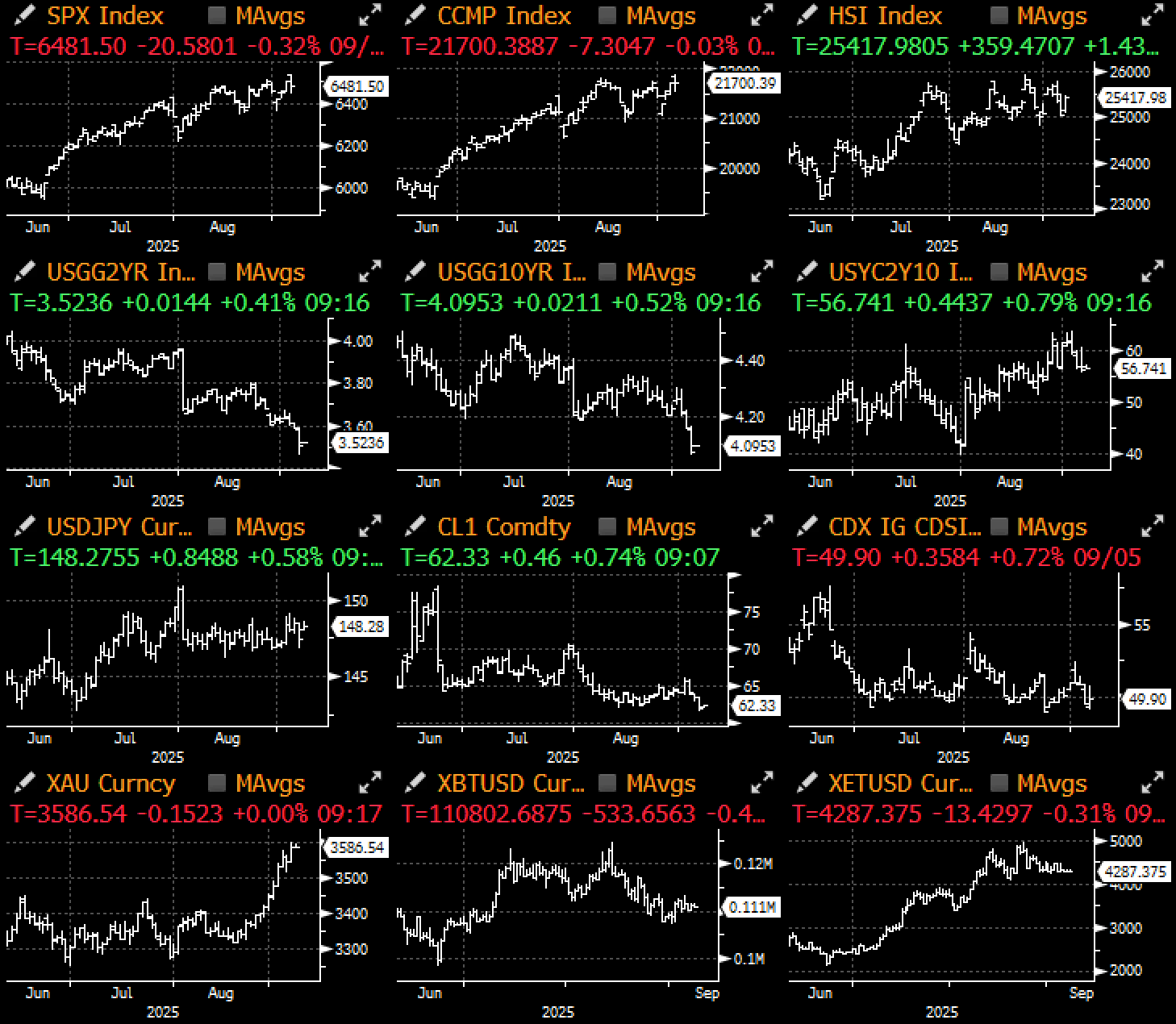

Equities were flatlined last week with weaknesses in Nvidia covered by other bellewether names as well as defensive sectors, with the SPX back in the middle of the late summer range. As mentioned last week, we are expecting a bit more volatility in the next couple of months on challenging seasonality trends, in addition to higher net leverage currently being carried by hedge funds as reported by JPM.

SPX has Been Stuck in the Tight Range Since August, But We Don’t Expect That to Continue with Sep-Nov Seasonality Trends Being Challenging

Source: Bloomberg, Cam Hui

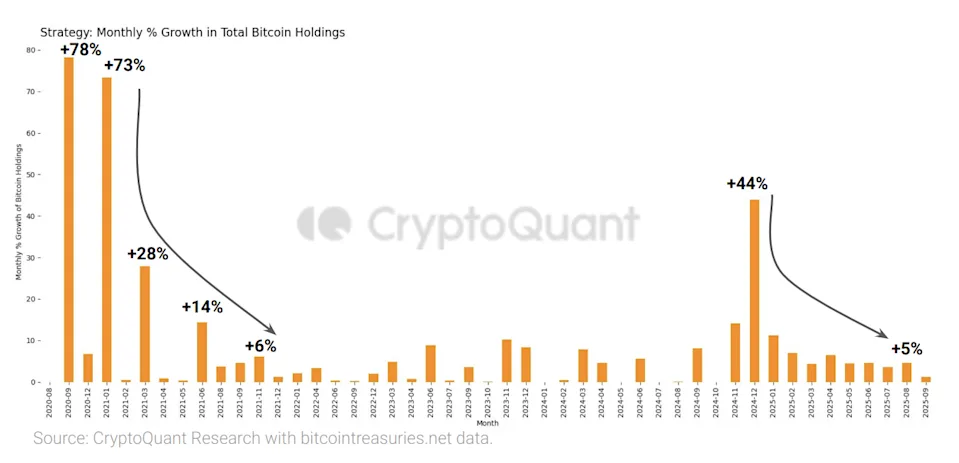

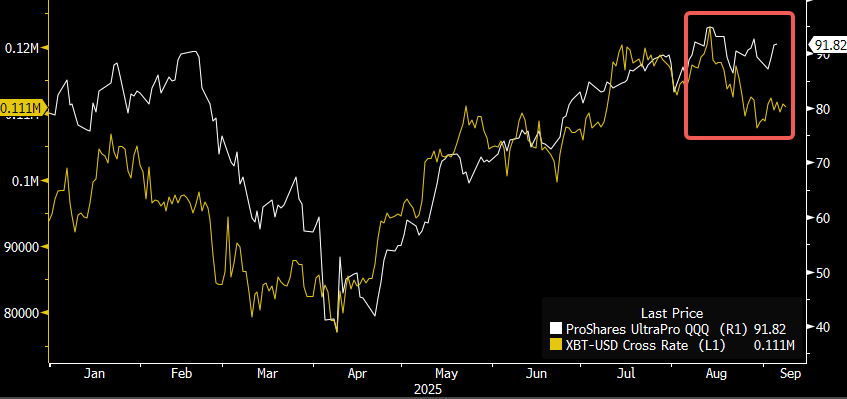

Crypto prices treaded water much of the past week, but with BTC lagging noticeably both vs its peer group as well as vs equities and spot gold. Net buying momentum has slowed with DAT buying falling off substantially, as well as CEX reporting low levels of new capital on-ramping with investors preferring to stay within the equity proxies.

The short-term picture looks a bit more challenging and we would prefer a more defensive stance consistent with the tough seasonal story with risk assets in general. Furthermore, we would also keep an eye out for any DAT-related disappointments as the NAV premium continues to come off and worries of negative convexity kick in on the downside.

Good luck & good trading!

Pace of DAT Buying has Slowed Down as Momentum has Worn Off

Source: CryptoQuant

BTC has Underperformed the Equity Complex as Well as Against the Breakout in Gold

Source: Bloomberg, Cam Hui